We had two tenants move out at the end of July. We also had back to back trips scheduled for the end of July and beginning of August, with the kids starting school on the 13th. We also had the cruise planned for the end of September into October, so that was a decent push to get the rentals rented before we left. We put countless hours into those two houses and it definitely took its toll.

RENTALS

As of October 1st all our rentals are rented! That’s a good feeling after two months of vacancy. This is the month of taxes. We have several houses that are paid off, which means they aren’t escrowed, and I’m responsible for paying the taxes and insurance on them. The 4 houses we have in KY are owed this month, and it’s about $7k worth. We’ll owe 2 houses in VA that come to about $3k next month.

I have a couple of houses that are struggling to pay rent on time. Usually it happens for a couple of months and they get back on track, but that’s not happening quickly. I’m trying to remain optimistic, but there isn’t a track record of it getting easier if they have taken this long needing to catch up.

We closed on a new property near our house. It’s a townhouse that we hope to get rented later this month. We’ll see what it looks like once it’s empty, but it didn’t appear we’ll need to do anything to it to get it rented (which is how we buy our rentals). There will be separate posts going into the details of each rental turnover and the purchase of House15 using a commercial loan.

PERSONAL

This is the last month for the 0% interest credit card. When we have a major purchase on the horizon (it was house-wide carpet this time last year), we open a 0% interest credit card. We started this concept about 8 years ago. We look for a credit card that has 0% interest for at least 12 months and that gives us a bonus of some sort. We make more than the minimum payment each month and then pay it off before the deadline. A default payment can cause you to lose your 0%, so it’s important you’re making your payments. But we don’t pay a lot towards it because the money is doing more for us in our savings account (or the investments) than it would by paying down a 0% interest balance. This time around was a bit different. The carpet only cost us $10k, but the balance is over $14k. This credit card had the same incentive as our typically used card (2% cash back), so Mr. ODA used it a majority of the time. For a while, my goal was just to pay what gets our balance lower than the original balance from the carpet. But then we had some big rental purchases that we put on the card, and it just wasn’t worth paying $5k+ to the card. We will make a transfer from our big savings account to make that payment at the end of the month.

Mr. ODA’s last pay check arrived on October 11. He took the “deferred resignation program” as of April 30. The sunset date was September 30, so that covered the payout that we just received, including his balance of annual leave.

Outside of rentals, our spending has been minimal. With the cruise, we didn’t spend much since that was a week of almost everything paid for in advance. The dog had his annual check up, so he was the bulk of our costs. We have our routine costs we see, but happy to see lower balances after all the rental work costs.

SUMMARY

I don’t even want to admit what is about to leave our account this month. I guess the positive is that it’s under $100k..? We have to pay the taxes on the houses that aren’t escrowed, pay off that credit card, and buy a house. At least the house purchase goes right towards equity. Since I didn’t get all the account numbers yesterday morning like I planned, here’s an update that captures our new purchase.

After each trip, I typically summarize how much it cost us. I like talking about money, mostly to work towards eliminating the stigma about talking about money. The more information you have, the better informed you are when it comes to decisions, so here’s a reference point to file away. We sailed Royal Caribbean’s Oasis of the Seas. I loved it!

COST BREAKDOWN

Flights – 25,000 miles + $273 We looked at several different flight options now that we’re a family of 5 flying and that adds up quickly. The first night we were looking to book the cruise, there was a group of 5 tickets for just under $700, which we thought was a great deal, but once we were ready to book, it wasn’t there anymore. We ended up going with Frontier for one direction and using American Airline miles for the other direction. When booking with miles, you only need to pay the taxes on it, so that’s what we did.

The flight options were very limited for the way home. We ended up just sucking it up and picking a 9 pm departure. Not long after the booking, we received an email saying our itinerary was changed and now the departure is 12 pm. While that seemed concerning at first – to get off the cruise, through the airport, and to our gate before noon – I had hoped it would be just fine, and it was. We got off the ship around 8:30, took an Uber to the airport, and arrived too early to check in for our flight. They built the airport expecting this isssue, so they sent us to the waiting room. We sat there for about 45 minutes and then checked our bags and got to our gate. We sat at our gate for a couple of hours and got home on time.

On the way down, we each got a checked bag because of our American credit card. However, we still needed to prepare for “carry on” status on the way home with Frontier. Then, once we were already packed, Frontier offered us to upgrade all our bags to checked bags. Had I trusted that they wouldn’t have said “no, you have to check a carry on size,” I would have happily changed our 3 carry on bags to one big bag to make traveling through places with 3 kids easier. So while some parts were harder because we had 3 rolling suitcases to account for, it was nicer through the airport to not have suitcases to manage.

Hotel – 34,000 points If you’ve ever had to fly into a cruise port, you know it’s less stress-inducing to fly in the day before. I went on a cruise a year and a half ago, and we were flying out during a snow storm that was affecting travel all over the area. We ended up arriving at our hotel near midnight, so we were happy to know we were there for the cruise boarding time and not stressing about delays that morning. That means there’s a cost for a hotel one night.

The hotel was booked with points, so it wasn’t a literal cost to us. We stayed at the Tru in Dania Beach. They had a shuttle from the airport to the hotel, so when we arrived, Mr. ODA called the hotel to come pick us up, and it worked out well. We had to wait 20 minutes for a crib to arrive, even though it was on our reservation as a request. This isn’t a huge deal, but when it’s 10 pm and I’m just setting up a crib to get over tired kids to sleep, I’m not thrilled. Otherwise, the hotel was nice and it provided a good breakfast.

Uber – $58; Airport Parking – $70; Dog – $289 The hotel provided a shuttle from the airport to the hotel, so we didn’t have to pay for that part. Then we needed an Uber from the hotel to the port, and then from the port to the airport. We requested a car seat in the Uber on the way to the port, so that limited our options. Then she was 23 minutes late to our pick up time, didn’t get out of the car to greet us or help set up the car (pick up the 3rd row to fit our 5th passenger we disclosed ahead of time), didn’t acknowledge being late, and generally didn’t speak to us except to say get our IDs out for the port. That’s not an Uber issue, it’s a specific driver issue, but that was not a great experience. On our way from the port to the airport after our cruise, we got charged a wait fee, even though the wait was because security was stopping our Uber from getting to us. Uber removed that charge though.

The CVG airport parking is $10/day for economy. That’s my first economy experience instead of the ValuPark lot, which is $12/day. I didn’t really think anything of it, but it wasn’t a great experience. I always thought it odd that the ValuPark lot has shuttles that pick you up at exactly your car, but the economy lot has the shelters. I didn’t properly account for the time to wait for the shuttle and then to have the shuttle drive through all the shelters.

Food – $44 Obviously most of the food was part of our cruise fare. We had McDonalds on the way to the airport, Burger King during our layover, and then McDonalds on the way home.

Cruise – $3,099 The big one! We did not prepay gratuities, so that was billed as we left the ship. Gratuities are $18.50, per person, per day. We had $50 on board credit. Ironically, and just coincidentally, we spent $50.40 between drinks and child care (the babies room (0-3 years old) is $6 per house before 7 pm and $8 per hour after). Royal Caribbean only requires $100 per person as the deposit, and then the balance is due a few months before the cruise departure. We booked right at that threshold, so we paid our deposit and then a few days later paid the balance.

LOGISTICS

The booking of the cruise could have been a bit more forward. Cruises are not family-of-5-friendly. There’s an option on Royal Caribbean to book a “guarantee” or GTY room. You get a discount for allowing them to assign you in an open room (of the category you picked (e.g., interior, ocean view balcony)) about a week before the departure. I did this for a cruise I took in January 2024, and it worked out perfectly fine. So we see these prices quoted online for GTY rooms, but they always make you call to book for more than 4 people. We’re expecting the cost to be just the taxes and port fees for the 5th person, but when we call, the difference is over $500.

We tried to explain how that feels like a bait and switch and that there’s no indication of that on the website, and they basically said “well, that’s the way it goes.” They can’t guarantee a 5+ room available at the time of sailing. This makes sense, but it also eliminates our ability to use that cheaper booking option. We asked if there was something they could do to help make us feel whole since we were being forced to spend $500 more than if we could be put into the guarantee-pool, and they gave us $50 on board credit.

Mr. ODA’s parents book Celebrity (same parent company) all the time, and if they book their next cruise while on their current cruise, they are given OBC. Turns out Royal Caribbean doesn’t have the same philosophy, and they hardly give OBC. We tried to see if there was a special deal for a cruise if we book on the ship and they had nothing to offer.

Our departure experience was horrific, and I’m not even sure how we timed everything so poorly. At CVG, the kiosk jammed printing our tags, so we had to wait in line to get to the counter for the last luggage tag. Well, the line took forever because there was a large group in front of us that couldn’t speak English, so the workers couldn’t get everyone checked in quickly. Then we were too late for her to print checked bag tags because it was 30 minutes before the flight. So now we’re stressed trying to get through her attitude, us being late, and having to get through security and run through an airport with 3 little kids. This is the first time I’ve ran to my initial flight (ran for connections countless times!). I’ve never had this issue before, but everything along the way took just a few more minutes than I had planned for, and the luggage tag issue stole about 15 minutes of time from us (plus, our flight was delayed by 20 minutes and then 45 minutes before the original flight time, they said it was on time… we hadn’t delayed our departure from home, but it was wiggle room we thought we had and then suddenly didn’t). After the attitude from the ticket counter, then we encountered two more attitudes from the gate agents. It was a rough start, but the flight attendants were nice, and we had plenty of time to catch our breath at our connection.

Child care is provided on the ship. They have a few hours in the morning (maybe 9-12?), then 1-5 for the afternoon, and then 7-1 am. For the kids 3-12 (split between two rooms of 3-5 year olds and 6-12 year olds), it’s free until 10 pm; then it’s $10 per hour per kid after 10 pm. For the babies (0-3 years old), you need to make a reservation for times when you arrive on the boat. We prioritized the buffet, so by the time we got to the kids area, lots of time slots were booked already. She offered me 6 hours worth of booking, which I split between 3 days. Our youngest is 7 weeks shy of being 3, but he wasn’t 100% potty trained (although we did try) so they wouldn’t let him move up. If he was potty trained, they would have let him go up to the 3-5 room. The first 2 hour block, we only used 1.5 hours worth of it based on the activities we were trying to get done. The second 2 hour block, we only used 1 hour worth. And then we didn’t use our final day worth of time because he got sick, and I didn’t want to contribute to the spread of it. We dropped the big kids off a few times and just took the baby with us to activities, which worked out fine. He’s so good when he’s alone, but the 3 kids feed off each other!

I brought lots of hook magnets. I used them to hang everyone’s lanyards with their seapass cards, hats, and to dry bathing suits. I also used them to hang from the ceiling and utilize curtains that I brought (actually, I bring these curtains everywhere we travel because a really dark room is important to getting the kids to sleep past sunrise when bed time is 2-4 hours later than usual). There were 2 hooks in the shower, 3 hooks on the bathroom door, 2 hooks in the bathroom with 2 towel bars, and 2 hooks outside the bathroom. We’re going on another cruise next year, and I’m going to bring more hooks because we could have used more space to dry out bathing suits. Having the curtains hanging to separate the kids from each other and then from us was great.

I also bought a pack of decorative magnets. This is very unlike me; I don’t like anything extra. But I put them on the stateroom door, and it helped the kids identify which one was ours. The door is textured, so they didn’t all fit. I put them inside the cabin on this big blank wall, and I actually really appreciated the decoration.

You’re allowed to bring on 12 cans/bottles that are less than 17 ounces each, so we did that for Mr. ODA’s sodas. We didn’t buy any drink packages. I don’t know what sodas cost on the ship. At the buffet, we have lemonade, iced tea, and water available. At some of the included restaurants, they have other flavored water type drinks like strawberry melon. At breakfast they had apple juice and orange juice. There are enough options for variety if you’re not looking to buy a package. I had Mr. ODA bring a non-diet/zero type drink in case I wanted some variety, but I was so full that I didn’t end up wanting any sodas and had a couple of lemonade and juice options throughout the week. The alcoholic mixed drinks are about $15 a la carte. They offer a happy hour special of margarita (and maybe one other option that’s $6-7) and have a drink of the day that’s $8. I didn’t know about the drink of the day special until day 3 and didn’t know about it at all on my last trip, so that’s a positive to know. I think the Truly/beer type option was around $8-9 each.

When buying the drink package, that’s your baseline. Are you going to drink 5 mixed drinks or 8 beers/Truly each day to make paying up front worth it? I’ve heard some people say “I just like not having to think about what I’m ordering.” But, do you enjoy paying $65 for 2 drinks? I understand it’s vacation and many people have the mentality that money is no object, but it is something to pause, have the perspective, and make an informed decision on.

The app is really good. There’s a little room for improvement, but everything you need is there. We’d like to see a search feature, where you can search “bingo” or “laser tag” and see the offerings instead of scrolling every day and hoping you catch the times. I like the daily tips they post about what’s happening that day and some good reminders. I also like how many activities are offered. I wish there were a few more things in the 6-8 timeframe for those with a 5:00 dining time, but I understand that’s not the worst problem. There is so much offered for other times, and I found myself juggling wanting to do all the things, but also not wanting to be on a schedule.

A few weeks before your cruise, the app will have most of the shows and activities available. One example that we didn’t have until we were on the ship was laser tag’s schedule. But you should get on your app a month in advance and keep checking for the show reservations to be opened. They seats go fast. We were able to reserve the ice skating show and Cats, but we weren’t able to get a seat at the aqua show. I was really bummed about that, but we went to the aqua theater at the beginning of the show and were able to get a seat.

We did not pay for a wifi package, nor did we set up our phones for an international plan. I was looking forward to being completely cut off from the world for 4.5 days. To my surprise, iMessage worked the whole trip. It wasn’t too bad, and I got to share stories as we went with some people.

LESSONS LEARNED

Book any 0-3 year old child care slots ASAP

Pack half the pajamas you need (our kids wear pajamas through breakfast at home, so there’s no re-wearing, but they don’t eat anything in the cabin, and they don’t leave the cabin once in pajamas, so don’t use up the space)

Prepare accordingly for theme nights (I may have not planned well for my oldest)

Bring as many magnets as you can hold (although you may get flagged for a bag check in security)

Read the daily tidbits in the app each morning

Don’t pack lots of snacks (I thought I’d be looking for breakfast faster than everyone being ready to go, so I packed granola bars. I also thought we’d want more snacks, but we’re so full from eating bigger meals and being on a different type of meal schedule that eating in the room was never a thought)

If you’re on the cusp of 52″, 48″, age 3, or age 6, I may wait until those milestones are hit. While it’s not the end of the world and doesn’t kill your cruise, we had kids disappointed they couldn’t do some things based on height (water slides) or age (rock climbing).

Drink the happy hour or daily special beverages if you don’t have the drink package

THE CRUISE

We took a 5-night cruise. It was more time than I had planned for originally. I didn’t want to be stuck on a boat in case the kids didn’t take to sailing well, but the price was $1000 less than the 3-4 night offerings, so we went for it. It worked out well. Everyone’s first question seems to be, “were you afraid of them going overboard?” Turns out, there are very limited options for that to even occur. We were in an ocean view balcony, but the glass goes higher than the littlest ones, so that wasn’t an issue. Most decks have the staterooms on the outside, so the only real place they could attempt to get overboard is on decks 15 and 16, and a little spot by rock climbing on deck 7. It was barely a thought of mine the whole week.

The biggest hurdle of the week was getting the kids through crowds. There’s a lot of people on the boat, and people tend to congregate in certain areas. Keeping 3 little ducklings together in a crowd could have been worse, but it wasn’t the easiest either. The cruise ship gives you bracelets for your kid to wear with their muster station on it. I wish there was more information on it, so I put their names and room number on the back. The youngest didn’t have a yellow bracelet, and I wasn’t happy about that. Luckily, I had packed a bracelet that I could put his information on. I used a regular sharpie and the lettering was legible until about the last day. I could have rewrote the information, but by then I was feeling more comfortable.

We did not push too hard to get to all the activities. We made a concerted effort for a few activities, but I didn’t want to be tied to an agenda all week. We generally started the day with breakfast. We ate in the main dining room twice, which was quieter and calmer, but also slower. One morning, I ordered a small breakfast, and the waiter pushed me to get the “express” breakfast. It came with 2 things I didn’t want, and I was frustrated that he pushed me to waste food. We usually then went to the pool or splash area (the splash pad is pretty cool with slides and activities within it for the kids). Ice cream opened at 11:30, so that worked well as a way to get out of the pool and start drying off for lunch. We ate lunch in the buffet (Windjammer). I personally liked the variety of options with the kids, but it wasn’t the easiest process. Apparently kids really struggle holding plates flat. We only lost one apple once, but it was stressful every time trying to make sure they kept the food on the plate while walking. Our afternoon was spent either with the kids in the kids club area (Adventure Ocean) while we did trivia, or they came to trivia with us. We rode the carousel, the big slide (Abyss), and participated in some random activities (family festival, scavenger hunt). We would get back to the room at about 4:55, rush to change, and then run to the main dining room for our 5:00 dinner. On my last cruise, there were only 2 dinner times, so being on time seemed less of a priority. This sailing had a 5:00, 6:45, and 8:00, so I felt the push to be as close to 5:00 as possible so we didn’t delay a 6:45 sitting. We ate all our dinners in the main dining room. I truly appreciated the themes, but perhaps only 50-60% actually participated.

At Cozumel, we got off the boat, had a beer at a tourist trap, and got back on the boat. I don’t think we were off the boat a full hour. There was swimming available in some pretty water just next to the cruise ships. There are shops for trinkets and a few places to eat or drink. It was an area that clearly catered to cruise ships and I felt perfectly safe.

Our second stop was Royal Caribbean’s island, CocoCay. I can’t sing enough praises about this concept. All your food is available. There are servers just like on the boat if you want a drink. It’s clean. There were some concerns about jellyfish while we were there, but we didn’t have any problems. My youngest was struggling with the sand concept (and not touching the sand and then rubbing his eyes or sucking his thumb), so we eventually moved over to the pool. The pool was packed, and I almost said lets just go, but we got in. Once you were in, it wasn’t uncomfortable at all, and there was plenty of room. There’s a 0 entry area with water fountains, which kept the kids entertained well. There are life vests on the island for your little swimmers. I did hear that snorkeling was sold out when we arrived around 10, so you could keep that timing in mind. The ship staff give you towels as you get off the boat (you sign them out with your seapass card), and there are towel stands on the island if you want to swap out your wet, sandy towel for a new one.

I will note that we had a medical emergency just hours into the cruise. It didn’t affect us at all. We heard the “alpha alpha alpha” call while we were at dinner, and about an hour later, the captain came on the loud speakers and announced the plan. We departed Ft. Lauderdale, but we were going to return to Miami to get this patient off the ship. They were making a plan on whether we’d have to fully dock or if the coast guard could come out to us. They announced a bit of time later that they decided the coast guard could come out. Then about a half hour after that, they said that the swells from the tropical storm we were near were too rough and the coast guard couldn’t get close to our ship to safely transport the patient between the two boats. So then they decided to send out a helicopter, and that happened just as the sky opened up on us at the aqua theater and we gave up and went to bed. So even though the course changed, it really didn’t affect anything we were doing on the ship. The patient actually got off and received emergency coronary bypass surgery that night and was recovering, so that was a blessing. There was also supposedly a death in another cabin, which I knew nothing about until after I got back home. I share this just to say – things happen, and there’s so many people, so it’s not surprising, and it didn’t affect the rest of the trip.

Getting on the ship and off the ship on the bookends of our cruise was extremely easy. I had a similarly easy experience at Cape Canaveral (actually probably easier). On the way there, we went through the security check points. I was flagged for my magnets, and in the process, they found my extension cord. Honestly, it wasn’t clear what the rules were about the extension cords. I wasn’t worried about the number of plugs as much as I was the extension to an outlet. They’re quick to say “there are plenty of outlets,” but they don’t address the fact that 3 outlets are on one end of the room and there’s only 1 at the bed. It didn’t matter though. We plugged in a phone overnight by the bed, and the sound machine was over by the kids with that 3 outlet option on the desk. They confiscated my extension cord, but they tagged it, and I got it back at the end of the cruise. After that, we went upstairs to a huge waiting room. We were told to sit in order as we entered. The place was packed; I expected this to take a while. It was less than 2 minutes. We scanned our boarding passes and walked right on. On the way off, everyone just left when they were ready. We walked right into the main dining room, scanned our seapass cards, and left the ship. There was luggage areas to pick up any luggage you had carried off the ship overnight, but we hadn’t done that. Then you go through the immigration check where they take your picture and approve you to continue. And that’s it. There was no queuing through either process except for the 2 minutes we sat in the waiting area at the port on the way on the ship. It’s incredible to me.

SUMMARY

I was a reasonable level of nervous taking 3 young kids on a cruise for 5 nights, but it went significantly better than I expected. Our next cruise isn’t until this time next year, but I wish it were sooner! I highly recommend cruising, especially with Royal Caribbean.

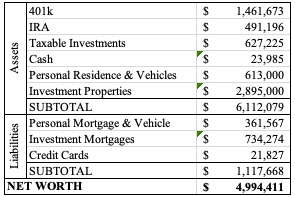

Let’s start with a win – we hit $5 million net worth!

It has been a month. Goodness. Two rentals to turn over and just … life.

That’s where I left this post on September 17. It’s currently October 6, so I’m going to just call it good and post. We had two rentals to turnover and get rented before we went on a trip, which we did accomplish, but it was exhausting. I’ll elaborate in future posts on what went into everything there. For now, I’m posting this back dated to September so that we have it for future reference, especially because it was a milestone month. Look for October’s post soon, as well as updates to the rentals (including a new one!).

This month was unbelievably painful financially. And yet, I appreciate that we’ve set ourselves up that we can handle these things without stress, even though the balances on credit cards made me feel like I was drowning. At one point, we had over $30k on credit cards. I’m still juggling life as a mom, financial consultant, part time worker, and volunteer on the HOA board. Oh, and managing two vacant rental turnovers, throw in 2 trips away from home, and school starting.

RENTALS

We had one house pay late, with little notice and communication (if you’ve been here, you know this is a pet peeve of mine). They paid the late fee at least. I had another house pay partial on the 3rd and then true up on the 6th. Again, no communication, and she beat me to asking what the deal is. I also had a tenant who already pays twice per month be late on both of this month’s payments, so that also brought in late fees.

In a story for another time, we have two vacant rentals. 11 of 13 houses renewed. Two houses each actually moved out of state, and unfortunately, my kind heart scheduled both of them to end their leases on July 31st. We’ve been spending all our time at these two houses. The one had smokers in it (against the lease) and we’re struggling with that. We’ve replaced the carpet and painted all the walls (except 2 closets and a powder bathroom) and it still smells funky when you walk in. Then there’s just the routine type turnover things like scrubbing and wiping dirty hand marks off the door frames. All of these things will be detailed in separate posts. The other vacant one was quite the story, so that’ll be multiple posts. Our attention isn’t as heavily on that one because we’re going to likely sell it instead of re-rent it.

We replaced a roof ($5500), replaced an HVAC ($8300, but split with a partner), evicted bats ($1480), and made decisions on flooring replacement in another house with extensive termite damage. Seriously. Financially painful. Coming this next month, we will also be paying for termite repairs at another house where we tore out carpet and laid LVP.

HEALTH COSTS

I tend to focus heavily on this topic in this blog. It’s surprising because it’s not really the niche of making money, but insurance and doctor bill processing seem to be wrong more than they’re right. Therefore, it falls more into “protect your money” than anything else.

This is a longer story for another post yet again, but the gist is that the insurance company took 6 months to process a claim. They sent me the bill in June. I called 3 weeks after the bill arrived to find out they had sent my balance to collections because their system flagged it as a January overdue balance…even though this was my first invoice on the matter. Love it.

The end result here is that we needed to add $1600 to the credit card.

PERSONAL

I don’t know that there’s much personal life happening with all those other things we’re managing. We took 2 trips. One didn’t cost us much because the grandparents take care of a lot of the cost, another one cost us more than usual because I put a lot of effort into food that we usually don’t do when we travel there. Overall, the trips were fairly inexpensive financially, but they took a toll on me due to the time commitment and what we had to give up by doing these trips.

Otherwise, we’ve just been wrapping up summer and starting school. We’re about to get back into baseball season with lots of practices.

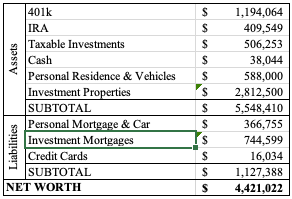

NET WORTH

The market had a big jump last week and my update of financials occurred Thursday morning. Unfortunately, life put a blog post on the back burner while we were turning over a rental, so I’m only getting around to posting this now. The market is in a fairly similar spot as of yesterday’s close, and I’m thinking we’d even be over $5 million if I were to fully update our financial status right now. We’ll just hope for the best for next month.

In October, we’ll pay off our $15k credit card that we’re carrying, so that will be a big swing in our credit card balance two months from now. We need new windows at our house (the seal keeping in the gas between the panes is going on quite a few windows (or went years ago), and it creates this streaky dirty look to them), but I think I’ll appreciate not carrying this large credit card balance month to month while we utilize the $0 interest for a while.

Well, we started the month with way too many things hitting the credit card: 2 insurance policy renewals, a new insurance policy, air conditioning fix at a rental, and bathroom replacement at a rental. That eventually led to a $1500 charge for bat removal at another rental.

PERSONAL

My big news this month was handling my HOA’s annual meeting. We’ve been working so hard for the last year, and I tried really hard this year to increase communication between the Board and community. I think I did a good job because there wasn’t any contentious point of this meeting and there were very little questions. I received nice feedback on how I presented the budget and that I did a good job throughout the year. It was a welcomed win since there was a lot of heat in the previous couple of years.

The family’s big news is getting passports for a trip this Fall. The parents already have theirs, but we got the kids their pictures and submitted their application. So our credit card balance is higher than normal because we paid for flights and the cruise itself.

It took us until the last week of June to meet our deductible on our health insurance. It’s only $3,300, so that’s quite the impressive feat. I’d point out that my March surgery took until then to get processed correctly, but at least we eventually got there. I have very little faith that it’s all processed correctly though, so it’s on my to do list to verify that we’re not overpaying into that deductible, which they don’t make easy because they don’t show me prescription fills clearly.

We went on a trip for a long weekend to visit Mr. ODA’s aunt in WV. They have a vacation house there, so we didn’t pay for lodging. Unexpectedly, they provided all our meals. I bought them a gift card and some beer. So between that gift, gas, and the meals on either end of the trip, we spent about $200 for a trip, and it was one of the best vacations I’ve been on.

Two of the kids spent this past week at camps. One was 3 hours per day at a dance studio, and the other was 9.5 hours of all outdoor time for the week. He had a blast, and I’m kind of jealous that he got to play all those games and have a great week.

RENTALS

This month, I received an email from Rent App that a tenant was paying their rent. She didn’t give me a heads up, so I wanted to verify things with her. She said this app pays me in full, but it takes the first half of the payment from her account at the beginning of the month and then the second half of the payment in the middle of the month. They’ve lived with me for for 8 years, so I’m surprised she sought out this option instead of talking to me about a payment plan. The program was extremely sketchy and I didn’t feel good about a single step of it. I gave up the registration process at the point that it required untethered access to my phone, but I wish I would have followed my gut at the first personal information step, as if it wasn’t bad enough I had to give my bank account details for the transfer to happen. The payment eventually came through on the 10th, but I didn’t feel good about it.

Another tenant paid late with the late payment. And another tenant paid late with little to no communication and several follow up conversations. I can’t stand when I have to hunt down money. I’m willing to work with everyone who reaches out. She paid the first one with a (1/3), so clearly she knew the plan. And yet, on the 6th, I had to ask where the rest of the rent was. She said it would be done that day. A partial payment was made on the 7th. Then another partial payment on the 8th to finish it out.

We hired someone to clean out the gutters at two houses. Both houses are inundated with trees over the roof, so it’s something we need to stay on top of because they back up every 6 months. We could add gutter guards, but just didn’t see the point since we could do it. Now we don’t live there. He is also going to cut trees 10′ back from the roof on one of those houses.

And then the bats. One house had a bat show up last Monday. My property manager didn’t think much of it, so we didn’t do anything (I wasn’t even told about it at that point). Another bat showed up on Saturday. The tenant went for rabies shots and got boosters for her dogs. She then took a bat to get tested, which came back negative. She said she wasn’t comfortable staying there, so she stayed with a friend. We had traps set so bats could get out of the attic, but they couldn’t get back in. The pest people will go back next week to check on things.

We have two houses that will be vacant at the end of this month. We were supposed to have one at the end of June and one at the end of July, but the June one asked for an extension. I let them have it, but I’m not thrilled about my timing now. We won’t be able to truly get to work in there until mid-August, and it’s going to require a lot of work (not hard work, just time consuming). Then for the other one vacating at the end of the month, we don’t intend on renting it again. We’re going to let it sit over the winter and sell it in the spring.

NET WORTH

The way that I update our net worth each month involves overwriting the numbers from last year. So I can easily see that we’ve gained over half a million net worth since July 2024’s update. What’s nice about that is that it’s all appreciation, paying down mortgages, and the stock market with continued savings. We didn’t make any large financial moves that would have adjusted our net worth in one large move like buying a house. I had a conversation with someone about our net worth and goals recently. It would be nice to cross the $5 million threshold, but we’re not actively managing our funds in a way that will cause drastic swings outside of market movement. We crossed $4 million in March 2024.

We’re over $200k from last month’s update. Our credit cards are much higher than last month because of trip purchases and rental work that was unexpected, but needed. Here’s to the last month of summer.

I had an “ah-ha” moment the other day about this word. There’s a difference between being able to afford something and wanting to afford it. So many times, we focus heavily on what people see on the outside. I hear it at work lately – I work with agents, and there are comments made about how people spend their money. Now, I agree with the “I just handed you a check for $20,000, what do you mean you have no money?” However, there’s a flip side. Just because someone pulls up in a Tesla doesn’t mean they want to throw money around.

TRADE OFFS

Mr. ODA and I have money. We can go out to dinner, go on a vacation and stay in a fancy hotel, pay for flights across the country for all 5 of us, buy another house, splurge on a vacation house and a boat. If we wanted to. We don’t.

Instead, we want to look into the future. We decided that the ability to spend time as a family, being there for the kids’ activities, and going on different kinds of trips throughout the year to give the kids experiences is more valuable.

I talk about this concept often in this blog. Every dollar spent has an opportunity cost. Every dollar spent should cause the question, “is this the best use of this dollar?” We joke about how we hesitate to buy a $30 pair of shorts, which you wear for years, yet we’ll spend $30 to eat one meal. Of course, we do have those instances where we go out to eat, but they’re not a constant staple of our household. We know that the instant gratification of that one meal isn’t going to get us to our long term goals. It’s the same concept with the $5/day coffee purchase. It’s not about the literal $5 that’s going to get you on your way to financial freedom; it’s the mentality that comes with making better financial decisions.

HOUSE POOR

When we were shopping for our first house in 2012, the bank pre-approved us for $750,000. We set our limit at $350,000. Why? Because we felt we could scrape together 20% down payment and closing costs for a $350,000 home. If we were under a $750,000 mortgage, we’d have to pay a higher monthly payment and private mortgage insurance (PMI) as a penalty for not having 20% down. At $350,000, our mortgage payment was about $2,000. At $750,000, the mortgage payment with PMI would have been about $3,500. That’s an extra $18,000 per year we would have been spending on a house instead of investments, trips, a new car, etc.

If I said to you, “pay $2000 to your mortgage, and at the very same time, put $1500 into a savings account that you can’t touch,” what would your reaction be? You’d find every excuse not to do that. You may do it for a month or two, but there would be an emergency or large purchase that comes up and you’d justify using that money for that instead.

CAR DECISIONS

While we can “afford” the Tesla, we didn’t buy it to be showy. We bought it to serve a purpose. Unfortunately, the concept of Tesla comes with pre-conceived notions for people. We didn’t pay for an extra color. We bought the base model because we weighed our expectations of using it versus the cost of extra charging needed and such. With the tax credit, our net was $38,000. I’d venture to say your car was about that price or more if you bought it new. So while we can afford the Tesla, that’s what we chose for our family because it met our needs. We didn’t buy an $80,000 BMW just for the name when a $40,000 car meets our needs.

GADGETS & TRINKETS

Maybe your spending is at the hundreds of thousands level. Maybe you’re buying the new Nintendo Switch that just came out. Maybe you’re buying each new game for your gaming system. Maybe you have bought into the influencers that are constantly jamming the latest mop and vacuum down your throat. Do you need 4 mops? Do you realize that you probably just need to actually use the one you already have and that this new gadget isn’t a miracle worker?

Everyone has their thing. There’s something that brings you joy and you’re going to be drawn to purchasing new iterations of it. I get that. But have you stopped and really considered the purchase?

This is where I don’t like the “envelope” method. People who use this concept, whether it’s literal envelopes or separate accounts, tend to overspend. They see there’s money left in an envelope and it goes into “extra” immediately in your head. “I saved this month, so I can buy myself something fun!”

This month, I replaced my favorite earrings because the originals were worn out ($12), bought a pair of black shorts because I had none ($14), bought a dress because Mr. ODA needed free shipping 😉 ($20), and two books I really want to read and aren’t available at the library ($20). Before this month’s Amazon order, my previous one was for kids summer pajamas in April. I buy filters for my vacuum instead of replacing it (although I’ll admit that I’ve had my eye on a new vacuum cleaner for about a year, but it’s been sitting at $80 and I know I’ve seen it for less than that). My mom bought me my steam cleaner mop several years ago, and I have a Bona that I bought for myself in 2016. The point here being that I’m stopping and thinking before making decisions, regardless of the amount of money I have available to me.

EDUCATION

It comes down to being an informed consumer. While you can rely on the experts, understand your own goals. When that relationship banker ran our numbers for a house purchase, all he did was ask us our fixed monthly expenses and income (debt to income ratio). Note that our approval was after the changes on how mortgages were approved from the 2008 crisis. It’s a flawed system. But we knew our limits and what our goals were. He didn’t ask us our goals outside of “so you want to buy a house.” At the same time, we were paying towards a wedding. So on top of needing to come to the table with about $80,000, we also needed $12,000 to go towards that wedding. We closed on our house on July 17th and were married on August 4.

We have money in many locations. Currently, in our main checking account, I’m projected to fall below $0 if I don’t have any income before the end of the week. I have a bank account with more than enough money in it, but it just pains me to move money out of that account. I don’t want to set the precedent. I bet if I had kept my business money separate from my personal money, it wouldn’t be as obvious. But we don’t keep things separate because the business income is our family income. So when I had to pay out over $3000 for a repair on a rental house, that ate into my personal checking account balance, so I’ll need to make that transfer.

I listened to the young receptionist at work bark about people spending their money and how someone showed up in a Tesla but can’t pay their $75 office bill. However, I’m observant. I saw that she complained to me that the money in her account showed up on the wrong day so her card was declined at Hobby Lobby. I saw that she regularly came in with a new outfit from TJ Maxx. I’m sure she got a deal, but is a new outfit twice a week a necessity? When she was let go from the job, she turned to “retail therapy.” It’s hard for me to help walk you through the loss of income while you are actively spending.

Personally, I worry, “what if the ability to transfer from our special savings account isn’t there one day?” That’s because I’m looking at the big, big, big picture of our lives, and not what happens today, this week, or this month when it comes to our finances. So that’s why I don’t buy the kids all the cute outfits I see and I don’t buy myself the latest gadget. I’d rather have the ability to go on a trip and do activities with the kids that build memories.

School’s out, and my organization of time isn’t what it used to be. I did put together a summer calendar, made a list of activities available for each day, and made their wish list, so my type-a was showing then. The only problem is that the oldest can read and the second can mostly read, and so they see something and think we can do it immediately.

RENTALS

We had one that was supposed to leave at the end of June, but they asked for another month. So now we have two supposedly leaving at the end of July. I’ll believe it when I see it. Nothing they’ve done has indicated they’re excited about leaving and making progress towards finding another place (they’re both trying to move to another state).

I had another tenant ask to renew for two years. I agreed she could stay there, but we needed a slight increase in rent in year 2. This isn’t the first time I’ve done it that way.

We’re still chipping away at the termite infestation. Live termites running around when the shower got removed meant we had evidence that they’re not treating correctly. They did a major treatment of the house and said it will take 45 days to take effect. We’re leaving it for 60 days before tackling the damage under the living room. We cleaned out and laid a vapor barrier in the crawl space a couple of months ago. In the bathroom, we replaced the subfloor, replaced the stall shower, replaced the vanity, and laid LVP on the floor. The bathroom really needs to be painted now, but generally it’s in good shape. That cost us $3,710.

PERSONAL

We’re just managing the summer schedule. We’re not doing things that cost a lot of money outside of camp and our trips. The two little ones did a church camp this week, which was 3 nights for 2 hours each night, and totaled $40 for the two of them. The two big ones are doing separate camps in a couple of weeks. Then the middle one is doing a gymnastics camp in July. She was originally only scheduled to do that one, but a dance camp with some friends came up, so she’s doing that one for $100.

We haven’t done any trips yet. It just worked out that our trips are back to back at the end of the summer. It also means we’re going to miss both back to school activities, so I’m pretty bummed about that.

We’re still carrying a balance from our carpet replacement last Fall. We use that credit card regularly, so it isn’t as low as I would have liked to see. Typically we get a card for the bonuses, but it’s not worth using it because we have a 2% cash back card. But this one offers the same, so Mr. ODA uses it often. We’ll need to pay that off in October, which is also when Mr. ODA’s pay checks are expected to stop.

NET WORTH

I didn’t get a few numbers from Mr. ODA, so our actual net worth is probably slightly higher than this. The market has recovered a bit for us, so we’re continuing to increase our net worth from the month before (there was a dip there for a hot minute).

*I’ve been working on this post for a week, so my numbers are a week old, but I don’t want to re-update them. I’m also posting on a Tuesday just to get this ‘out the door.’*

I’m starting to pull myself out of the overwhelmed hole I felt I was in. There’s still a lot going on, but I feel better equipped to stay on top of things. I had just been so exhausted, that I didn’t have the energy to do anything extra each day, and I was just getting by. Last weekend, I was able to work on pressure washing our patio and deck furniture (which was long overdue), and then I stained our deck. That’s been a pretty good springboard to me getting a fire lit under myself to get other things done, so that’s felt really good.

Our middle child graduated pre-k on Thursday. That was a big milestone, and my poor girl is so sad that she’s going to miss her teachers. She’s really struggled with my going to work and not being home all the time (although my time not home, while she would be home, averaged about 10 hours per week). I have things better organized at work, and I’m feeling good about my tasks and role in the office, so the hours I’m spending there are dwindling. I had agreed to about 20 hours per week, but I was closer to 26/28 each week. The biggest issue was waiting for someone to be available to help me, and then that everyone else is full time, so they don’t realize I’m trying to get out of here by 2 pm each day. This week our oldest graduates kindergarten and has many events around end of school.

RENTALS

One of the mortgages has been paid enough that the balance dropped from 6 digits to 5 digits. It’s still a lot of money owed there, but that felt like a nice accomplishment when I went in to capture the balance!

June is Richmond tax season for these houses. That means I’ll be paying out large chunks of money for the houses we have no escrow on.

We had a few maintenance needs come up. One house had the water heater flood the basement. Luckily, I think we’re OK on that front. We replaced the water heater. The gas wasn’t hooked up right, so the tenant called the plumber to get that squared away. This happened while I was in a different state, and I’m so grateful it happened in a house with a handy tenant.

We had some flashing fall off a roof line. This wasn’t a priority to address at the time, but the tenant started claiming allergies were flaring up because birds were getting in the attic. Sometimes you just need to accept that’s the story you’re hearing. We had a handyman go over there and verify there are no birds anywhere. The “hole” she thought she saw was just where the soffit was hanging a bit, but there were no gaps in the wood structure itself. He tacked up the soffit, and I contracted with another company to repair the one piece of flashing.

That handyman also went out and handled a wasp nest. At that house, the tenant says a window won’t stay open when she opens it, and we let her know it’s on our radar now, but it won’t be fixed just yet as our people are spread thin and that’s not an emergency. That house had a temporary tenant in it (housing with our current tenant). To cover the tenant and us, I asked for a $500 deposit. When they moved out, I had our tenant sign that there was no damage, and I returned the deposit.

We’re still working on the major termite damage that occurred at another house. There was quite the domino effect. Leaks from bathrooms and the laundry room created a very wet environment, which created a breeding ground for termites, which feasted on our wood all over that place. The crawl space got cleaned up, but we’ve been waiting over a month for the bathrooms to get replaced and fixed. I’m hopeful that it’ll start next week, but frustrated nonetheless.

I had a leak from a toilet bolt at another house. I was frustrated because we had just been called out for water on the floor at this house recently, but it turns out this was necessary. When the house is a certain age, things just wear away and need replaced.

We also had a limb fall from a tree at another rental. The tenant explained how much of a liability it was for me. I love when tenants instruct me on my level of liability (that’s sarcasm). We have a tree guy that’s been super useful for many things and he handled it the next day with no problem.

PERSONAL

We haven’t been spending much money. Most of our money these days goes to grocery shopping. On our current statement for our main credit card, we only have 11 transactions recorded for over 3 weeks.

We paid our last month of pre-school for our second. They are closing the school and they didn’t want to add on days for the snow days that occurred, so they gave us $50 off the last month of tuition to cover the 2 days we were owed for make-ups. Since the school is closing, everyone scattered, and we ended up not getting into another preschool next year for our youngest. So at this point, that’s an extra $375 per month in our pockets next year – unless a spot opens up for the littlest.

Mr. ODA took the buy out, which I think I mentioned last month. His last day of work was April 30th. He said he’s settling into the not working concept and starting to get over the desire to know what’s happening at work and with his programs he worked so hard on. He’s done a lot of work around the house here, including treating for termites in a very intense fashion, but that was cool to see.

NET WORTH

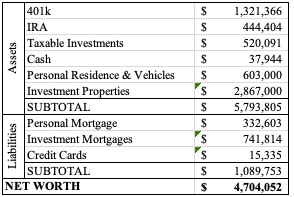

Two months ago, my job asked for my goals. It’s a specific document that I was to fill out. Someone else had mentioned their net worth goal, and our next big step would be $5 million net worth. Well, the market has been in shambles, and our net worth plummeted from where it was. I thought it prudent to not make such a goal when our net worth is completely reliant on the market actions right now (i.e., we’re not selling/purchasing or making any big moves that would drastically change our net worth outside of the market actions). We’re finally on the upswing and now at the highest net worth we’ve been, so that’s encouraging after those big dips recently.

On April 6, we submitted our taxes. Honestly, I think that’s the earliest we’ve ever done it. We usually owe a good amount, so there’s no incentive for us to do it early. After owing a penalty last year, we pushed to be on top of the projected tax liability. It looks like we’ll owe a bit on the Federal side and get a refund on the tax side.

And so here’s my annual reminder that if you take the time to manage your finances all year long, then tax season is not a hurdle. I find it much easier to maintain 13 houses worth of data if I do it during the time it’s happening. Life has gotten in the way a bit, and I find it hard to even make sure I have one or two months worth of things logged correctly. I hope to be more on top of it in this coming year.

I have a spreadsheet where I log all our income throughout the year. I set up a formula where I can track each month’s income to ensure I receive the total amount that I expect to receive. I found that since some of our houses pay the same dollar amount of rent, it’s harder for me to mentally track each month’s payments, and I like having the visual and verification through this sheet.

Then there is a tab for each property in that same workbook. The sheets are set up based on monthly expenses, and I plug in projected expenses (e.g., taxes, insurance, utilities). This helps give me a verification that expenses have been paid when owed. By now, I have nearly every invoice emailed to me, but I like having this ‘fail safe’ look at what may be owed that I hadn’t paid in a given month.

Then Mr. ODA enters our investment items, W2 income, and interest income into our tax software. Then I sit down next to him and dictate the numbers from my spreadsheets so he can enter them into the software. We have 13 rental properties, so this is time consuming. However, it’s really easy. We enter our data into the fields for each house. This year took us about 90 minutes to enter the rental property information.

I know multiple people who file extensions because it takes so much time and effort to gather the documents for their accountant to do their taxes. It’s like they don’t think about their taxes until April 1 and then decide it’s too much to do in two weeks. This is where being prepared all year long comes into play. Make it easier on yourself and put yourself in a position where it doesn’t feel overwhelming.

We started getting emails about end of school year activities, and boy was that a surprise that we’re at that point. The middle one is done mid-May and the big kid is done at the end of May. Less than 2 months until summer break.

Mr. ODA took the second round of the government’s offer for administrative leave, which means he would only have a few weeks left working. I’m still working my part time job, which is taking way more hours than we had planned for. I’m enjoying it, but it’s been a juggling act with the family, which is probably why my son who absolutely loves school begged me to stay home because his belly hurt last week.

Buckle up because apparently I have a lot to share this month.

RENTALS

We received about $600 in tax payment reimbursements from one of our localities, so that was a fun surprise this month. Really helps my psyche that I have a tenant who hasn’t fully paid, didn’t tell us why ahead of time, and hasn’t been up front with when she’s going to actually pay us.

I executed 2 short term leases. Both included a rent increase for their short term period; one house is increased by $75 and the other by $25. Luckily, both are here in the Central KY area, so we can flip it between tenants. One is scheduled to leave June 30th. That house will need new carpet in the bedrooms, and it’ll need probably a whole-house paint job again. They smoked in there, even though we covered the lack of smoking rule multiple times. I’d be more upset about it if the carpet hadn’t reached its useful life years ago. The other house leaves July 31, and I can’t even tell you where we’ll need to begin with that one. She made a wood feature wall without permission. She had a giant fish tank without permission. She spent a lot of time doing things that really weren’t an improvement, so I’m definitely worried about what we’re going to uncover in that house. Mr. ODA and I are talking about fixing it up and selling it. We may look for a short term renter so that we can sell it in the Spring instead of this Fall.

I had 2 other properties accept a rent increase that will go into effect later this year. I require 60 days notice for changes so that starting at the 30 day mark I can begin advertising it if needed. One house goes up by $25 per month as of June 1, and the other goes up by $50 per month as of July 1. I also have another property that has a rent increase of $50 per month going into effect next month.

I have 4 houses that renewed another year, and I didn’t change their monthly rent rate. There are 4 more houses that haven’t been discussed. My intent is to have them renew for a year at their current rate. There are 2 of those 4 that could leave at the end of this term, but time will tell.

We have multiple maintenance issues to address. One house requires a tree trimmed off the roof, the siding cleaned, and the back deck stained/painted. We still have termite damage we’re dealing with at a house in Richmond. I have a leaking toilet that was just addressed, and then they hit me with a faulty HVAC unit during a heat wave. Then we have some houses that really need eyes on them to see what condition they’re in at some point this summer back in Richmond. It’s amazing to me how people just don’t care to tell a landlord that something is broken. I woke up this morning to a text that one of the houses here has a flooded basement due to a water heater failure.

I spent some more time fighting my insurance guy here. It irks me so much when I see him offer up his services on the local facebook group for property owners. He’s quite terrible. I sent him photos of a house that had some issues with a cluttered backyard and had the tenant clean that up. I had to fight him last month on an increase where he changed one house from a crawl space to a basement when I assure you that the vines growing through the windows solidify it should not be deemed a “basement.” When the dust settled from that debacle that he was insanely unresponsive to, I ended up owing $9.68. When I asked why my account wasn’t put back the way it was found before this mess he created, he said he didn’t know but it’s probably from the audit and changing square footage. HIs guessing and not actually answering infuriated me. I gave up and paid it, but then I ran to get quotes from other people. I hadn’t done that before because our 4 claims in a 12 months period are killing us (again, because I really wanted trees to fall on us!). I hate when people make the claim that because it’s not a lot of money, I should just give up and accept it. That’s a ridiculous way to treat people.

PERSONAL

Our electric bill is almost double what it was this time last year thanks to the vehicle charging and hot tub. Our electric bill is relatively low, so that’s not all that surprising. We also have 5 full people in this house now (as much as you can count a 2 year old as a full person… but he knows how to control light switches and eats a ton of food that we need to cook him, so I’m sure he’s a factor there!).

I’ve been working at my new part time job for over a month now. Mr. ODA was making fun of my hourly rate, but I’ll tell ya, it felt good to receive a paycheck that wasn’t $45 like it was for a day of subbing at the preschool.

I took the kids to get haircuts. My middle has had her hair cut once before, but I’ve cut the boys’ hair forever. I had family coming into town and the oldest was looking really shaggy. So I swallowed my pride and threw money at the problem, which is very out of character in this household. I just didn’t have the time to cut their hair, clean them, and clean up the mess. For $66 and 45 minutes from the time I left home until I got back, it was well worth it to me.

I had a medical procedure done this month. We haven’t met our deductible. In February, they said I had to pay my deductible to them. I said that didn’t make sense and refused to have them hold $2800 of my money for 2 months. They gave me an attitude and said I could never ever ever ask for a payment plan in the future, so that I could pay $500 to hold the date. I then showed up for the procedure, knowing I haven’t met my deductible, and they didn’t take any money from me. Another business model that bullies the customer into illogical money decisions. I also had an eye doctor appointment that was frustrating in itself, but I’ll spare you those insurance and communication details.

On top of everything else I’m juggling, Mr. ODA is coaching our kids’ t-ball team. Coaching means that I am team mom. That means that I’m responsible for communicating updates from the league (in the slow and haphazard fashion I receive information), gather value card sales that are required of every team member, organizing a basket for a raffle, and the best one – raising $350 for team sponsorship. What the heck, man?! Where did I say that my signing up of two children to play in the league means I have history or ability to gather money from businesses?? Well, I did it. I raised $350 and another mom raised $200 for the team.

No financial impact, but I’m also juggling our HOA board duties. I released our longstanding property manager and hired a new company, which took effect April 1. That’s taken a lot of time to get them stood up and make sure we stay on track for our annual meeting schedule in June.

NET WORTH

And with all of that said, that doesn’t even address the giant reduction in our investments that continues to happen. To counter some of the loss, I updated our property values for our houses. I don’t do that every month because they don’t move very much, but I can usually count on a few increases as the spring market ramps up. Our net worth did slightly increase (based on yesterday’s market closure, not today’s) from last month, which was a nice surprise.

I wonder why I’m tired and bogged down, but that post outlining what I’ve done recently made me realize all I was able to accomplish even though I felt like I was a jack of all trades and master of none. Hopefully things will settle down in our lives going forward now, even if I know there are definitely two house turnovers in my future.