Rate Sheet Options from your Lender

When reaching out to a loan officer, there are a lot of options to choose from. I’m hoping to break down the decision-making here. I’ll share how we ended up with several different options, too.

Basically, it boils down to:

- Put enough down to avoid paying Private Mortgage Insurance (PMI)

- Don’t pay more than 20% unless there’s a decent incentive.

- Don’t pick a loan term shorter than 30 years unless there’s a decent incentive.

- Carefully evaluate any Adjustable Rate Mortgages (ARMs).

PMI

I broke down PMI in a previous post: PMI – Private Mortgage Insurance. We suggest doing whatever you can to meet the requirements to avoid paying this. The cost of PMI can be a couple hundred dollars per month, which is money that can be put towards the principal balance of your loan or other bills, rather than in the bank’s pockets. There are also hoops to jump through to remove PMI early, which may include paying for another appraisal on the house ($400-$700!).

LOAN TERMS

A conventional loan will likely require 20% to avoid paying PMI. There are some loan options out there that may allow a smaller down payment without a ‘penalty’ (e.g., PMI, higher interest rate), but 20% is the standard, and is usually required when purchasing an investment property.

There may be an option to put down more than 20% or you may think you can afford to pay a higher mortgage each month, so you’re interested in a shorter loan term. Unless there’s an incentive (e.g., lower interest rate, better closing costs), stick with the bare minimum to get the loan.

If there is an incentive, you’ll need analyze the math and your goals to determine if committing extra money to a higher down payment or a larger monthly payment is worth it. If you have extra cash each month, you can pay more towards your principal rather than pigeon holing yourself into a higher monthly payment. Plus, if you have more cash liquid, you may be able to purchase another rental property, which will increase your monthly cash flow.

While we evaluate the loan terms on every house purchase, I’ll share the details of the two most “unconventional” options we chose. Two things to note: 1) lenders add a ‘surcharge’ to the rate for it being an investment property, typically around 0.75%, which means the rates aren’t going to be the great, super-low, rates being advertised; and 2) the term “point” means a fee of 1% of the loan amount.

HOUSE #2

For House #2 (purchased in 2016), we were informed that if we put 20% down instead of 25%, the rate would increase 0.25% on average. If we assume a 30 year conventional loan, 20% down at 4.125% equates to about $69,700 paid in interest (assuming no additional principal payments); 25% down at 3.875% equates to about $60,800 paid in interest. By putting an additional $5,850 as part of our down payment, we saved about $9,000 in interest over the life of the loan.

Once we determined that we’ll put 25% down, we then had to figure out the appropriate loan length. On this particular offer, 30 year amortization wasn’t an option for us because we would have had to pay a point to get a competitive rate. We chose a 20 year amortization because the house already came with a well qualified tenant, we didn’t expect a lot of maintenance and repair costs due to the house’s age, and we didn’t have an immediate need for a higher monthly cash flow based on our place in life at the time.

While our long term goal was to have rental property cash flow replace our W2 income, this house was early in our purchasing. At the time, we were focused more on paying off House #1 (higher rate and a balloon payment after 5 years). Frankly, we didn’t truly understand the power of real estate investing at this time, and didn’t know how much it would accelerate the timeline for us to meet our goals. By decreasing our loan length, we increased our monthly payment, but also lowered the total interest paid over the loan’s life by over $22k. Since more of our monthly payment is going towards principal reduction than had it been a 30 year amortization, this loan isn’t on our priority list to pay off early.

HOUSE #3

For House #3, we evaluated the rate sheet for the loan term, interest rate, and down payment percentage again. This house was purchased a few months after House #2, so those rate decisions were fresh on our minds. We were quoted several options: 1) 20% down at 4.25% for 20 or 30 years, 2) 25% down at 3.75% for 20 or 30 years, or 3) 25% down at 3.25% with 0.5% points for 15 years.

As you can see, there’s no incentive to pick the 20-year term because it’s the same rate as a 30-year term. If we have additional cash, we can make a principal-only payments against the 30-year term rather than unnecessarily tying up our money.

At first, we thought paying points was an absolute ‘no.’ However, points aren’t a bad thing. Paying down your rate up front can save you an appreciable amount in interest. Plus, points are tax deductible.

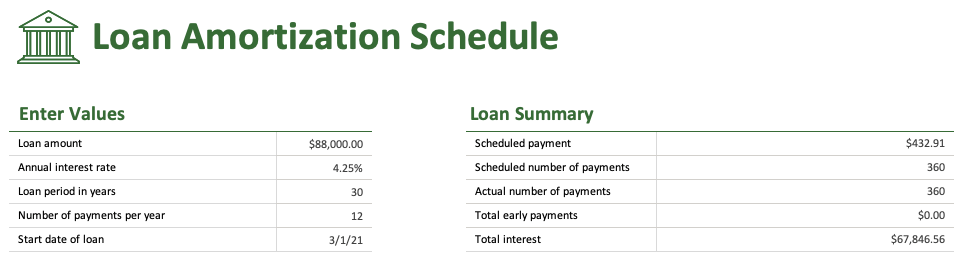

Now for the breakdown of each options. Let’s say the house purchase was $110,000 (because it wasn’t an exact number, and it’ll just be easier to use a ‘clean’ number like this). Microsoft Excel has an amortization template where you can plug in the loan terms and see the entire amortization schedule.

Option 1: 20% down payment equates to a loan amount of $88,000; the annual interest rate is 4.25%; the loan is for 30 years, with 12 payments per year. If we make no additional payments, this totals about $67,800 worth of interest paid over the life of the loan.

Option 2: 25% down payment equates to a loan amount of $82,500 at 3.75%. If we make no additional payments, this totals $55k worth of interest paid over the life of the loan. This requires an additional $5,500 brought to the closing table, but saves almost $13k in interest. It also decreases our monthly principal and interest payment (i.e., not including escrow) from Option 1 by $50.

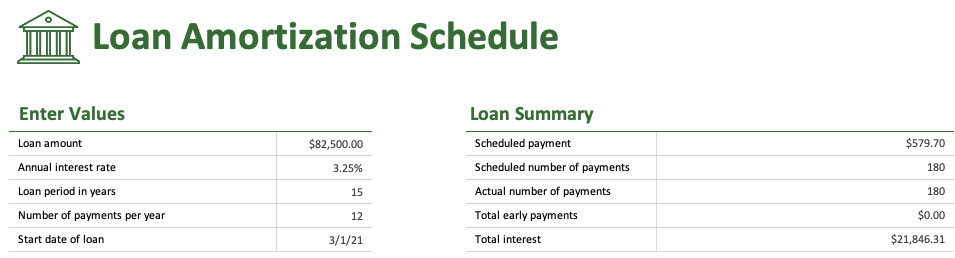

Option 3: 25% down payment, 3.25% interest, and 15 years (instead of 30 years) equates to just under $22k paid in interest. To obtain the 3.25% rate, it required “half a point.” If a point is 1% of the loan amount, that would be 1% of $82,500. This rate only required 0.5%, so that meant paying $412.50 as part of closing costs along with the additional $5,500 of down payment required for 25%. However, the shorter loan length means that monthly payment is increased (between Option 2 and Option 3, the difference is $197.63).

For about $6k, we pay a higher monthly payment, but we also save a significant amount of interest over the life of the loan. The short loan term of 15 years means this one is also not on our radar to pay off while we focus on paying down other, higher interest and higher balanced, mortgages. In this case, the benefits of the big picture math outweighed the increase in monthly payment.

We are five years in on this mortgage and are already seeing significant reduction in the outstanding principal due to the amortization schedule becoming favorable more quickly. In 10 short years more, our house will be fully paid for, through rent collection, without a single dollar of extra principal payments from our other financials. What a great feeling.

ADJUSTABLE RATE MORTGAGES (ARMs)

An adjustable rate mortgage can be beneficial depending on the terms and how long you expect to own the house. For us, we expect to hold our investment properties for a long time, so it wasn’t worth the risk of an ARM. Many times lenders won’t even offer an ARM on an investment. However, when we purchased our DC suburb home, we knew we didn’t expect to be there for more than 5 years, so we chose a 5 year ARM.

After a positive experience with that decision, we also chose an ARM on our second primary residence. We chose a 5 year ARM, even though we expected to be there longer than 5 years. We figured we would either accept the new rate, if there was one, at the end of the 5th year, or we would refinance when necessary. As a result, Mr. ODA monitored rates and refinance options over the last year or so. Unexpectedly, we sold that house 3.5 months shy of the end of the initial ARM term so we didn’t have to do anything.

I break down all the details of an ARM and our decision making in a recent post.

SUMMARY

When I reach out to my lender to ask what the rates of the day are and begin the process of locking a rate on a new loan, I ask for options. These options are in the form of a “rate sheet.” When you ‘lock’ a rate, you’re actually locking the ‘rate sheet,’ not the individual decisions of loan length and percent down. For every house, we evaluate the rate savings that can come from doing something less “conventional” than a 30-year fixed at 20% down mortgage. Our decision is based on what’s best for our goals and our cash in-hand.

As shown above, in our early decisions, we favored shorter loan terms for rate savings. but since House #3’s purchase, we noticed how much more we cared about low monthly payments and low down payments to allow us to buy more properties along the way. Every investment property loan since House #3 has been the ‘standard’ 30-year fixed at 20% down. Because of this perspective shift, we were able to buy six properties in 2017, which gives us about $2,000 in monthly cash flow that we can then use to pay down mortgages.