It’s been a while since I’ve talked about the credit cards we have and how we manage using them. I seem to be caught in multiple conversations around me lately about how people feel credit cards are bad, so they use debit cards. I understand that some people have a bad history where they weren’t disciplined enough, but don’t you think after several years, you’re older and wiser and could likely teach yourself discipline? My last post was about how you could make $500 in a year just by putting an expense on a credit card and paying it off each month if you have 2% cash back. So let’s dive in to what we made in 2025. There is one caveat: we have a lot of credit cards and we put a lot of effort into using the categories; I fully understand this is more effort than nearly anyone else is willing to put in. But hopefully you can take just one thing away from this teaching and information.

You need to find your why. Your why is your driving factor on everything. Put things in perspective of “if I hadn’t spent $10 on that coffee, what could that have gone towards to provide me with longer term satisfaction?” I admit that I’ll go to Starbucks for a drink, but I buy about 5 of those $6 drinks (I get a very basic thing) in a year.

INTEREST EARNED: $1,191.42

The easiest way to make your money work for you is through interest on a bank balance. Currently, savings rates are hovering around 3.25%. I’ll just jump right into it: compound interest. Even if you have $500 extra, put this money in a savings account. At this interest rate, you’re earning $16 in a year, but that’s $16 more than you had at the beginning of the year. The mentality that $16 isn’t “worth it” is the type of thought process you need to move away from. If that balance was $5000 instead of $500, then that’s $162 in passive income.

TREASURY DIRECT: $2,098.14

This is more advanced interest income. You can create an account here and invest your money in short term securities (think CD type things at a bank). The rate is currently about 6.25%. You’re tying your money up for a period of time (4 weeks through 30 years), and the rate is tied to the term of investment, but we are actively managing our investments in 4-8 weeks segments, earning about $50 at a time.

CREDIT CARD REWARDS: $1,947.75

We have several credit cards. Some are a flat percentage for all purchases, and some have categories that earn an additional percentage back. The amount that I have here is only related to what we cashed out. More was earned, but we keep some in our Chase account balance so that we can get a bonus if we book travel through their portal.

If you don’t want to manage categories, go for the Citi Double Cash card. It gives you 1% on a purchase and 1% on a payment. The key here is that you can’t claim a statement credit because that doesn’t count as a payment, meaning you don’t get your 1% on that amount.

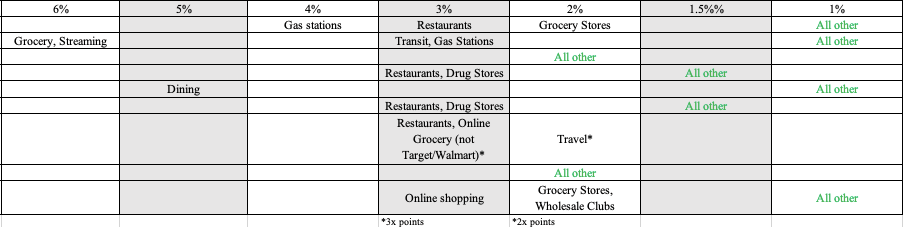

Without giving too much away on the cards we have, here’s a snapshot that I keep in my phone to remind myself what card to use for each purchase. The 5% category there changes quarterly. Usually, if I can’t use my Citi card, then I’m checking this graphic to see what the next best percent back for “everyday purchases” would be.

SUMMARY

This is “passive” income we’ve made. We had other avenues that brought in other income, but this is where we basically just spent money or kept money in certain accounts and brought in an extra $5,237.31. That’s a big number, and I’m sure that type of money can make a difference in your life or pay for a trip you want to go on.

I snapped a screenshot of a back and forth with THE Dave. I don’t know if it was accurate, but it sparked the same frustration in the poster as it would me. In summary, the caller says that if they put $2,000 worth of expenses on a credit card and pay it off before interest hits, getting 2% cash back, that’s an extra $40 per month. Do you see where this is going yet? Dave says no credit card. The $40 per month isn’t worth the credit card, and that’s not how you get rich.

I guess the first question is: Is everyone’s intent to be rich? Or is the average person’s desire to live comfortably and enjoy their life without worrying about their spending and making ends meet?

Every year I summarize the extra income we made in the year. I admit that we’re far above average in the management we do to get that, but the concept is there – we made more than $0 in extra income, and it’s nice to have money coming in that took barely any work.

I also take the time to admit that some people can’t manage their credit card spending and need the immediate acknowledgement in their account balance that money is leaving. However, even if you made credit card mistakes at 18, have you learned that lesson 10, 20, 30 years later? Do you think you’re in a different phase of life with more control and brain capacity to manage that spending?

$40 per month is $480 per year. If you took that extra income and put it in a separate bank account, what could you do for yourself for about $500? Does that sound enticing to put towards a trip, or to use that month allowance to go to a restaurant?

The flippant response that having no debt and not using a credit card, even if it’s paid off monthly, is doing a disservice to actually teaching people money management. Make your money work for you through rewards and interest, with very little effort, and you have that extra money to do things, even if that thing is just to pay a utility bill more easily.

My next post will detail the extra income we made in 2025 and how we manage our money to work for us.

I’m working with Keller Williams, and in a lot of ways, I see the parallel with Amway, which I also have experience with. People love to have their negative opinions about these companies, but both companies are teaching money management in a productive way if you’re coachable and paying attention. They’re teaching you to think outside the box.

I recently listened to Dianna Kokozska’s Ted Talk “Why Wealth Creation is the Ultimate Act of Love.” It makes the point that putting the effort in to being financially successful provides security, freedom, and opportunities for not only you, but others close to you in the event of a need. A phrase stuck with me: wanting money isn’t greedy; wanting money is strategic.

She shared how her son’s wife’s health was in trouble, and they needed money for a treatment. Not that everyone should have the ability to write a check for $35,000 on a whim, but do you have the ability to manage a crisis? Are you learning from others around you who have been successful? Are you keeping an open mind and actually making the attempt to build wealth?

Choose to be around people who challenge you. Look at your closest 5 people; are they where you want to be in life, or could you find a sphere of influence that can challenge you and teach you how to make money?

VICTIM MENTALITY

She quickly touches on the victim mentality. I see this around me at work often. People who seem to always have a crisis to manage. It’s in your head, and you’re focused on the negative instead of creating a positive outlook to be more productive with your money. Are you stuck in a spiral of “why does this keep happening to me,” or are you finding a path forward? Sure, we hit rough patches and things go wrong. The path forward comes in your decision as to whether you’re going to let these issues define you or if you’re going to find a way to make things better.

I have a family in one of my rentals that has both parents working blue collar jobs. He works in a kitchen and she usually works reception type jobs. I’ve known them since 2016. At that time, she delivered her 3rd child really early (I can’t remember, but it was like 30-32 weeks). There were extensive medical bills. They taught their children to work hard and to respect others. They had their own medical challenges. They lost several jobs over the last 9 years. They’ve had car trouble, making it a challenge to get to work. They ALWAYS find a way forward. If the car doesn’t work, they figure out uber and buses. If they don’t have money to pay bills, they tap into resources. They take initiative to find ways to get help with rent. I see a few splurges in their home, but they always seem like something they really appreciate. It’s not an excess of things that they’re spending money on. They communicate their challenges and let me know if something they’re working on is going to take more time. The rent they pay me is significantly under market value for that house, but I can’t bring myself to raise the rent that quickly or force them out to get it re-rented. They work so hard and are raising their kids to be resilient, and I just appreciate it so much. That’s the type of person who does not have a victim mentality.

While their efforts aren’t yielding them an extensive savings account or the ability to write a $35,000 check, they keep moving forward. Each set back is a lesson for them. They’re learning and growing. They’re not blaming others. They don’t tell me it’s someone else’s fault they don’t have money to pay rent on time.

POSITIVE APPROACH

You can be positive without being unrealistic. Optimism looks like focusing on the good in a situation, expecting a positive outcome, and approaching challenges constructively rather than ignoring them. There are many studies out there that will tell you having a positive thought process will lead to better stress management and overall well-being. It involves self-talk, reframing negative thoughts, practicing gratitude, and believing in your ability to overcome difficulties, fostering hope and improved health.

If financials are a struggle, plug in with someone who is doing well. Surround yourself with those who are meeting the goals you have for yourself. By being around these people, you will pick up on their thoughts and actions and find a way that you can implement some of those actions in your own life to start seeing success.

We opened a new credit card to purchase windows for our house. When we bought our house, there were 3 windows that had the gas seal broken and were dirty looking (not cloudy like I’d think would happen). Three sashes were really bad. One is on the side of the house in our bedroom, so we never see it. The other is the window over the garage, so front and center. We just keep the black curtain drawn so hopefully you can’t notice it, but it’s definitely noticeable if you look for it. Over the past 3 years, more windows have started to go. Some are getting to the point of being that bad, and some just have a holographic look to it that you can catch at certain angles. We also have a couple of windows that are freezing if you get near them. In my daughter’s room, I line the bottom of the curtains with stuffed animals to keep some of the cold out and let the animals absorb the cold.

Well, it was time to open a credit card then.

All of these companies are happy to open a line of credit for you. You can make payments on your windows (or really anything) for 5, 7, 10 years. Well, if you have good credit and don’t open credit cards often, you can look into giving yourself an interest free loan for 12-18 months.

We look for a credit card that offers at least 12 months of 0% interest and a reward of some sort. Usually the reward is related to an amount of cash back if you spend a certain amount in a certain period (e.g., $300 cash back if you spend $5,000 in the first 3 months).

We’ve done this several times. We opened a credit card to pay for IVF to have our first child (~$30k). We opened a credit card for the new carpet we put in our current house (~$10k). Now we opened a new one for windows ($11k). We pay about $500 (at least the minimum monthly payment owed) per month and always by the due date. If you are late on a payment, you forfeit the free interest and may even owe the interest that would have been owed on previous payments. Then as the end date of the 0% interest gets closer, we make a plan on where money will be transferred from savings to pay it before that date.

That’s one of the keys. We’re not taking this because we don’t have the money to pay it right now. We’re opening a credit card to allow our money to earn interest in a savings account of some sort for all that time. So instead of spending that money and losing that income, we delay the payment as long as possible to keep our money working for us. If you need something and don’t have the money to pay it right now, but you think you’ll be able to make payments on it as you earn income, then make that the variable. Don’t open a credit card if you haven’t ever and don’t plan to have that amount of money within the term. We also don’t open a new credit card while we’re paying on the previously opened credit card. In this instance, we paid off the balance of the carpet this past October. While it would have been nice to delay opening a new card a bit longer, the windows are really in rough shape, so we only had 2.5 months without a large credit balance to think about.

Well, tracking spending is just bugging me. We’re over where I want to be in monthly spending. I registered the kids for summer camps, so that was $580 more than usual spending. I also paid for a kid to take swim lessons ($85) and our gymnastics cost went up because she earned a spot in an advanced class that’s a half hour longer. If I take out the camp registration cost, then our spending is about $1700. My goal is $1350 per month. That’s not what we can actually afford (Mr. ODA’s number is higher), and I’m learning may not be realistic, but that’s my general goal each month. I’m halfway into March and can tell you that we’re going to be nowhere near that number this month, which is frustrating, but also reality.

RENTALS

We had two service calls this last month. One was a water heater being out and the other was unnecessary but cost us $100. This lady has actually been a problem in this realm. She claimed the mail key didn’t work for weeks and took forever to respond to messages. Mr. ODA finally went over there and it turned out she was trying the wrong box and not paying attention to what Mr. ODA was telling her. Then she said the microwave wasn’t working. The circuit was tripped, and Mr. ODA let her know that she can’t run an airfryer and microwave at the same time. Then she said the washing machine wasn’t working. We had an appliance guy go out and he said, “it’s working fine. There’s not supposed to be any more water than this in a high efficiency machine.” So much fun.

I’m expecting a tenant to move out at the end of this month. I still haven’t heard the final information on that, which isn’t surprising, but that’s on the horizon.

I increased the rent on two units over the last couple of weeks, which is in addition to a raise I put into effect on another one last month. I also have let three renew at the rate they were at the past year (or more) based on their cash flow numbers and the tenants in there.

PERSONAL

I’m still working part time. Although, these hours are 50% more than I had signed up for. I’m helping get another office organized and training a new hire. It’s been a lot. I feel productive, but I want more hours in my day. Mr. ODA started a part time job as well. We’re on the hunt for insurance help. We’re paying out of pocket for the whole policy that we were under for the last 5-6 years. While we’re not expecting a lot of coverage to be paid by the employer, there is a benefit to having the funds come out pretax.

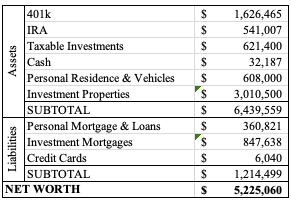

NET WORTH

Well, my update isn’t really that accurate. I’ve updated the numbers I could, but I’m already days behind on my schedule, so I couldn’t wait for Mr. ODA’s numbers anymore. We are still carrying half of the window order on credit cards (and that install should be next week… hopefully… it’s been pushed back once already). Our investments are down even more than last month, but I don’t know the extent at this time. Our net worth decreased from last month, with 10 accounts not updated, so I’d say it’s a substantial hit.

We have been financially secure for Mr. ODA to quit working for years. In fact, the plan was that after he met the requirements for his paternity leave taken (which was essentially work the number of hours you took as leave), he would quit. That goal was met back in early 2023. The hold up for him quitting was always health insurance. Him working wasn’t a huge detriment to our life and things we wanted to do, and he was getting most of his health insurance cost covered by his employer.

Well, at the beginning of 2025, the deferred resignation program was introduced. While the first round was very questionable, our life was greatly affected by his employment and the government over the next few weeks, so it was a no-brainer to take the program during the second round. His last day of work was at the end of April, but he was considered employed and paid through September 30th.

As part of his separation, his health insurance was covered for about another month. He had the option to extend his current insurance for another 18 months after that, and that he’d be responsible for paying the full premium. At the time, it was about $1700, and the 2026 premium is $1900 per month.

MRS. ODA’S INSURANCE OPTION

Meanwhile (just coincidental timing), my current employer was investigating a new insurance policy for their employees across 4 offices. They were originating their insurance through the Ohio office. It was a really expensive policy for them. For the 5 people who were taking advantage of that insurance policy, they could have covered 23 employees on this new policy. We learned that Ohio is one of the most expensive states to originate insurance out of it, so we moved the policy to Kentucky.

Anyway, through that process, the insurance sales person was completely incapable of answering basic insurance type questions. Mr. ODA asked for the brochure of benefits. He said, “I emailed you the summary of benefits.” Mr. ODA pointed out that the summary of benefits was a summary of a much larger document, and we wanted those details. He said that didn’t exist. Mr. ODA called the actual insurance company, and that lady laughed and said they definitely have that.

The policy also required a gap coverage policy. The information given to me did not make me feel like it was going to be a smooth process. It sounded like the doctor’s office would submit the claim to my main insurance company. Once it was processed, I’d have to take my bill and EOB and submit it to the gap coverage company for payment. So I’d have to manage the paperwork processing and the payments between everyone.

Their quote for the family policy was about $1750. I told Mr. ODA that it wasn’t worth all that extra effort and the concern that this insurance policy would even work right (because this sales person was not able to answer questions or quell concerns), just to save about $150.

FINAL DECISION

So in the end, we decided to keep the enemy we know. All of our doctors are now solidly in place since we’ve been in Lexington for 3.5 years. I didn’t want to risk needing to switch to a different doctors office because of eligibility and coverage. I didn’t want to risk the coverage being a fight even more than my current policy creates. But mostly, in case something did end up going awry with this new policy option, we couldn’t get our old policy back. So while adding $1900 to our monthly expenses while losing Mr. ODA’s income isn’t the most ideal situation, this is where we’re at in life.

About once a year, I have an urge to share some tips. I’m blessed/cursed with the ability to see how to organize things and tasks in my day, which doesn’t come naturally to everyone. The cursed side is that I have 4 other people living in the house with me, and their desire for things to work efficiently doesn’t match my desire. As the end of the year approaches, and new years resolutions start to be made, here are some things I think about when I’m managing my house.

ONE LAYER ORGANIZATION

To the fullest extent possible, I’m going to put things one layer deep. I’m looking to take one action rather than multiple steps for small tasks. Like I mentioned with the milk, I’m going to make sure I’m able to grab the most used things with my free hand. I’m also not going to lay things on top of other things because that means I need to move those items out of my way to get what I need. I’m willing to go one layer deep. That means I want to grab something with one hand to reach the thing I’m looking for. I don’t want to move several things to get to the one thing I need.

I’m thinking multiple steps ahead in the decision today. Here are some examples of what I mean by that.

Milk is something that’s used daily in the house. So I put it at the front of the fridge. I just need to open the right door and grab the milk handle with my left hand. If I need to open the door, move things out of the way (possibly even set something on the counter), and then grab the milk, that’s an inconvenience that isn’t necessary when milk is a frequently used item.

Two kids were on medication, so we had a lot of kids syringes in the silverware basket. I put them into the basket upside down so they don’t collect water and get things wet as I pull them out. I’m thinking several steps ahead in the one action I take.

When we get home with groceries, I don’t just put them in the pantry wherever they fit. I take the time to rearrange items so that everything is where it belongs and now strewn about.

I rinse out the sink after dishes so that crud doesn’t harden onto the sink and require me to scrub it later.

When putting something away, don’t go 90%. I watched someone put shoes in front of the shoe bin instead of in it. Just finish the step if you’re that clsoe. Those ten-percents add up over the day (not to mention the distraction it causes me to see it, do it, and forget what I was first doing).

SWEEP CLEANING

Now, even though I mention putting those shoes fully away, I do have a caveat. My overall cleaning process doesn’t mean that I’m going to take an item and put it exactly where it belongs immediately. I’ve seen reels online about how people had a life changing feeling because they put something immediately away instead of putting it on a surface to move/touch a second time. I don’t agree. If you have a kid’s headband that belongs in her room upstairs, then taking that one item from the first floor to her room is time consuming. I like to sweep rooms. This isn’t for when you get home with something and need to put that one thing away; this is meant as a mid-day and end of day straightening up.

When I’m doing a full clean, I’m going to take the kitchen things that are in the living room and place them on the counter in the kitchen. I’m not going to put them where they belong in the kitchen; I’m just focusing on cleaning the living room. If something belongs upstairs, I place them on the stairs. I don’t take a dish and put it right in the dishwasher. I gather all the dishes and put them on the counter to load the dishwasher once. I follow this process through the whole house. If it’s something that I can easily put right away, I will. But after years of cleaning up after my family, I know that I’m going to find more than one thing in the living room that actually belongs upstairs, so I’ll create a pile to bring up when it’s time to move that direction.

REDUCE

The other main part of organization is just to have less stuff. Right before Christmas, I was tired of cleaning up after the kids when they play in the basement. Most of their toys (outside of crafts and board games) are in the basement. They’d dump bins to look for something or to play with things (it really wasn’t ever just to dump for the sake of dumping), but they wouldn’t pick things up. I finally went through and got rid of all the little trinkets. I used to hold onto things that I thought mattered to them, but I got to the point where having things is a privilege. If they couldn’t keep up with cleaning and keeping their pieces of items together, then it shouldn’t be here. I eliminated toys that were missing pieces or broken, and I got rid of all the trinket type things (think McD’s toys). Cleaning up is much easier and faster now because there are less pieces, so I can create piles of where things need to move to and get them put away without having to make many trips around the room.

SYSTEMS AND SCHEDULES

I have a few goals that I’ve set for myself. Now that I’m working part time, my free time is less and the kids want more of me. I discovered that my life is easier if I made a plan for cleaning. For instance, I used to vacuum every other day. That’s just not practical anymore. Now I look to vacuum twice per week, but that doesn’t prohibit me from vacuuming if there’s a mess made at the table. More specifically, I made Saturdays bathroom day. I learned that if I didn’t clean the bathrooms every Saturday, then I’d start noticing that it was dirty mid-week, when I didn’t really have the time to be dedicating to the bathroom. So I made it a priority to clean all the bathrooms at the beginning of the weekend. When I was working in DC, I had a friend tell me something similar about her cleaning schedule and I thought that was crazy. Three kids later, and it all makes sense now.

I also have a goal that we go into the school week with all the laundry done. While Mr. ODA does a load or two of laundry during the week, I strive to do a final load and clear our all the hampers before the week starts. Sometimes I get it into the dryer, but it sits in the dryer until the next load needs room in there. Sometimes I’m feeling really on top of things and I make it a priority to get it washed, dried, folded, and put away before the kids’ Sunday night bed time. It creates less stress and I hear fewer “is my shirt clean that I want to wear” type questions to eliminate that disappointment.

Frankly, I could add more things into this type of schedule, but I’m still learning the concept of juggling between work, school, home, and kids attention needs.

SUMMARY

Create a system that works for you. These are things that make my life easier, and I find it more straightforward and faster to clean up after my family of 5 with these thought processes. If you create a system and do a house reset each night, it doesn’t become an overwhelming task to tidy and clean when it’s actually necessary. It also eliminates the distraction of the mess, and it doesn’t create the anxiety and stress if someone shows up unexpectedly or you need to prepare for company.

Before I get into an update, I have a quick perspective moment. Our preschool has a 3.5% processing fee to pay monthly tuition online. Tuition is $265, so the processing fee comes to $9.27. If I paid it online instead of writing a check each month, that would be an extra $83.43 I paid for basically nothing. For perspective, I spent $82 on a grocery run of essentials (e.g., dog food, paper towels, milk, eggs, etc).

RENTALS

I had to give notice to one household by 1/31 if I were to raise rent. Their lease ends 3/31, and that will mark 3 years with me. I was panicking because it’s our most expensive house (it’s also our nicest and biggest, and it’s fairly close to downtown). Rent has been $1750 for the last 4 years. Last year I missed the notification to raise it because a January deadline surprised me, but this year I put it on my calendar for January 1st to do. And then I dragged that calendar reminder through the whole month, only needing to then set an alarm to make sure I did it at 8pm on the 31st. I raised it to $1800 and they accepted within the hour. Phew. They’ve been late three times in 4 years and clearly communicated what was happening each time. We’ve had two major issues at the house that they rolled up their sleeves and helped mitigate the damage before the tech could get out there. They’re just really great tenants.

I had two tenants pay rent before the 1st and one partially pay before. That was surprising since the last two months I’ve had very late payments come through. I still have one person with a partial payment outstanding as of this morning.

We had a water heater go out on Thursday in one property, but otherwise I’m counting all my blessings that we made it through 2 weeks of below freezing without incident.

PERSONAL

I’ve preached monitoring your spending by writing it down for years, but I hadn’t done it. I had done it a few times retroactively, but I never made the time to keep on top of it to make pivots. With Mr. ODA leaving his career, that’s a high six-figure income that we’re without now. I’m working part time, but that’s basically a one-to-one ratio of income to health insurance. I’ve calculated that we need to be about $1350 per month in spending outside of the mandatory bills (e.g., mortgages, utilities, tuition, insurance). My threshold is lower than what Mr. ODA said is his threshold, so this isn’t a hard-and-fast amount, but one that is my “I feel OK if we’re close to this number” concept.

We screwed that up a good bit by purchasing a new vehicle and putting new tires on said vehicle immediately. We also had to pay for a previous heating issue fix in our house and a downpayment on new windows (which, quick side note, are glaringly needed as we go through 2 weeks of single digits and can feel the drafts). I’m also not counting the things that we do as mystery shops since those are effectively reimbursed (sometimes our cost isn’t fully covered since it’s a whole family outing and not a single person, but I’m not drilling down in that detail since I don’t have the specific break down of how Mr. ODA is getting paid). If I take those things out and remove expenses for rentals, then we spent $1597 in January.

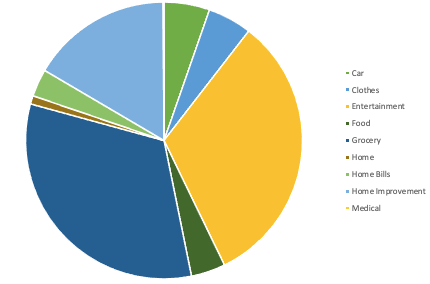

This isn’t the best representation of our spending, but I’ll develop this information as I have comparisons month over month. I also can’t seem to pick a better color scheme without it being a very manual process. Grocery, Entertainment, and Food are our biggest slices there. The entertainment category is basically why I gave up categorizing things years ago. Here I put things like going out for a drink, because while it’s at a restaurant or bar, the sole purpose was to have a drink and hang out. It also includes going to a gymnastics meet with my daughter, my fitbit purchase (I guess because I’m counting it as extra spending and not a necessity), and gift giving costs. We spent $528 on groceries this month, which feels low. I pushed really hard to clear out the food we have in the house already during our 2 weeks of being snowed in, but I hope that this is an accurate representation of monthly spending on groceries.

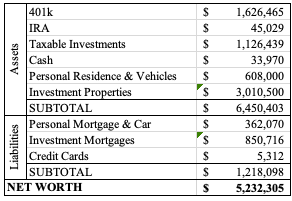

NET WORTH

It is higher than last month, so that’s good. Credit cards are carrying $4500 worth of windows, so it’s nice how low of a balance those are outside of that 0% interest balance we’re holding onto. Our investments struggled a bit over the past month, but the payments on mortgages and loans helped offset that.

Several months ago, we went on vacation. While there, we got the kids ice cream from McDonald’s. It was $1.79 each. They had been given multiple “treats” during the day (not of the food variety, but riding the carousel and train at the zoo), and I didn’t see it necessary to spend $10-14 on ice cream after a big day. But it was something that would bring them joy, and it would be a surprise since it’s not a regular occurrence.

Our financial advisor told us that he has a saying in his family, “we can’t afford ice cream.” The statement isn’t meant as a literal statement of “we can’t spend $5 on ice cream because then we won’t be able to pay our necessities.” The statement is meant as a frame of mind. It’s meant to teach an understanding that you need to prioritize your spending and have the big picture in mind.

Treating our kids to the occasional ice cream is ok. Giving them the ability to know that ice cream is not going to happen all the time, but we can get it once in a while shows that we have to prioritize our spending and determine where this ice cream splurge fits in our budget and long term goals.

That comes across with a much higher sense of philosophy than I intend for this example, but the general concept is there. We take the time to determine whether spending money on something is valuable to us and worth the cost.

THE STARBUCKS / CONVENIENCE PAIN

So many people knock the concept of buying or not buying a Starbucks. I see things said all the time like, “I didn’t buy my daily coffee this week, so I’m practically a millionaire.” That density is keeping you in your poor mentality. You think that not purchasing a coffee and getting the instant gratification should yield the instant gratification of wealth. Instead, the point all along was on your mentality. Do you find it a priority to spend $6-8 on a coffee routinely? Perhaps that means you’re also thinking you can treat yourself to that new shirt, new shoes. Perhaps that means that you’re also willing to walk into a convenience store, like at the gas station, and buy a soda or an energy drink.

I also think back to a friend who would leave their house to go get a gatorade at the gas station down the road. They once left their house while we were there, bought 3 gatorades, and came home to play a game with us. This was routine. What if you went to the store and bought a case of gatorade? You’d have a cold drink that you want in your fridge on demand, you wouldn’t be taking the time to leave your house, you wouldn’t be spending money on gas, you wouldn’t be adding to the wear and tear on your vehicle (which eventually costs literal money), and you wouldn’t be paying a premium for the same drink.

A quick search tells me I could buy a 28 oz Gatorade for $3.69. I can buy a 12 count of 12 ounce Gatorades at the store for $7.98. In a given sitting, do you really want 28 ounces or can you get by with 12 ounces? Even if you want more and want to drink 2 Gatorades in one sitting, it would cost you $1.26 to have two of them at the ready in your refrigerator.

I recently was behind someone on a drive down a two-lane road. They were going 35 in a 45, in a car that had plastic as the driver side window, half the bumper missing, the passenger mirror missing, and a tail light busted out. They finally got out of my way at the gas station, where I watched them park in a spot and walk into the store.

STOP AND THINK

People don’t think about how that small decision can snowball. You’ve been trained through social media to think that you have “earned” a “treat.” Marketing by these companies tell you that it’s not a big deal to spend your money this way. Be stronger. Think about the decision. Take just one month to physically write down everything you spend. Yes, I mean take a pen and paper, write where you spent money and the amount. Categorize the spending. See if you can find just how much money went somewhere that could have cost you less or was unnecessary. I bet you’ll find at least $100 that was spent unintentionally, and it’s very likely more than that.

The TREAT for yourself is being more financially secure. It’s having the money for the necessities. It’s being ready for an emergency, but still being able to make your mortgage/rent/utility payment.

I wrote most of this post 5 months ago, but I’m going to finish it now for the longevity of what we’ve done with these rental houses. The house has been rented since September and was vacant for 43 days. She agreed to a shorter lease term, so it goes through June 30, 2026.

The tenants in this house moved in 3 years ago. They were good tenants. They hardly asked for things and were super understanding and gracious when we had the HVAC go out (granted it was their lack of filter changing). They brought a dog into the mix and tried to hide it (not well), and I eventually called them out on it to let them know they don’t need to keep finding a way to hide the dog every time I need to come over. They added a 3rd person on to their lease about a year ago. The only major issue I have is they smoked inside the house. I knew it constantly because (just like with the dog cover up) they weren’t great at hiding their evidence.

Earlier this year, I reached out that if they want to renew, I’d be raising their rent from $1200 to $1275. The girl who usually handled the bidding called me and explained they had intended to move to Georgia for a job, but they weren’t ready to move as fast as the end of the lease. I told them they could do month to month for a little, and we agreed to June 30th. I knew I had another lease ending July 31st, so I thought it would work out well that we could address the one house before the other became vacant. In theory. They ended up asking for another month, and we were busy with summer things at the end of June that I agreed, even though it meant two houses were vacating at the same time. I told them that I wouldn’t be able to extend any further though because it’ll be hard enough to rent end of August time frame, let alone into September or later.

On July 29th, they asked me what time they had to be out on the 31st. I said 5 pm. The next day, they asked me if they could have a couple more hours, but I let them know that I had already booked someone to meet them for their keys at 5 pm, and that’s all I could give without it costing them more. I was out of town for this vacancy and asked a friend to be my property manager to walk the property and gather the keys.

They ended up being out and basically cleaned up by 5 pm. I was impressed. The fridge was completely wiped down. The bathrooms were in rough shape, but overall, it was one of the cleanest vacancies we encountered.

THE TURNOVER

We had to have a friend go out to get their keys because we were out of town. I tried to get them to stay until the weekend to make it easier to move, and so that I could be the one to meet them (not that I said that), but they didn’t want to pay the per diem for that option. They ended up keeping their timeframe perfectly.

The turnover took longer than I had planned. I was working part time without a real ability to give up those hours because I had things that needed to get done, and it was summer, so we had 3 kids in the mix. Not to mention, we basically had back to back trips planned for the end of the summer. Overall, it was a learning experience.

We spent about $800 on supplies for the turnover, outside of the carpet, which was about $3,000. With the extra cleaning of the bathrooms and the time it took us to clean and paint the property, we kept their security deposit of $1,200. We could have gone after them for more because of the smoking (I have pictures from when I was doing work in the house of ashtrays with used cigarettes upstairs in the house), but it’s not worth the effort and cost.

FLOORING Before they moved in, we had ripped out the carpet and installed luxury vinyl planks (LVP). Conceptually, the goal was to not need to work on the floor anymore. We had limped along with the carpet, especially in the living room, since we bought the house, and it just wasn’t worth it anymore. We did the install over two days back then. Now that they were out, there were several gouges in the floor and the floor was separating in some spots. Mr. ODA handled fixing the separation, and he replaced a few boards that were damaged and noticeable.

The kitchen floor was so dirty and it’s the first thing you notice when you walk in. I spent many hours on my hands and knees cleaning out the grout to make it look less dingy. I didn’t get it perfect, but it was fixed. It’s one of those things that no one will ever know just how much time I put in for it to not be perfect, but it would have been so much worse had I not done anything.

BATHROOMS The bathrooms were a wreck. I’m so lost when I walk into homes and the bathrooms are dirty. Do you want to sit on that toilet or clean yourself in a shower that is dirty? It seems counter productive to me. Mr. ODA had to take over with Bar Keepers in one of the bathrooms to remove the staining and soap scum build up, but we did pretty dang good.

I wish I had a ‘before’ picture easily available to show, because this picture does not do justice to how much time went into this tub.

CARPET We bought this house 9.5 years ago. The carpet was questionable when we bought it. We would have it professionally cleaned between tenants, and it would look amazing compared to what we saw at first, but the stains would always come back because they were deep in the pads. Before these tenants, we ripped out the carpet in the living room area and laid LVP because the living room was especially bad. Well that still left carpet in the 3rd floor bedrooms, hallway, 2 stairwells, and the whole basement. With the smoking by the tenants and knowing we had far surpassed the useful life, we went ahead and planned to replace the carpet.

There were delays in getting the appointment scheduled and making it all work. The lady who did the measure appointment said installations were 3-4 weeks out. That was disheartening because we had already lost over a week by having back to back trips at the beginning of August. We went into Home Depot to find something else. I ended up settling on something because it said 5 day install. Well, 5 days came and went. I was so frustrated that I had settled on this worse-off carpet just because I wanted to meet a timeline, and now the timeline meant nothing. Then suddenly, we got a call and they said “can we come install the carpet today? We’ll load it now and be there within the hour.” That they did. They installed it in 7 hours and that was behind us.

PAINTING This took forever. Two big stairwells really take a lot out of your time. Every surface needed to be painted just to work on covering the smoke smell. While we didn’t spend a lot on the turnover (outside of carpet), this house just took so many hours from us. We painted every wall. I painted some of the trim that had not been previously painted, but it was in rough shape. We also had to repair several walls because they had sticky things to hold shelves up and they didn’t remove it.

MISCELLANEOUS THINGS DONE

Replaced the dryer door handle (that had actually broken off before they moved in, and I thought this was an insurmountable task to fix/replace… well, it was a $6 plastic piece off Amazon that popped right in. Welp.)

Replaced window screens that were worn away and in disrepair.

Cleaned out all the air filter areas for the HVAC.

Replaced all the rusted and broken floor vent covers.

Installed a doorbell because they installed a Ring, took it with them, and didn’t put the old one back in.

Replaced the cabinet knobs (it appeared someone had spray painted over the original 90s brass with something to mimic a stainless steal look, and they were all worn and chipped).

Wiped down the cabinets and walls to get them to be less sticky. Wiped down all the doors, light switches, and outlets because they were so gross.

Replaced the broken light in a stairwell that they broke on their move in (and reported).

Repaired some ceiling areas that were damaged due to a roof leak before the HOA replaced the roof.

Replaced a shower curtain rod that they took with them instead of leaving behind.

Painted the front door. It looked like someone had taken steel wool to it to clean it.

LISTING TIMELINE

We got the property to “good enough” stage so we could get it listed. There was still things to get done, but we didn’t want to wait until it was perfect and lose interest as we got further into the school year under way.

We listed the property at the end of August for $1,400. I thought we were golden. The location of this property is excellent, and it’s on a bus route that takes you downtown and to the outskirts of the city for shopping. There were two other listings for $1,500. It didn’t move. I didn’t even get productive bites.

I dropped the price to $1,350 two weeks later. I did show it a few times. I was happy that when I made appointments, people actually showed up, but they didn’t qualify. Mr. ODA hosted an open house and had one person come through. That one person was our person though. I removed the listing two days after the open house and we have it rented at $1,350.

I offered her $1,325 for an 18 month lease or $1,350 for a lease through June 30th so I could get back on a Spring schedule. She agreed to the shorter timeframe. She was looking for a quick move because her landlord was selling her place. Our house seems too big for her needs, so I wouldn’t be surprised if she leaves at the end of June and we need to find a new tenant.

SUMMARY

We knew a September listing was going to be tough, but I didn’t expect it to be that tough. When we had a property managing on this place, they always took 5-6 weeks to get it rented and it drove me crazy. At least 3 weeks from start to finish isn’t terrible, but I’m definitely used to it moving faster. It’s also nice that had my tenants stayed, we’d be getting $1,275, and now we’re getting $1,350. Thus far, this lady hasn’t asked for much. We struggled with the utilities getting into her name. For some reason, the utility companies credited my accounts and billed it directly to her, so I didn’t even need to work on capturing that money from her, which was nice.