We’re continuing our spring/summer of travel and activity, which is why there are fewer posts and lots more spending.

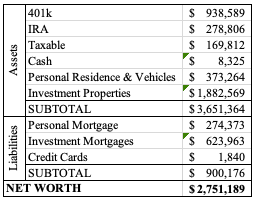

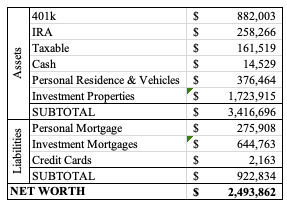

The stock market has increased, which has been the main factor in our net worth change. We paid $2,000 towards the mortgage we’re paying down, leaving a balance of $3,300. This mortgage will be paid off once all our rent is collected for July; it was pushed back a little bit because of the flooring replacement that occurred in one of our rentals, which is why our credit card balance is much lower than last month. We’re also still waiting for half of one property’s rent, which is the norm these days.

Utilities: $250. This includes internet, cell phones, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant.

Groceries: $518

Gas: $268

Restaurants: $165. Our credit card reimburses for many of these expenses; we received credits totaling $120.13 in the last month.

Entertainment/Medical: $1,093

Investment: $1,100

Insurance Costs (personal and rentals): $845

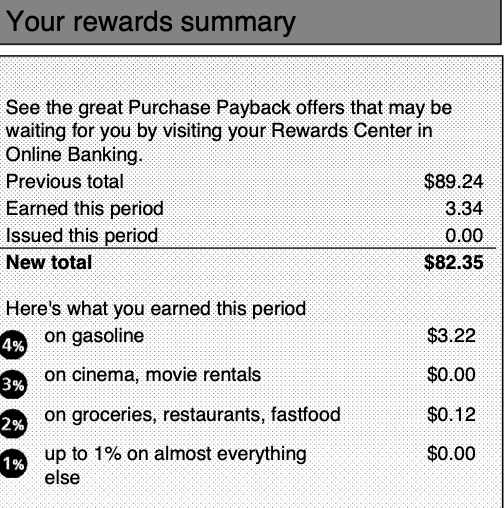

VIGILANCE ON CREDIT CARD REWARDS

Mr. ODA discovered that our PNC credit card rewards balance was decreasing, despite earning new rewards this cycle. He investigated further and noticed that we had been losing rewards for a few months now. PNC has a policy that they don’t issue their rewards until you hit $100 worth of rewards. Once we hit $100, PNC sends us a check in the mail. Since they send a check, we still receive paper statements, even though we regularly check our financial accounts online. Over the past few months, both of us checked the balance to see “ok, we’re nearing $100,” but didn’t put any more effort into knowing the details of the balance. Mr. ODA happened to notice that the statement didn’t make sense.

$89+3 somehow equals $82. There isn’t a single section on our statement or via our online account that identifies the loss of rewards Mr. ODA called PNC to ask for more details and learned that our rewards expire after 2 years, despite their policy of not issuing a check until you hit $100. They basically said, it doesn’t matter that your account is over 10 years old, or that credit has been used less in the last year due to the pandemic, or that they don’t clearly identify the expiration of rewards and just identify a lower balance. As a comparison, and I keep going back to Chase, but Chase changed up their reward categories to allow the consumer to earn more rewards during the pandemic (e.g., in addition to giving rewards in the travel category, since consumers weren’t traveling, they added grocery and home improvement stores as major reward categories).

The PNC customer service representative reinstated 60 days worth of lost rewards and issued a statement credit. We don’t want a statement credit because we no longer want to use this credit card, earning rewards that we’ll never be able to capture. If we use this credit card to use up the statement credit, that’s rewards that could be earned on a different credit card. Now Mr. ODA is fighting for the credit to be applied to our checking account or to have a check sent to us (which is the preference on our profile) and fighting for the reinstatement of the rest of the rewards lost.

Without PNC, we’re down to 4 credit cards in our regular rotation. We have 3 cards that we use for categories (gas, grocery, restaurants, travel, home improvement stores), and then we have the Citi Double Cash card that is for “everyday purchases.”

We paid $2,850 in extra principal towards the main mortgage we’re paying down, leaving that mortgage with a balance of $5,500. We had a $4k flooring purchase on another house that has set our pay off timeline a few weeks back, but we’ll still have that mortgage paid off in the next couple of months. We have a rental property that we purchased in 2016 that has flooring that’s at least that old. The carpet has long passed its useful life, and the linoleum in the kitchen and laundry room has started to peel up at the seam. Typically, we wouldn’t want to replace flooring while a tenant still lives there, but they’ve lived with this for almost a year, and they’ve been our tenants since we purchased the house. As a means of keeping the tenant happy, we agreed to replace the flooring in all the rooms except the bathrooms.

We had two of our tenants not pay rent by the 5th, as required by the lease. They’re the two that are typically late, and they’re typically not up front with telling us about it. We’ve said several times that we’re really flexible landlords, but we can’t be flexible if we’re not told what is happening. With one tenant, who had just recently irked us with a plumbing issue and being incommunicado, we didn’t even reach out for information. We’ve had enough of their antics and having to chase them for rent. So I simply sent them their notice of default letter, outlining all their rights as tenants as now required under COVID-related procedures. I received an email letting me know that they’d pay on the 7th. I love their nonchalant response, like they hold the power and will pay whenever they feel like it (hmm). For the other tenant that was late, she texted to say she’d be late with the payment on the 7th, and then on the 7th only paid part of the rent due. She said she was in a car accident and there was an issue with her sick leave pay out, but she’d get it to us when it got fixed. She resolved it on the 12th, although still without the late fee.

We were able to get the invoice on the HVAC replacement for one property, which meant we paid our partner the $3,288 we owed him, on top of his usual $2,167 that we pay out for him to pay the mortgages and then his share of the profits (since I manage all the rent collections).

OUR SPENDING

Our credit card balances are high for several reasons. The $4k flooring purchase; as well as the insurance for one of our properties that isn’t escrowed because we paid off that mortgage, which was $436; an expensive gift purchase that isn’t transparent in the cash and credit line items because that cost was split 3 ways (i.e., we received 2/3 of that cost back in cash, but it’s still reflect in the credit line); and our travel.

We booked a camp site for the end of the month that required payment up front. We just got back from a trip, which increased our spending. But I’ll note that when we travel, we’re not eating expensive meals. Our interest is in the experiences and activities, rather than exploring sit down local restaurants. Our food for 5 days cost us $161 as a family of 4. We also ended up only paying for 2 of the 4 nights in the hotel because the air conditioning was broken, even after they came to ‘fix’ it, and then, when I was checking under the bed to see if any toys or socks got left behind as we were leaving, I found a large, dead roach. We didn’t ask for any comps; one was automatically reflected in my final invoice without my prompting, and then when the manager was speaking to Mr. ODA about his stay, he volunteered removing another night.

We opened a new credit card to take advantage of the bonuses since we knew we’d have this travel and the flooring cost to meet the $4,000 spending threshold for their bonus. This credit card has an annual fee of $95 and no 0% interest period, which goes against our norm when looking to open a new credit card. However, the bonus can be transferred to our Chase Rewards Portal, where we can use it to book travel at 50% the cost. We also received a $50 grocery credit.

ROUTINE UPDATES

My husband and I cashed in the last of his savings bonds that we got as children, so that was an extra $735 that we brought it that wasn’t planned.

We paid about $6,074 for our regular mortgage payments. Several of our properties had mortgage increases due to escrow shortages. I haven’t figured out which I dislike more: planning for tax and insurance payments, or the large escrow increases that seem to happen year after year. I think it’s the escrow though.

Every month, $1100 is automatically invested between each of our Roth IRAs and each child’s investment accounts. I should also note that I don’t speak to other investments because they happen before take-home pay, but my husband maxes out his TSP (401k) each year as well, which I had also done when I was employed.

Our grocery shopping cost us $700. Honestly, I don’t even know how to explain that cost jump. I think it’s because my husband shopped some deals at Kroger and Costco, so we stocked up on some things that aren’t part of our routine purchasing.

We spent $200 on gas. Two trips to Cincinnati, our trip to Atlanta, and then more-than-usual trips around town.

$400 went towards utilities. It’s higher than last month because we paid 3 months of our cell phones, which gets us back on quarterly billing as a family. Utilities include internet, cell phones, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant. We still haven’t sought reimbursement from the builder on our electric bill, but this month’s bill was even less than the last month’s.

Our entertainment costs included baseball game tickets for our trip as well as two games later this summer, parking for the games this past weekend, a new shirt for our son, activities for the kids, and the hotel. This past month, we spent $650 on things I’d classify as entertainment related. I also included boarding for our dog ($100) in this total.

Speaking of our dog, he had his annual appointment (shots and the year’s worth of preventative medicines), and that cost us $500.

We spent $292 eating at restaurants and ordering take out. We utilized a Door Dash credit on one of our Chase credit cards, which was about $30.

But! I killed it with running errands this month and actually returning things that needed to be returned. I returned $150 worth of items one day!

We paid our State taxes during this period too. Between two states, that was $954. Also, anecdotally, I’ll share that we spent $6.40 to mail our Virginia tax return. We processed our taxes through Credit Karma, as we had done last year. We got through the federal e-file and moved onto the state filing, only to find out that if you’re filing partial states, Credit Karma doesn’t support it. I had to print 70 pages of our federal return, sign it, and ship it off to Virginia.

SUMMARY

Our net worth actually dipped this month. The stock market is the main factor in that, but the house valuation estimates are starting to level off and look more realistic as well.

Between our personal lives and our business life with these rental properties, we were sure kept busy. We expect the Spring months to be a busy time of year, and honestly it feels good to be active again. While we’ve loosened the purse strings for the summer months, especially after having done hardly anything for the last year, it was still a shock to see just how much we spent in these categories. But that’s the benefit of looking at your finances regularly. We can either choose to remain on course with our summer plans, or we can dial it back if we feel this was more than we expected.

Since we know we’re on top of our finances and have set up a healthy mentality when it comes to spending, we’re comfortable looking at this information once a month. If you’re currently developing these money habits, you may want to do these types of check-ins more frequently.

This month had a lot of money movement – tax payment out, stimulus check in. As I’ve shared before, we don’t budget. But you can start seeing how we’re pretty consistent on where we spend out money. This is because we have a spending mentality that we use to make each decision, rather than giving ourselves a ceiling in each category. I believe some may see a ceiling as a definitive amount to spend (e.g., if I’ve allocated $100 for restaurants this month, and by the last week I still have $75 in that budget pot, then I’m going to go spend it). If you know your long term goals and take responsibility for your decision-making, then you don’t need to pay close attention to each dollar.

With that said, my family came to visit for a week. It was our second’s first birthday, and my dad is helping us finish our basement. With 3 more adults in the house, we spent more than typical feeding them and eating at restaurants versus cooking after spending the day working in the basement. Mr. ODA and I share the same birthday, so we splurged for a nice meal that night. We actually spent about $300 at restaurants over this last month, but thanks to our Chase credit card, we received statement credits for $188 worth of these purchases!

We have also spent more on entertainment. We went to a winery and a brewery, purchased tickets for the local horse race season, and have done other activities now that the weather is nice. The pandemic and winter had our spending lower than our usual amounts, but I expect our spending to be more than it had been in these coming months. We’ve already put together our summer bucket list for travel.

We had all the tenants pay their rent on time, except one who eventually paid. Our rental income is $12,353, and we pay our business partner about $2,100 (we collect the rent and then pay him to cover the mortgages he holds and his half of the ‘profit’ after the mortgages are deducted from rent). We had to replace the HVAC in a rental. Luckily, this rental is owned with a partner, so only half the cost will affect us. We haven’t paid the bill yet, so that will hit next month.

We paid about $5,972 for our regular mortgage payments. We put an additional $5,000 towards an investment property mortgage, which now has a balance of $8,665. We also put $5,000 towards one of the properties that we have with a partner, which he matched, leaving that balance at $42k.

Every month, $1100 is automatically invested between each of our Roth IRAs and each child’s investment accounts. Our stimulus checks that we received for the kids went directly into the kids’ UTMAs.

Our grocery shopping cost us $539.

We spent $91 on gas.

$290 went towards utilities. This includes internet, cell phones, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant. We still haven’t sought reimbursement from the builder on our electric bill, but this month’s bill was significantly less than the previous months.

About $1300 was spent on supplies for the basement bathroom work. We registered the kids for swim lessons, registered our son for pre-school in the Fall, did more activities with the nice weather, and I made several gift purchases (current birthdays, baby shower, next Christmas (I like buying when I find something that makes me think of a person rather than a mad dash in the Fall to buy gifts)), so that was about $400.

SUMMARY

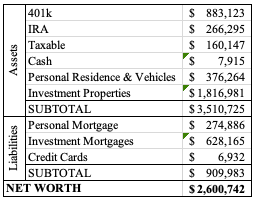

Our net worth has increased over $123k since last month due to our investment accounts and property values increasing. Our cash balance is starting to dwindle down to what we typically carry as ‘cash.’ And our mortgage balance is decreasing more than average due to our goal of paying off two of the mortgages that we’re carrying.

This one has been pretty easy, but we did have an interesting issue arise with the first tenant.

This is our largest house at 4 bedrooms and 1.5 bathrooms, and 1281 square feet. It’s a cape cod style house, so the upstairs has slanted ceilings, the half bath is not anything to write home about, and the HVAC struggles to work up there. The carpet on the stairs could really be replaced (but it hurts me to spend money on stairs because they’re soooo expensive compared to carpeting a room!). But the house has a huge fenced-in yard with a nice deck that’s a great selling point.

The kitchen was renovated at some point, so that’s held up well – and lets face it, who doesn’t choose baby pink knobs for their new kitchen cabinetry? But the plumbing and roof have been painful.

I’ve already told many of the stories about this house through other teaching posts, so bear with me if things sound familiar.

LOAN

The house is in Richmond, VA, and the purchase was very simple. We offered $109,000, and the seller countered with 112,500 and 2,000 in seller subsidy (i.e., closing costs), which we accepted. It was listed on June 22 at $119k, and we offered on June 25, so I’m actually surprised we got the contract agreed to so quickly.

Quick note here: after reviewing real estate contracts in NY, KY, and VA, Virginia wins. Sure there are several states that I haven’t ventured into, and this is an extremely small sample size. The paperwork is simple yet thorough, all while being in plain language. So if you’re needing a template to work off of, look up Virginia’s purchase agreement.

We settled on a 30 year conventional loan at 5.05%. We received a $200 lender credit since we closed on several properties in a short period of time. This is the house that we refinanced and received an appraisal of $168,000! We had already started with equity in the house because it appraised at $114,000 at closing.

INSURANCE

Interestingly, we couldn’t insure the house through the company that we had gone with because they have a 5 rental limit. Our agent was able to quote us through another company though, so our process appeared seamless. However, the quote was much higher than we anticipated. We went through a friend to insure it, but shortly after closing (literally a week), we were able to find an even cheaper option – that was awkward.

THE NEIGHBORHOOD

Not a category that usually gets mentioned. I discussed the neighborhood of the one house we sold already, which was because I didn’t realize it was in a higher-than-average crime area that tenants honed in on. But this neighborhood is worth mentioning.

Rentals aren’t prevalent here. In fact, many of the homes are the original owners. While working on the house when we first purchased it, the neighbor across the street approached me. He as-politely-as-possible threatened me that this is a nice neighborhood, that everyone keeps up their property, and that they don’t want any trouble. I assured him we have good standards as landlords, and we haven’t had any neighbor complaints for any of the tenants we had in our houses.

The location also comes into play for our first tenant.

TENANT #1

This house is under a property manager for 10% monthly rent.

As with most of our tenant searches, no one fits perfectly into our requirements. We offset this by a higher security deposit or having another signatory on the lease. We had two prospective tenants – one was a mother/daughter combo (an adult daughter) and both had bankruptcies in the last year; the other was a man and his family that had an eviction 7 years prior. We chose the one with an eviction. His application actually said that he “will also respect the property to the utmost.” Boy did he.

He first requested that the carpet be replaced. It was actually a reasonable request because it wasn’t the best. Here’s the carpet on the second floor. Old, bottom of the line padding; a gorgeous blue; lots of wear spots.

We decided to refinish the wood floors on the first floor because 1) he wasn’t moving in for two weeks, and 2) it would save us in the long run to put that investment into the floors instead of carpeting every few years (and risking someone completely ruining it before its useful life was up). It was $1850 and the company was able to start immediately and get it done before the tenant moved in (granted, it was the day he moved in, but it did get done). And the refinish turned out great!

He asked us for a screen door, but we said that wasn’t a necessity. He asked if he could install one himself. We agreed, as long as it didn’t prohibit our access (e.g., he can’t lock it, give us a key). This later becomes an issue because he locks it after vacating and we need it rekeyed.

This tenant had a few late rent payments and struggled with paying rent on time, but overall he was a good tenant to have. He took care of the property and let us know when he ran into issues (it’s amazing how many people don’t tell us of a problem in a timely fashion).

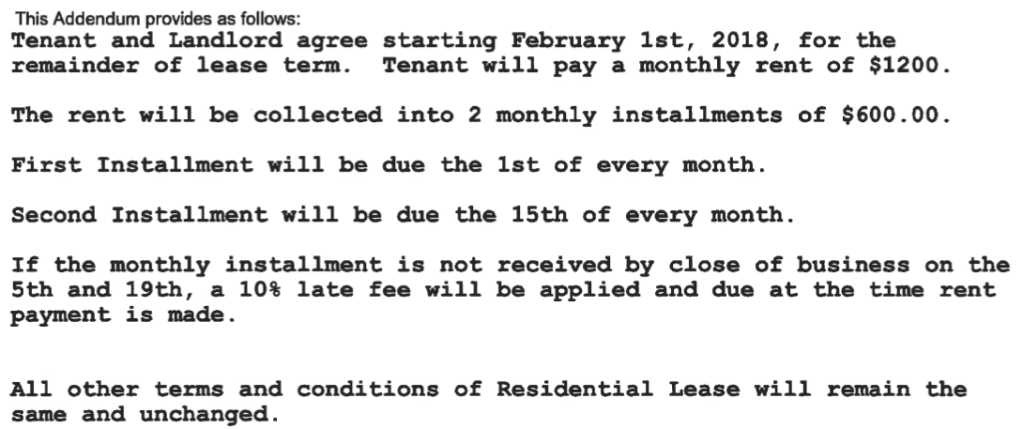

Just as we did on House 5, we offered this tenant the opportunity to pay rent in two installments each month. His rent was $1150 from August through February. He took the opportunity and we executed an addendum to change the rent to $600 twice a month. Again, it’s an inconvenience to us to collect two rent payments, but it theoretically should save the tenant money if they’re constantly in a position that they owe late fees (if he usually pays $1150+115=1265, then 1200 is a better position).

And then the fun happened!

I was at WORK one day, answered my work phone, and someone on the other end asked to speak to the owner of [this house’s address]. I barely used my work phone for work calls, so to receive a personal call on my work phone was very surprising. I informed her that I was the owner. She then went on to ask me questions about the tenant occupying the residence. I couldn’t answer a single question – hah! I let her know that I really didn’t know who was living there or the status of the home because I have a property manager. She was very nice and understanding, and she called my property manager.

She was with the school system. Apparently, our tenant had moved into the City public school district, but kept his kids in the adjacent county school system. It was April. I thought it was ridiculous that the school system would investigate this with 6 weeks left of school, but technically, he was in the wrong. And get this – he blamed me for it! Our nice tenant turned on us and went crazy. He claimed that he could just walk away from the house …. honestly I don’t remember his reason for it, but somehow he thought he had a case.

Virginia has a wonderful statute that says if the house is vacant for 7 days, the owner takes possession without any court interference. There’s also a statute that says we can’t collect double rent, and we need to be doing our best to rent it out if given notice. We tried to keep communication lines open with the tenant, but he was silent. We had told him that we were willing to release him from his lease obligations if we found another tenant, which we did. He was responsible for May’s rent and late fees, and we would have a new tenant move in June 1. We also informed him that he would be responsible for the leasing fee associated with finding a new tenant, which was basically considered the ‘lease break fee’ and is fairly generous ($300 instead of a standard two-months rent that’s typically seen as the fee). It kept going south from there.

On top of the rent owed, he had several lease breaches – room painting (clarification: rooms are allowed to be painted as long as it’s a neutral color or painted back to a neutral color before vacating), wall patching and painting, house cleaning, mowing, re-keying, and utilities since he turned them off. By mid-June, he still owed us $874.76. We made an arrangement with him that he’d pay a certain amount each pay check, but he failed several times. We finally threatened to take him to court, which would affect his credit score and increase the balance owed since court fees would become his responsibility. Since he had been working to rebuild his credit since his bankruptcy, we thought this would light a fire under him.

We went to court.

Court also added a 6% interest charge on the outstanding balance, which now included the $58 court fee.

It took him over a year to pay the balance. By the time the court judgment arrived, his balance (after paying $50 here and there was $660. The court doesn’t put a timeframe or process on the judgement, but leaves it to the two parties to determine the payment schedule. He didn’t adhere to it well, but we did eventually get the whole balance paid. Mr. ODA also took this opportunity to have fun with calculating interest payments on a declining ‘principal’ balance that isn’t getting payments on a predictable schedule!

TENANTS #2 & #3

These tenants were/are much easier. The second tenant in the house had several large dogs, but we didn’t see any damage to the house. She eventually broke the lease to buy her own house in November 2020; we can’t fault someone for wanting to take advantage of low interest rates! She gave the appropriate amount of notice, but the lease was going to be broken as of 10/31, which isn’t a great time to have a rental come open. She ended up being very gracious with the situation, paid us one month of a lease break fee, and we kept her security deposit.

Right after she gave us notice, we had an old tenant reach out to us. They had moved back into town (I’ve mentioned them several times) and asked if we had a 4 bed/2 bath house available. Amazingly, we did. We showed them the house and they signed a lease within a few days.

Since turnover was fast, and I didn’t really know the status of the house, I didn’t get a chance to paint the house. All the rooms had been white except for the one room that I repainted after the first tenant had painted it lime green. The house really needs a whole paint job, and so I offered her an incentive. If she wanted to paint any of the rooms, she could knock $75 off the rent per room. So far she’s painted three rooms.

MAINTENANCE AND REPAIRS

The plumbing in this house has been horrendous. We had the tub snaked as soon as the first tenant moved in ($150). We then had issues with hot water, which required several adjustments to the water flow rates to coincide with the tankless hot water heater ($325). We had the upstairs toilet serviced ($120). Then a year later, we had to service the hot water tank again ($570). Tenants had complained that the upstairs sink drained slowly. We had attempted to snake it and fix it several times, but it never seemed to work. We finally just bit the bullet and replaced the plumbing – from the second floor to the crawl space. That work and the drywall patching cost us $1563.

Then there’s all the roof work. Shingles had flown off during a storm, so we had those replaced ($350). We also had a leak in the flat roof over the laundry room. We had a roof guy come out, and he said the roof hit its life expectancy. He replaced the pitched roof ($4135), and not the flat roof. So we’ve still had issues there that will need to be addressed.

SUMMARY

That sounds like a lot of money, but we’ve owned this house for 4 years now with our rent being double the mortgage (slightly better now too with the recent refi). When purchasing properties, any good investor is going to build maintenance and capital expenses into their numbers that determine if it’s a worthy investment. Rent cash flow wins out, and all the rest is just the cost of running our business – not to mention the $60k of appreciation we have on paper in just 4 years. It’s also worth noting that these things took up about 10 days worth of action from us over those 4 years, so most months, we just collect the rent with no other action required from us.

No property is going to be perfect, and this business relies on people, the tenants, to make the business profitable. No path will take a straight line, and being flexible to the ebbs and flows of rental property investing help make it fun too!

This little house has been made home by two families. It’s a 2 bedroom, 1 bath that is 719 square feet. While there have been a few issues with the house, it’s been pretty easy to manage because of the tenants taking great care of it.

I feel like the bathroom’s blue tile, patterned floor, and that peek at the door knob exemplifies the age of the house.

The first thing we did was remove this prison-like wall mounted sink and install a new vanity from Ikea. During my installation of the vanity, I had a good scare. The house’s orientation yields to using the back door more than the front door (and the fact that the gate at the front of the yard was padlocked and there’s no concrete walk to get to the front door). Someone knocked on the back door, but I ignored it. Then that person went to the front door (through a side gate) and knocked there. That’s incredibly persistent of someone who shouldn’t know anyone’s here. Then he went to the back door and knocked again. I panicked. I called the non-emergency police line, and two officers came out. The man had left by the time they got there, but the officers knew exactly who it was. There is a man who lives around the block that has suffered multiple strokes, but he likes to mow everyone’s grass, so he was looking to see if he could mow ours. While innocent, I still won’t be answering any doors while I’m working on a house alone though.

LOAN

We locked the loan at 4.95% and 0 points. We also received a $200 credit in closing costs due to closing on several houses in a short period of time. Our attorney also lowered their fee from $395 to $350 due to several closings. It never hurts to ask if there’s a discount, especially when we’re a multi-repeat customer!

We closed on the house in June 2017. The purchase price was $63,500, and we put 20% down. We paid off this loan in January 2019.

TENANT SEARCH

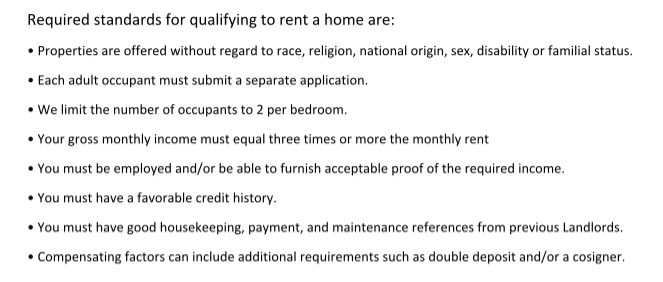

We listed the house for rent through HotPads, Zillow, and Trulia. We received a lot of interest. After setting up showings for another house, we learned to do more of an “open house” style showing. It’s amazing how many people confirm a showing time and then don’t show up. I first sent everyone who contacted me an “Initial Interest Form.” It was used as a first-pass look at their income, credit, and whether they disclosed a felony and/or eviction. I still told them about the open house schedule, but the future use of this form will be to weed out non-qualified people before we set up showings.

On the form, we list our standards.

I shared in the email when I sent the form that I would be at the house from 3-5pm on a Saturday for them to come see it. If they told me they couldn’t make it, I responded that I would make another time available pending the results of this open house.

Based on the interest forms received and being one of 3 couples to show up, we selected a couple that was most qualified. They requested to move forward with an application. We utilize SmartMove, a tool we found through Bigger Pockets, to screen our tenants. This process allows the tenant to provide personal information directly to the website, pay the entity directly, and eliminates us as a middle man. We also share that the application fee is non-refundable, and that’s why we give an Initial Interest Form to be filled out first, which is their opportunity to disclose any information that would disqualify them, causing them to ‘waste’ their application fee.

In our case, the background and credit check revealed that one of the individuals filed Chapter 13 bankruptcy. Upon further research, Chapter 13 is used to restructure debt. It wasn’t that she had delinquent accounts, and it appeared after asking her to explain, that this was a proactive approach to managing her debt from a divorce than an inability to pay debts. Since they had already paid their two application fees, we felt we’d take on this risk and rented to them. To mitigate our risk, we required 2 months of rent as the security deposit.

They lived in the house for a year before he graduated grad school and moved out of the area. However, at the same time, she had a family friend looking for her own place. We ran her background and credit check, and we were able to approve her easily. She took over their lease term in the Spring of 2018 and has been there ever since. We haven’t raised her rent since lease inception because at $795, it’s over the 1% Rule, and it’s full cash flow since the mortgage was paid off 2 years ago.

Even better, the couple that moved away from the area came back recently. They reached out to us for a bigger house to rent, saying they had such a terrible experience with their last landlord and would only rent from us again. We were actually able to accommodate exactly what they needed, and now they’re in House 7. While at this time I haven’t discussed our 7th house, I did mention their story in the Tenant Satisfaction post.

Treat your tenants fairly, and even give a little where you may not want, and it’ll make your life much easier.

MAINTENANCE AND REPAIRS

The house has a stackable washer and dryer, but it’s actually on the exterior of the main building in a little closet-type addition. It is unfortunate that an individual needs to go outside the house to do their laundry, but I suppose it’s better than having no hookups and going to the laundromat. Remember, the house is only 719 SF! Well, that little closet wasn’t well insulated, and in February 2019, we had a very cold two weeks where we endured several pipes bursting or freezing across our rental portfolio. The washer line froze. The fix was just to wait for the thaw, but we did add insulation to the closet to help prevent it in the future. Later that summer, the washer actually stopped agitating, and we replaced the whole stackable unit. The frustrating thing about stackable units – even though the dryer was perfectly fine, it’s all one unit so we had to replace the whole thing.

The furnace drain line was frozen in January 2018, so we had a plumber thaw it. It happened two weeks later again, and so the plumber installed heat tape around the drain line and sealed it.

We dumped new gravel in the driveway area. The gravel had become muddy, and we saw it as an easy fix to make the tenant happy and improve her experience. Plus, she said she was going to do it, but we felt it was our expense to incur, not hers.

We’ve had long term plans to replace the bathroom, but the contractor we met with in October still hasn’t given us an estimate. It’d also be tricky since the house only has 1 bathroom and she has a toddler living there too. The tub was painted before we purchased the house, and it hasn’t held up to the last 4 years of use, so we see the benefit in fixing up the bathroom, but we just haven’t been able to tackle the logistics yet.

Our tenant pays us every month and doesn’t ask for much. She’s made it her home, which is a good sign from a tenant. Our cash flow being $795 every month (minus semi-annual taxes) with very little repairs and no mortgage is a great scenario.

When we purchased the majority of our investment portfolio in 2016/2017, primary mortgages with excellent credit were sitting around 3.5% and investment property mortgages were about 4.5-5%. We thought these were amazing rates. Fast forward to a once-in-a-lifetime pandemic. A new baseline for low rates is created: We closed on our primary residence in November 2020 at 2.625% with nothing special about getting that rate.

Let’s go back to early pandemic days in the spring of 2020. Mr. ODA is always watching the market, but was particularly interested in the mortgage interest rates because we were coming up on the 61st month on our primary residence’s 5/1 ARM. Just a couple of months into the pandemic, we decided to move, so the ARM refinance (refi) became moot. But since rates were so low, he looked into refinancing our investment properties.

There are a few caveats. With the first company, we couldn’t refinance loans that had a balance less than $100k and be able to maximize the pricing structure they advertise so proudly ($0 closing costs). There was also an investment property fee, and took a long time for both of these to close.

As with the original loan, you’ll want to weigh the financial cost of refinancing against what the new rate will save you. When we looked at the variables, only 2 of our loans were worth pursuing a refinance.

In 2020, we refinanced House 9 from 4.875% to 3.625%. Our monthly payment went from $778.80 to $674.55.

The original loan amount on this property was $110k originated on 9/22/2017. We had paid it down to about $105,800 (shows how slowly the amortization schedule works for you in the early years), but with the closing costs rolling into the new loan (and cashing out $2,000), the balance became $111k. Eek, seems counterintuitive to refinance to a higher balance, but it’ll save us in the long run. We have greater cash flow each month with the lower mortgage payment, a larger percent of the monthly payment goes toward principal vs interest (amortization schedule again!), and we’ll save ourselves over $9k in interest over the life of the loan, if we make no additional principal payments.

We refinanced through a “zero closing costs” type entity. However, there are stipulations to what counts as $0, and investment properties aren’t exactly that. We had to pay an ‘Investment Property Fee’ of $2,358.75. The company paid the closing costs (e.g., credit report fee, title fees, recording fees) worth $548.91. We paid our prepaids, but also received a lender credit of $300. Essentially, we paid a slightly higher rate than the market would offer because the company rolls its closing costs into that rate, akin to paying points or receiving lender points to shift your rate up and down.

Mr. ODA initiated the refinance through an application in the beginning of March. We were quickly informed that we wouldn’t even be assigned a loan officer for two weeks. At the end of those two weeks, we were told they still didn’t know if they could move forward with our refinance. A week later, Mr. ODA followed up, and they had approved us to move forward. We were patient through the process, but it wasn’t until mid-May that we finally closed (in a parking lot, under a tent = pandemic closing #1!).

We rent this property for $1,280 and pay a property manager 10% of that. Minus the $674 mortgage and we’re still sitting quite pretty. While we reset the payoff clock by 3 years by starting a new 30 year mortgage, the extra money working for us in future years will far outweigh the costs of refinance.

In January 2021, we refinanced House 7 from 5.05% to 3.375%. Our monthly payment went from $664.31 to $559.34.

Our loan balance was $85,616, and the closing costs of $3,108 were rolled into the new mortgage. We also cashed out $2,000, so our new loan amount was $91k. The $2,000 was the most that could be cashed out during the refinance; we chose to take the cash out because we could make that money work elsewhere (e.g., pay down a mortgage with a higher interest rate). Even with the higher loan amount, the interest rate is so much lower that we’ll save over $15k in interest.

An appraisal was required as part of the refinance, which is how we learned that the house that we purchased for for $110,500, is now appraised at $168,000!

So, we rent it for $1,200 and self manage but only have to pay a $559 mortgage now? HELLO cash flow!

This closing was done at our kitchen table in KY through a VA-based loan officer. Mr. ODA initiated this loan in November, and we closed in January. A notary came to our house to go through all the paperwork, but it was all wrong. I enjoyed the “we never make mistakes” type of response from the Title company, and I pointed out that their paperwork did not match the lender’s paperwork that we had sitting at the table. Since the closing was at 6 pm, it was after hours for everyone and we couldn’t get an answer quickly, so we sent the notary home. We spoke with the loan officer an hour or so later and pointed how how each closing document had different numbers on it, and she went to work fixing it.

Theoretically, every investment property we own could’ve benefited from a refinance. And we would have with the “zero closing cost” company over time without their own pandemic policies getting in the way. If the loan amount was less than $100k, they would make you pay the closing costs AND would arbitrarily add 0.375% to the advertised rate. BUT, they wouldn’t let you pull equity out as cash to get the loan back up to $100k. So, that crushed our dreams a bit.

With options limited to “traditional” lenders’ pricing structures, we had to evaluate our future goals for the property and where the loan balances and rates already stood. Not to mention, there’s the time and complexity that comes with refinancing while hoping rates continue to stay low.

The lender we normally use has closing costs around $3k. This means that with the extra principal proportion and smaller monthly payment resulting from a refi, we need to balance against $3k to determine how long it will take to break even. Properties with small balances and properties with decent rates (mid 4%) would take longer to break even. Since we pay down our mortgages relatively systematically to achieve greater portfolio cash flow, some of our 30 year loans won’t be around for 30 years. And what if we wanted to sell the property to ‘1031’ to a different one? Our portfolio also has 15 and 20 year loans with great rates that wouldn’t be beneficial for us to pay to lower that rate.

There are a lot of moving parts when deciding whether or not to refi, and its very rarely free, especially with rental properties. But if the numbers work, it should be a no-brainer to pull the trigger and make it happen. Your future self will thank you!

This was a mess. I learned my lesson to research each property individually and not to make any assumptions. I also learned my lesson to hold true to our standards and expectations for a renter. We owned this house for a year and a half, but we learned a lot about tenants and the selling process. Hey, every struggle is a learning opportunity for next time, right!?

Mr. ODA showed me House 6 first (5 and 6 closed at the same time, and on my numbering list, this one came second… so try to overlook this awkward numbering!). I researched the area and the house’s history in detail, and I decided that it was worth pursuing. Very shortly after that, he approached me about House 5. The house was in better condition than House 6 and was literally only half a mile away. I assumed it was in the same neighborhood. I was wrong, and that’s where things went downhill fast.

LOAN

This house was so cheap that we needed an exception approved to get a loan. The purchase price was $60,000, which means a loan with 20% down is $48,000. The cutoff for even approving a loan with our regular lender is typically $50,000. Since we were below that threshold, we were ‘penalized’ by the rate.

I covered the closing snafu in the House 6 post, which also highlights the decision-making on the loan terms. Since this house was below that $50k threshold, our options were: 5.125% witha $200 credit or 5% with no credit. The higher interest rate would cost us an additional $1300 in interest, which isn’t offset by the $200 credit, so we chose the 5% rate. Hindsight: If we had known we would sell it just 18 months later, the credit would’ve been the better choice!

We purchased the house in July 2017. We immediately started aggressively paying towards the mortgage since it was the lowest balance and the highest interest rate.

We rented the house for $775, which far exceeded the 1% Rule.

WORK ON THE HOUSE

We did a lot of work in the yard. Here’s what the house looked like at some point before we owned it. It’s cute!

While it was under contract, the house sat vacant, so there were a lot of overgrown bushes, flowerbeds were filled with debris and no remnants of flowers having lived there, the lawn hadn’t been cut in a long time, and the tree in the front left had been removed at some point, leaving behind a mound of a stump and mulch that also collected debris. It’s a shame, and I kind of wish we had brought this little 2 bed/1 bath house back to life like it was in this picture. But I digress. Although this picture shows that the previous owner took care of the property, and that’s what attracted us to the purchase.

The floors were in immaculate shape, and the kitchen was quaint, but in decent shape. We purchased a new refrigerator before we could list for a tenant.

The bathroom needed a lot of help, but we didn’t want to overhaul it. The medicine cabinet wasn’t working anymore and the glass was cracked, so we wanted to replace it with just a mirror that covered the old medicine cabinet hole. Interestingly, we found a stash of 100s of razors behind it! (Apparently this is a thing from times gone by. You finish your blade and then you shove it behind the medicine cabinet for it to reside in the wall for all eternity.) We had several plumbing issues in the house. The drain pipe for the tub had multiple kinks in it, which caused the water to drain slowly and be more easily clogged. This would have been a major overhaul to get new plumbing installed in a way that was more direct.

The electric in the house was in need of work. We fixed quite a few electric-related-things while we owned it, but re-wiring the house was a major expense that would’ve come due in a few years.

TENANT ACQUISITION

The house was in great condition, had a big lot, was in a located close to the downtown area, and was on several bus routes (I even had a bus driver stop and ask me what the rent was on the house while I was working out front). It seemed like a great investment. We had several showings to qualified individuals….. who then went home, researched the house, and saw that it was in the highest crime area on Trulia’s crime map.

After sitting on the market for 5 weeks, we lowered our standards. There’s a reason you have standards as a landlord – it’s because if you select the right tenant, you’re saving yourself time, money, and headaches in the future. Here’s the email from our property manager. There are multiple red flags, and yet we gave her a chance.

The prospective tenant provided us with an employment verification letter showing that she had just started a new job, her most recent pay stub corroborating the employment verification letter, and wrote a decent introduction in her application. Between it being 5 weeks with no tenant and it now being mid-August (with it harder to rent in the Fall), we overlooked her credit score of FOUR HUNDRED AND FORTY EIGHT (448) and SEVEN (7) accounts sent to collections. I don’t recommend you do this. Oops.

EVICTION

This is the fun part to recount. It’s detailed, but I think it’s interesting.

RENT COLLECTION

She moved in August 2017. By December 2017, we already had enough issues that she wasn’t going to be trusted going forward. We’re very flexible landlords, and we’re happy to work with you on any issues as long as they’re communicated up front and timely (meaning, if we have to continuously reach out to you for rent, you’re not in a position to ask for favors).

We had allowed PayPal to be used to pay rent, but every month there was an issue. She either sent it in a way that incurred fees (after being told that she would be responsible for such fees) or it was sent in a manner that caused PayPal to hold the funds and not immediately release them. After December’s rent was late, the late fee wasn’t paid in full, and there were fees taken out by PayPal, we cut her off from electronic payments. Our property manager informed her that going forward, all rent had to be received by her office (either by mail or drop off) before the 5th.

Speaking of flexibilities – we noticed that she needed to send us rent based on each pay check, versus having all the rent money at the beginning of the month. She was paying us a late fee every month. Her rent was $775, and her late fee was $77.50. That meant every month, we were collecting $852.50, which really wasn’t necessary. We offered a change to her lease terms – rent was due on the 1st and 15th. As compensation on our part, rent would be increased to $800, split into two $400 payments. However, if rent was late, the late fee was now 10% of the late payment ($40) or up to $80 if she was late on both installments. She agreed to this, as it saved her money each month and set her up for success by being able to set up a system with each of her paychecks. We didn’t like that our relationship with the tenant had come to us hounding her over money, so we thought this was the best path forward for both sides of the party. Here’s the addendum to her lease.

And yet this didn’t change anything!! The addendum was signed at the end of January 2018. She paid February’s 1st $400 late. Then she didn’t pay February’s 2nd $400, and we had to reach out to her several times before even getting a response… after she also didn’t pay March’s 1st $400.

Our property manager filed unlawful detainer (eviction) with the court, and that got the tenant’s attention. She then had to pay the balance due, as well as the court filing fee, before March 30th (court appearance date) to dismiss the court action. She showed up to court with the cash to pay and then everyone just went home. You can’t evict someone who has paid in full, even if the process of collecting rent was unnecessarily burdensome.

And then came April. There was another story about a medical emergency and a new job on the books. We had agreed to a new one-time schedule for April’s rent payment, and she missed those deadlines and was incommunicado. We sent her another default notice on April 25. Note that this medical emergency was for her “husband.” This is the first that she had implicated herself that someone may be living in the house other than her and her son. She paid her balance owed on May 4th.

On May 8, she was given another eviction warning notice for lack of May rent (the 1st $400) and gave no response to requests for information on when to expect rent. After continued lack of payment after that notice, she was served with another eviction notice. On May 17, she was given 30-days notice to vacate the premises by June 17, 2018 at 5:00 pm. But then she paid in full and on time. We then changed her lease terms to state she was on a month-to-month basis and she would be granted 30 days notice when we (or she) decided to terminate the lease agreement. It was signed on July 16.

Guess what? She didn’t pay September’s rent. At this time, we also addressed her husband.

She was married when she applied, but we didn’t know. Justnow as I was looking back through our files to write this post, I saw that her pay stub she used for employment verification said that she was filing her taxes as married. I hadn’t seen that before. In all our visits to the house, there were always other people there. There was one man that seemed to be around 90% of the time. We overlooked it, but our lease did stipulate that anyone who stayed for more than 2 weeks was required to pass a background check and be on the lease. I strongly suspect that this individual was not going to pass a background check, which is why it was never disclosed to us that she was married and another adult was living there. Our property manager informed her that only she and her son were on the lease, and that if anyone else was living there, they had to be on the lease. She asked if we were referring to her mother-in-law visiting, our property manager said that it appeared to be her husband was living there, and then she ignored us.

We gave her our 30 days notice on October 5 to vacate, meaning she had to be out by November 5. Our property manager reached out to her on October 26 to see if she would be out earlier and set a time for key pick up. The tenant nonchalantly stated she wouldn’t be able to make it out by the 5th and she’ll be out by the 9th. Umm, excuse me, ma’am, but that’s not how this works. We held strong to the 5th and she lost it. Our property manager said that her lease is over on the 5th, and if she was not gone by then, the court fees would be her responsibility for us to get the court and local police department involved for her removal. She got angry and claimed that we didn’t handle the rental well at all, that we couldn’t charge her any court fees, and that she should charge us for not being able to use her tub because it was clogged (guess what on this one? The plumber removed things like a dental floss pick from the drain, immediately making it her fault (and at her cost) for said clog). She then said: “Lets just hope your (sic) as speedy with my deposit as you all were with terminating the lease.” I laughed out loud on this one just now. We should have terminated her lease an entire year before this discussion happened, but we kept working with her! Hysterical! Gosh, and to think this wasn’t our worst eviction process (more to come :)).

SELLING

A friend-of-a-friend was attempting to purchase a house in the same neighborhood as this house, and they ran into multiple issues causing them to walk away from other deals. Mr. ODA approached him with an opportunity to sell this house, which had similar specs to the one that they were pursuing. The buyer spoke to his wife and father about the deal and agreed to move forward. Of course, this deal was not easy.

The contract was ratified on October 31, 2018. We didn’t close until January 8, 2019. Our typical close time on our purchases is 4 weeks. We’ve done faster, and we may have done a bit longer if the time of month lined up better for our finances, but over 2 months was horrendous. Since our tenant was moving out on 11/5, and the closing was expected to be no later than November 30th, we didn’t pursue finding a tenant.

The appraisal was late being ordered, which was somehow allowable. Then it came in at the beginning of December at $65,000; our contract was for $68,000. We split the difference ($1000 from the buyer, $1000 from the seller, $1000 from the agent who was dual representing).

On December 18, our Realtor finally pushed back on the buyer’s side of the transaction to get things done. But it was Christmas time now. With so many offices closing for the end of the year, we weren’t able to get a closing date until the first week of January. The buyers were signing paperwork from Pennsylvania, which caused more delays because of having to send the paperwork back and forth for everyone’s signatures.

We sold in January 2019 for $67,000, after having purchased it for $60k just 18 months earlier. While this seems like a great deal, it’s not an automatic $7k in our pockets. You need to account for our closing costs from the purchase and sale (about $6,500), loss of rent for two months while trying to close the sale and the 6 weeks of no tenant when we purchased it, utility costs associated with vacant times, and costs to fix things around the house during our ownership. However, during that time, we had a tenant paying our mortgage (covering the loan interest and paying down the principal), and we were collecting more rent than projected because of her continued late payments.

1031 EXCHANGE

We made the decision not to pursue a 1031 exchange on this house. A 1031 continues to defer the depreciation to the next property, and it allows capital gains to be deferred. Based on current tax law, it can be done infinite times. However, there are extra lawyers and fees that come into play, so it becomes worth it when you have big dollars at stake, and that you have another property to purchase quite quickly after selling the first one.

The appreciation on the house was minimal given that it had only been 18 months since purchase, we had two sets of closing costs to add to the cost basis, and we hadn’t earmarked a place for that money to go upon selling. Plus, the cost of an intermediary would continue to eat into the “profit” versus tax paid, so we just went ahead and planned to pay capital gains taxes on it. Unfortunately, since we had depreciated the structure and the fridge over the prior 18 months, that paper money had to be brought back into the fold when calculating our taxes the following April. That’s several thousands of hidden money that is easy to forget about.

Depreciation is a great tax break when you own the property. The IRS assumes the value of your asset is being reduced by wear and tear and father time. This is true. It’s why if a landlord neglects the property and isn’t active with maintenance, renovations, and other replacements, the property will turn into a trash-heap in time. However, when you sell the property, you show the IRS that it in fact did not do that. If someone is willing to buy my property for more than I bought it for, then it obviously didn’t depreciate to a lesser value. I have to pay the IRS back for the depreciation assumptions that I was allowed to make over the time I owned it, plus pay the tax on the actual profits. Bummer, but logical.

In summary, we bought a cheap house and got a poor tenant. We had a TON of headaches with that tenant. We had to do a few house/yard projects over the ownership life of the property, but nothing worrisome and not already built into our numbers. Somehow, we made it work that eventually the tenant always paid up and then some (late fees). We made mistakes, we learned lessons. We figured out a set of streets to avoid for future purchases, learned how to sell an investment, and learned how to file taxes on an investment property sale. The story is fun to look back on. I’m glad we experienced what we did. But I don’t want to do it again.

This is probably our easiest house to own; the closing process was the hardest part here. We closed on House 5 & 6 at the same time, so I’ll cover the closing story here because House 5 has a lot else to be said when I write out that whole saga.

TENANT

This property has a property manager on it (10% monthly rent). She processed a couple of applications at the onset, and it took 2 weeks to find the tenant. The lease started on August 18, 2017, and that’s been the same tenant in the house to date.

Rent is $850 per month. She pays on time, and it’s usually early. She just asked about her renewal, and we decided to keep her rent at the same price, even though it’s the start of her 5th lease term. Our cash-on-cash return was ahead for the last 4 years, so even though our taxes have increased by $400 since we purchased the property, we decided it was best to keep the tenant than to get a few more dollars per month.

She asked if she could paint the kitchen cabinets that were definitely old, and we figured they couldn’t be made any worse. When a tenant wants to make your house their home, it’s most often is a sign they make taking care of the property their priority, and that they want to stick around for a while.

We had to treat the house for ants over this last year, but the only real issue we’ve had on this house is that the main sewer line had to be replaced due to corrosion and tree stump intrusion into the pipe. The poor tenant had her toilets backing up into her house. It was $4,000 to replace the line from the street to the house. Honestly, I expected it to be more.

LOAN DECISION

Option 1 – 20% down payment – conventional 30 year fixed at 4.95% with 0 points Option 2 – 25% down payment – conventional 30 year fixed at 4.7% with 0 points

We weighed these two options for our loan (purchase price of $66,000). The difference is an increase of $3,300 in down payment to save $5,700 worth of interest over the life of the loan. Being that we closed on several houses in a short period of time, we chose Option 1. Having cash for the down payments and closing costs of the other houses was more important than the marginal savings in interest of putting 5% more down.

We’ve been paying down this mortgage. At the time of our decision on which house to pay extra principal towards, this was the smallest loan amount with a relatively high interest rate. We started paying extra towards this mortgage in October 2020. To date, we’ve paid an additional $35,500 towards principal, leaving a balance of just under $14k.

CLOSING

During the Spring and Summer of 2017, we saw a lot of houses. We also made offers on a lot of houses that didn’t end up going anywhere, either because there was no consensus on a purchase price or because the home inspection was unsavory. We closed on House 4 at the end of June, walked away from a deal on one house due to a home inspection issue, and then closings on House 5 & 6 got lost along the way by the attorney’s secretary. We worked with a specific attorney who we had a great relationship with, and who eventually helped us with a difficult purchase (see the story for House 8), but this was a hiccup.

The attorney’s office let us know they were unaware of these two closings around June 20th (in reality, they just missed the ‘all clear’ to move forward with a title search, but they were definitely made aware of them), which left us scrambling. Our rate lock expired July 7, and the secretary responsible for filing all the paperwork was taking her vacation the week of July 2. Since she was taking the week off, our attorney scheduled a surgery of his for the same time, so the office was closed. She said she would find a way to make it work, but then we didn’t hear from her and had to reach out to the attorney himself. Here’s that email, outlining all the details.

It wasn’t until June 30th that our attorney confirmed he was able to hand off our closing to another attorney’s office. We had a few questions about their fees, since we explicitly stated that we didn’t want it to cost us more because we had to change our closing location, and then the secretary there got defensive and gave us an attitude. I was quick to call her on it, explaining that we just wanted to better understand the break down of what they put on our closing disclosure. She backed down, and then we had an awkward interaction a few days later when we showed up in her office to sign the paperwork. It’s interesting how people don’t understand that writing in capital letters can come across as rude. Turns out this other firm was an old law school friend of the attorney we normally use, and they worked out a favor among themselves on the fees to ensure they didn’t lose any future business from us.

At the end of the day, we closed on the houses on time and without costing us anything extra, but it wasn’t a stress-free path to get there.

Luckily, this house has been easy to manage and the tenant has worked out perfectly. Our rent at $850 far exceeds the 1% Rule; with a purchase price of $66,000, our monthly rent goal would be $660. Tax assessments have recently risen given that the local market has appreciated substantially, so we will consider a rent increase in the future. However, at this time, having a long-term tenant on a house that has hardly any issues is more important than risking a rent increase and having her leave.

When reaching out to a loan officer, there are a lot of options to choose from. I’m hoping to break down the decision-making here. I’ll share how we ended up with several different options, too.

Basically, it boils down to:

Put enough down to avoid paying Private Mortgage Insurance (PMI)

Don’t pay more than 20% unless there’s a decent incentive.

Don’t pick a loan term shorter than 30 years unless there’s a decent incentive.

Carefully evaluate any Adjustable Rate Mortgages (ARMs).

PMI

I broke down PMI in a previous post: PMI – Private Mortgage Insurance. We suggest doing whatever you can to meet the requirements to avoid paying this. The cost of PMI can be a couple hundred dollars per month, which is money that can be put towards the principal balance of your loan or other bills, rather than in the bank’s pockets. There are also hoops to jump through to remove PMI early, which may include paying for another appraisal on the house ($400-$700!).

LOAN TERMS

A conventional loan will likely require 20% to avoid paying PMI. There are some loan options out there that may allow a smaller down payment without a ‘penalty’ (e.g., PMI, higher interest rate), but 20% is the standard, and is usually required when purchasing an investment property.

There may be an option to put down more than 20% or you may think you can afford to pay a higher mortgage each month, so you’re interested in a shorter loan term. Unless there’s an incentive (e.g., lower interest rate, better closing costs), stick with the bare minimum to get the loan.

If there is an incentive, you’ll need analyze the math and your goals to determine if committing extra money to a higher down payment or a larger monthly payment is worth it. If you have extra cash each month, you can pay more towards your principal rather than pigeon holing yourself into a higher monthly payment. Plus, if you have more cash liquid, you may be able to purchase another rental property, which will increase your monthly cash flow.

While we evaluate the loan terms on every house purchase, I’ll share the details of the two most “unconventional” options we chose. Two things to note: 1) lenders add a ‘surcharge’ to the rate for it being an investment property, typically around 0.75%, which means the rates aren’t going to be the great, super-low, rates being advertised; and 2) the term “point” means a fee of 1% of the loan amount.

HOUSE #2

For House #2 (purchased in 2016), we were informed that if we put 20% down instead of 25%, the rate would increase 0.25% on average. If we assume a 30 year conventional loan, 20% down at 4.125% equates to about $69,700 paid in interest (assuming no additional principal payments); 25% down at 3.875% equates to about $60,800 paid in interest. By putting an additional $5,850 as part of our down payment, we saved about $9,000 in interest over the life of the loan.

Once we determined that we’ll put 25% down, we then had to figure out the appropriate loan length. On this particular offer, 30 year amortization wasn’t an option for us because we would have had to pay a point to get a competitive rate. We chose a 20 year amortization because the house already came with a well qualified tenant, we didn’t expect a lot of maintenance and repair costs due to the house’s age, and we didn’t have an immediate need for a higher monthly cash flow based on our place in life at the time.

While our long term goal was to have rental property cash flow replace our W2 income, this house was early in our purchasing. At the time, we were focused more on paying off House #1 (higher rate and a balloon payment after 5 years). Frankly, we didn’t truly understand the power of real estate investing at this time, and didn’t know how much it would accelerate the timeline for us to meet our goals. By decreasing our loan length, we increased our monthly payment, but also lowered the total interest paid over the loan’s life by over $22k. Since more of our monthly payment is going towards principal reduction than had it been a 30 year amortization, this loan isn’t on our priority list to pay off early.

HOUSE #3

For House #3, we evaluated the rate sheet for the loan term, interest rate, and down payment percentage again. This house was purchased a few months after House #2, so those rate decisions were fresh on our minds. We were quoted several options: 1) 20% down at 4.25% for 20 or 30 years, 2) 25% down at 3.75% for 20 or 30 years, or 3) 25% down at 3.25% with 0.5% points for 15 years.

As you can see, there’s no incentive to pick the 20-year term because it’s the same rate as a 30-year term. If we have additional cash, we can make a principal-only payments against the 30-year term rather than unnecessarily tying up our money.

At first, we thought paying points was an absolute ‘no.’ However, points aren’t a bad thing. Paying down your rate up front can save you an appreciable amount in interest. Plus, points are tax deductible.

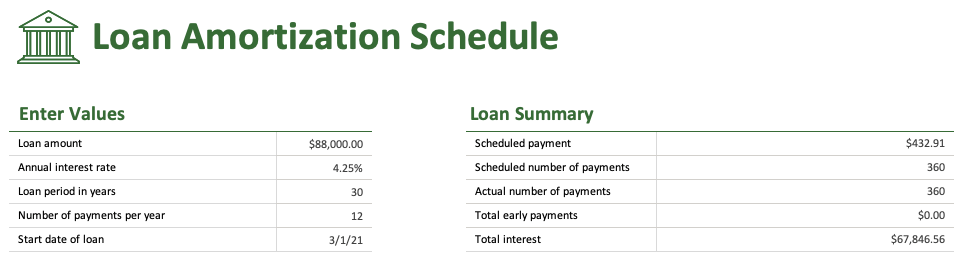

Now for the breakdown of each options. Let’s say the house purchase was $110,000 (because it wasn’t an exact number, and it’ll just be easier to use a ‘clean’ number like this). Microsoft Excel has an amortization template where you can plug in the loan terms and see the entire amortization schedule.

Option 1: 20% down payment equates to a loan amount of $88,000; the annual interest rate is 4.25%; the loan is for 30 years, with 12 payments per year. If we make no additional payments, this totals about $67,800 worth of interest paid over the life of the loan.

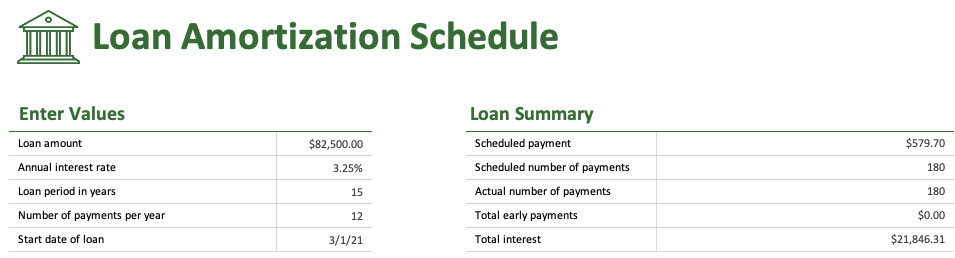

Option 2: 25% down payment equates to a loan amount of $82,500 at 3.75%. If we make no additional payments, this totals $55k worth of interest paid over the life of the loan. This requires an additional $5,500 brought to the closing table, but saves almost $13k in interest. It also decreases our monthly principal and interest payment (i.e., not including escrow) from Option 1 by $50.

Option 3: 25% down payment, 3.25% interest, and 15 years (instead of 30 years) equates to just under $22k paid in interest. To obtain the 3.25% rate, it required “half a point.” If a point is 1% of the loan amount, that would be 1% of $82,500. This rate only required 0.5%, so that meant paying $412.50 as part of closing costs along with the additional $5,500 of down payment required for 25%. However, the shorter loan length means that monthly payment is increased (between Option 2 and Option 3, the difference is $197.63).

For about $6k, we pay a higher monthly payment, but we also save a significant amount of interest over the life of the loan. The short loan term of 15 years means this one is also not on our radar to pay off while we focus on paying down other, higher interest and higher balanced, mortgages. In this case, the benefits of the big picture math outweighed the increase in monthly payment.

We are five years in on this mortgage and are already seeing significant reduction in the outstanding principal due to the amortization schedule becoming favorable more quickly. In 10 short years more, our house will be fully paid for, through rent collection, without a single dollar of extra principal payments from our other financials. What a great feeling.

ADJUSTABLE RATE MORTGAGES (ARMs)

An adjustable rate mortgage can be beneficial depending on the terms and how long you expect to own the house. For us, we expect to hold our investment properties for a long time, so it wasn’t worth the risk of an ARM. Many times lenders won’t even offer an ARM on an investment. However, when we purchased our DC suburb home, we knew we didn’t expect to be there for more than 5 years, so we chose a 5 year ARM.

After a positive experience with that decision, we also chose an ARM on our second primary residence. We chose a 5 year ARM, even though we expected to be there longer than 5 years. We figured we would either accept the new rate, if there was one, at the end of the 5th year, or we would refinance when necessary. As a result, Mr. ODA monitored rates and refinance options over the last year or so. Unexpectedly, we sold that house 3.5 months shy of the end of the initial ARM term so we didn’t have to do anything.

I break down all the details of an ARM and our decision making in a recent post.

SUMMARY

When I reach out to my lender to ask what the rates of the day are and begin the process of locking a rate on a new loan, I ask for options. These options are in the form of a “rate sheet.” When you ‘lock’ a rate, you’re actually locking the ‘rate sheet,’ not the individual decisions of loan length and percent down. For every house, we evaluate the rate savings that can come from doing something less “conventional” than a 30-year fixed at 20% down mortgage. Our decision is based on what’s best for our goals and our cash in-hand.

As shown above, in our early decisions, we favored shorter loan terms for rate savings. but since House #3’s purchase, we noticed how much more we cared about low monthly payments and low down payments to allow us to buy more properties along the way. Every investment property loan since House #3 has been the ‘standard’ 30-year fixed at 20% down. Because of this perspective shift, we were able to buy six properties in 2017, which gives us about $2,000 in monthly cash flow that we can then use to pay down mortgages.

I realize that some of the items that I share each month will be repetitive, but I’m catering to new readers that may not have seen the previous month’s details. As always, feel free to reach out if you have any questions about this information.

SPECIFIC LARGE CHANGES FROM LAST MONTH’S UPDATE

Paid $8,000 towards an investment property mortgage. This property’s mortgage balance is just under $14k, and we expect to have it paid off in the next 6 months. It would be earlier, but we’re also paying off another mortgage at this time, so we’re putting money towards that one next.

Mr. ODA cashed a few savings bonds that were mature, so we brought in $622 that wasn’t planned.

MONTH’S EXPENSES

Every month, $1100 is automatically invested between each of our Roth IRAs and each child’s investment accounts.

We had all the tenants except two pay their rent on time, and the other two houses paid on the 12th (typically when a tenant is late, the balance is paid on the next Friday of the month – pay day). Our rental income is $12,353, and we pay our business partner about $2,100 (we collect the rent and then pay him to cover the mortgages he holds and his half of the ‘profit’ after the mortgages are deducted from rent). We made it through the month with no investment property costs! We did have a tenant power wash our house out of the kindness of their heart though.

We paid about $5,900 for our regular mortgage payments.

Our grocery shopping cost us $500. We did the trial period for Walmart+. Unfortunately, the first two weeks of that trial period were destroyed by back-to-back ice and snow storms, so we couldn’t ever get deliveries scheduled within a couple of days. Once life went back to normal, there were plenty of delivery times available, even same day. While it was convenient, it wasn’t worth the annual fee and tipping the driver each time, so we cancelled it.

We spent $57 on gas, and $83 eating take-out.

We made some purchases that aren’t typical: ski season pass for next year ($119), medical bill ($70), and some furniture and odds and ends for the house (~$1,500).

$464 went towards utilities. This includes internet, cell phones, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant. Last month I shared that our electric bill was very high. We learned through the course of 6 HVAC company visits that our unit was not running properly, and that meant our heat strips were essentially on since we moved in ($$$). We will seek financial compensation from the builder once our next electric bill comes in.

SUMMARY

Our net worth increased by $45k from last month’s update. This change is mostly due to the value of our houses increasing and our mortgage balances decreasing.