There are many teachings out there that talk about a safe, sustainable, and efficient way to wealth being many streams of income. This diversifies and provides multiple avenues for growth, but also mitigates risk and protects your larger portfolio against any one stream failing.

Our financial portfolio meets those goals. Instead of having an emergency fund sitting in a savings account earning 0.03% interest (that’s literally our savings account interest rate, and that’s the ‘special’ relationship rate), our money is put to “work,” earning more money for us.

INDEX FUNDS

Probably the simplest and most common example of multiple streams is index fund investing. A quick read of JL Collins’ “The Simple Path To Wealth” will teach you that through index fund investing, you have an ownership share of every company the index fund covers. Some are matched to S&P 500 companies, some to International, some to the DJIA, and most to the “Total Market.” Mr. and Mrs. ODA invest in the “Total Market Index Fund,” through Fidelity, in our IRAs and taxable investment portfolio. By owning a small part of every publicly traded company, we own that many streams of income. Any one company going belly up will only be a blip on the radar of that index fund, and, over enough time, it will go up, and up a lot. This is as risk free of a true investment as you can get.

Being Federal Employees (Mrs. ODA no more, though), we both have access to the Thrift Savings Plan (TSP) for our 401k’s. The TSP provides a group of 5 index funds to choose from: Government Securities, Fixed Income Index, Common Stock Index, Small Cap Stock Index, and International Stock Index.

In times of market upheaval, we can ‘escape’ to the Government Securities fund, and pending a nuclear winter or alien attack, is guaranteed to be paid (TSP.gov). However, with this little risk also comes little reward, so it won’t grow fast. With index funds and a safety spot, our TSPs are about as low risk a retirement investment as you can have. Note that Index Funds through Fidelity or Vanguard (for example) and the TSP have the industry’s lowest fees on their funds, so we won’t lose our nest egg to management costs either.

REAL ESTATE

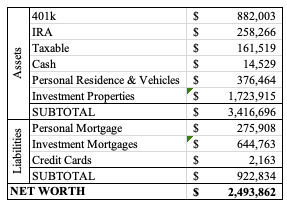

Outside of anything related to the stock market, we have 12 single family rental properties. Each of these houses operate as their own small business, with long term tenants in most of them (that have thankfully all been able to maintain rent payments through the pandemic). If one or two houses did lose their tenant, or have an AC break, or a roof needing replaced all at the same time, the other houses (businesses) can pick up the financial slack. A few of the properties are owned outright, so the lack of a mortgage certainly helps the whole portfolio’s cash flow. And actually, we did have to replace/repair multiple roofs and HVAC units at the same time in the summer of 2020! On top of the individual homeowners insurance we have on each house, we have a Commercial Liability Umbrella Policy covering anything above and beyond the individual policies.

DIVERSITY

We also have some money tied up in more actively managed mutual funds – investments we owned before we discovered index fund investing – and individual stocks. However, I can’t bare the capital gains taxes required if I were to sell them and shift that money over to an index fund. But – they’re there in case of an emergency.

That Federal job I mentioned – I’m lucky to have about as much job security as any W2 employee can have in this great nation. Through the shutdown a couple years ago, I had 2 paychecks delayed, but my rental properties made it so that I didn’t have to worry about our finances. Otherwise, a safe, consistent paycheck is something I can count on – with health insurance for our whole family that comes with an annual out of pocket maximum of only $10,000.

So we have a W2 income, 12 rental property small businesses providing monthly cash flow, and a slew of stock investments diversified across all markets. We have diversity that mitigates risk and shields us from small “emergencies” manifesting themselves as such.

We view “medium” emergencies as something that can be solved with a new credit card deferring needing to truly “pay” for our expenses until life gets back to normal. You’ve seen a past post discussing our perspective on strategic credit card usage (and the Chase cards specifically). Twelve to fifteen months of no interest on a credit card can get anyone out of a financial bind when emergencies hit. We haven’t found a reason to NEED this option, but know that it’s always out there if the perfect storm of bad luck were to ever hit.

For these “small” and “medium” emergencies, stocks could be sold before we would need to be faced with something like not being able to pay utilities, buy food, or get foreclosed on. We simply don’t view a “large” EMERGENCY cropping up with any higher than a near non-zero probability given the shielding and structure we have built out of our total financial portfolio.

I can’t fathom what that perfect storm would look like. Six months of expenses can easily be found in selling our stocks if all of our tenants suddenly stopped paying rent, for example. But if a pandemic isn’t going to make that happen, what would?

All this to say – Mrs. ODA and I keep very little cash liquid to cover our “emergency” fund. Outside of a couple thousand in our checking account to cover regular monthly/cyclical financial obligation fluctuations, we don’t have any dollars NOT “working for us.” Whether it be investing in index funds, contributing to IRA/401k, or paying down mortgages to eventually achieve more cash flow, we put all our money to work. We see the rewards of this strategy far outweighing the risk of encountering a debilitating financial emergency, and therefore don’t follow the traditional personal finance advice of keeping X months’ living expenses in cash handy at a moment’s notice.