This month is basically just story telling, from insurance tidbits to mortgage annoyances, while not addressing the decline in the market and our investment accounts. 🙂

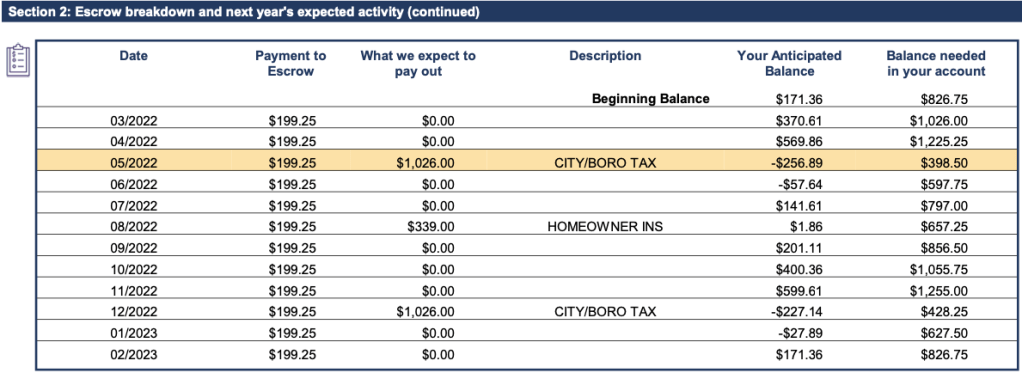

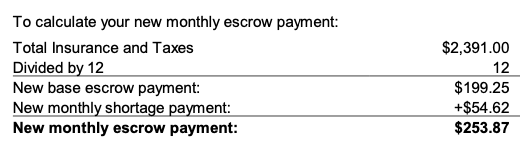

It seems all my mortgage payments are increasing on 3/1, so I’ve been managing those changes. I mentioned recently that one of our houses had the escrow analysis done incorrectly. Luckily, that was addressed, and the increase in our mortgage payment is only about $100 instead of nearly $200. Our personal mortgage increased by $16, another property increased by $52, and then our last 3 mortgages were all refinanced in January and this ‘first payment’ has been a bear. The information out of the refinancing company has been contradictory, they requested a bunch of information weeks after closing to support all the money they already gave us, and it’s just been rough. Rough enough that I ran to the post office to get a check in the mail at 4:48 pm today, only to get home to an email saying that I had to send that check (due tomorrow) to a different address. Ugh.

I was excited to share some positive news this month, but that got overshadowed by these mortgage payments! Anyway, we came home to some surprises after our vacation.

First, I had a medical procedure done in January. It was originally scheduled for November, but the week of the procedure, I had my heart go crazy on me. That cancelled my procedure because I couldn’t go under anesthesia until they knew my heart would be OK. We got my heart sorted out enough that I was cleared for the procedure, but once I was able to reschedule it, it went into 2022 ….. a new deductible year. They said that I needed to pay half the cost of the procedure before they’d schedule it. Since I had been waiting since September for this, I wasn’t going to question anything, and I gave my credit card number for $1200. Well, my insurance hasn’t processed the procedure yet, but I guess since I paid in advance, some sort of system review showed I had overpaid, and they refunded me $1196. I don’t know how they decided to keep $4, but I’ll cross that bridge when I see my claim is processed on my insurance website.

Second, I’ve mentioned before that you need to stay on top of insurance! I received a bill for my heart-related-ambulance-ride for over $900. The last time I was in an ambulance, I ended up owing the full bill, which was $500 at that time. When I saw $900, I figured, gosh 10 years later and a new jurisdiction, and THAT is what I owe. It said “we billed your insurance, and this is your balance.” Hmmm. Log into my insurance website and see there’s no claim history for an ambulance ride. I then learned, for the first time ever, how to submit my own insurance claim. I let the fire department know I submitted the claim, and then they said they’d do it for me! Why did your paper say you already did?! Well, the surprise I got was that my insurance covered all but $46 for the ride!!! I couldn’t believe it. That’s the happiest I’ve ever been to spend $46.

The most random thing that happened was a check from our electric company from our Virginia house. We sold that house in September 2020. Our mail forwarding isn’t active anymore and it was sent to our old address, so I really have no idea how we got it. It was $31.09 due to a required review of all accounts every 3 years. It’s not anything crazy or life changing, but that was truly a surprise!

RENTAL UPDATES

We had our usual suspects not pay rent earlier this month. One flat out said they won’t pay until the 23rd. I’m not even sure how to handle them anymore. I keep reminding myself that we raised their rent $150/month to get them to leave, but they accepted. So at least we’re in a good position there? The other paid us $700/$1150 on Friday (late). She at least emailed us with the awareness that we shouldn’t have to hunt her down for rent payments, so she got a pass because I was about to send the default notice at 12:01 am on the 6th. I’m also once again in a position of tracking down a rent relief payment on another house that’s supposed to cover December, January, and February. While the tenant ended up paying December rent, we’ve still been floating the January and February finances. The approval of their application (that was submitted in November) was January 10. As of today, no information from the State and no check in the mail.

I got a tenant renewal processed this morning. We increased their rent by $50/month (starting 5/1 when their current term ends), after it having been steady for 2 years. Our usual baseline to keep a good tenant is a $50 increase every 2 years.

We gave two property managers notice to increase rents on 2 properties that are up for renewal on 4/30. We do 60-day notices. It’s not entirely necessary, but I look at it as a way to negotiate with the tenant for a month, and then if they don’t agree to new terms, we have a month to get it rented. One ‘cried COVID’ last year, and we let her by. She’s been there 2.5 years at the same rate, and she even got the house under market value originally because it was November (bad timing). She’s at $875 and we said we’d go to $950. That’s a larger increase than we usually do, but the market rate for the house is $950-1000. If she balks, we’ll manage the turnover and get a new tenant in there. For another house, they’re at 1025 and have been since October 2019. They even negotiated a discount back then for an 18 month lease, so they’ve been under market. Despite our efforts to grieve our taxes, the City thinks this house is in an affluent neighborhood and has charged as such. We’re offering them a bump to $1100. Again, more than our usual $50 increase, but it’s been more than 2 years and $1100 is under market value. Then we had a 3rd person say she wants to stay in the house, but her lease isn’t up until August. She’s been there since August 2017 and has been at $850 rent since then. We’re looking to increase her rent to $900. She’s an awesome tenant that never needs anything, and I know she’s in grad school without much money. We’ve made her so happy for the last several years by renewing her without an increase, so I hope she understands the need to increase it now.

I paid the insurance on our townhome, which is a property we own outright, so I need to manage the escrow-type transactions. That was $210.

After our cash-out-refis in January, we have been looking for a new property to purchase. We’ve made 4 offers that have been out-bid. Mr. ODA has been trying to work the off-market angle. We made a full price offer for one of the houses contingent on seeing it, and the guy said that he’d now prefer to sell off his portfolio as one instead of each individual house. He declined our full-price-off-market offer. Sketchy. Then another guy said he wanted to wait until the new flooring was installed in his house before letting us see it, and then he won’t respond to messages now a week or so later. Interesting. We’re now trying to work another off-market deal through our Realtor, but the seller and our Realtor are out of town. I ran the comps on it and come to $235ish, while they were expecting $250k. I don’t deny that they’d get an offer in this market at $250, but I don’t know that it’s worth it to us. Then again, to be done with this driving around, seeing houses, making offers, and losing out, may all be worth an extra $15k.

PERSONAL TIDBITS

This month, we went on a trip for just about a week. The flight was paid for in a previous month, so that’s not captured in our spending. We stayed with a friend, and she made us nearly all of our food. We paid for our brewery visits with her. It was a great trip, and I definitely recommend Bend, OR! We did a last minute change from Touro for our rental car to a ‘regular’ car rental place at the airport, so that charge shows up in this month’s finances. We also booked 2 last minute hotel rooms, once for the night of our arrival and one for the night of our departure (we flew in/out of Portland, which is about 2.5 hours from Bend, so it was easier with the kids sleep schedules to be near the airport those two nights instead of arriving really late or leaving really early).

We bought Hamilton tickets. We were late on that band wagon until we finally found a friend with Disney+ who wanted to watch it with us even though they had seen it 257 times. Since December 2020, we’ve watched Hamilton a whole lot. We got on right when tickets were being sold and were about to accept the $200+ ticket price until Mr. ODA found the ticket sales through the actual venue were only $130! It’s not until June, but that’s something to look forward to!

We finished our basement over the last year and have been using for the last month now. We had a projector on hand that we used as our TV down there, but it started to die shortly after we hooked it up. We bought a new projector and have been really happy with it, and I was happy with it only being $270.

While our electric bill was surprisingly low last month, it was surprisingly high this month. They did an estimated meter reading, putting the estimated kWh usage at the highest it’s ever been. When I questioned their estimation process and shared the current meter read, they said that next month will probably be an actual reading and since it’s not more than 1000 kWh difference, they’re not going to change anything. Sure, I can afford this $414 bill that may be offset next month, but many people can’t. Their estimation process shouldn’t put the projected energy usage at an all-time-high, thereby dumping surprisingly large bills on people. Regardless, it’s something that works itself out, and isn’t something I’m going to fight any harder on right now. It’s just annoying knowing that our energy usage was high last year because we had a broken unit without our knowledge, and then with a working unit, they’re estimating that we’ve used more than ever.

Mr. ODA changed one of our credit cards, so I’ve been all out of sorts here now. The credit card was a travel-related card, and they increased their annual fee by $100. He ran the numbers and determined the benefits didn’t outweigh the cost increase. Instead of closing the card, they agreed to change the type of card. However, all the things we used that card for are now on different cards, and this change “activated” an old card of mine. Our credit card usage is convoluted; perhaps I’ll do a new explanation and update my last post on it (and then maybe that’ll get me to remember all the changes!).

NET WORTH

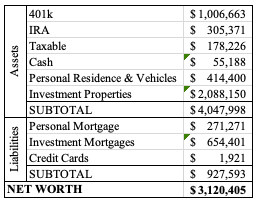

Our net worth dropped about $15k from last month, but that was due to the market. While not fun to see those numbers go down, it doesn’t affect our day-to-day. Our cash balance is really high right now while we keep cash liquid for a downpayment while finding another investment property.