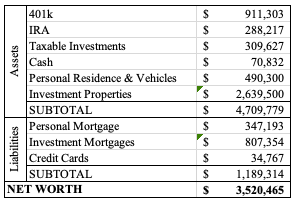

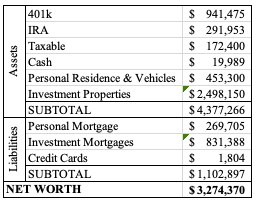

We’re just going to cut to the chase – $4 million net worth! I mentioned that this was a goal for this year. Unlike other years worth of large jumps because of purchasing houses, this was less in our control (granted, our market allocation decisions are what’s driving it…. and by “our,” I absolutely mean only Mr. ODA’s because I don’t do anything in that realm).

RENTALS

Well, we’ve had a quiet month. What’s going to be funny is, I’m going to list the things that we did. Quiet doesn’t mean silent or without effort, but we’ve had a rough go of it over the last year, so this was a welcomed break.

We had termites at a property. We pay $98 annually for their termite warranty program, since we found extensive termite damage and live termites when we bought the house. We’ve had to treat the house several times, so this $98 is a steal. However, I’m wondering why we keep needing to treat the house.

We paid $125 for a plumber to go out to a clogged sink. When we received the invoice, it was for 2 plumbers to go. Between the phone call that they were on their way and the tenant saying they were great, only 35 minutes had elapsed. The company charged us almost $300. Mr. ODA called to ask why they choose to send two plumbers to do a one-man job, while also charging us for it. The owner said it was for liability purposes, which Mr. ODA fought back on. They agreed to a reduced rate, but we were only charged $125, which was less than agreed upon.

We had our third tenant move in, after we unexpectedly had to turnover three houses in the middle of winter. We also were given notice by another tenant that she’s vacating by the end of March. We handled increases for two houses (one handled by a property manager to increase $50/month, and one handled by me to increase by $25/month).

We had one tenant pay on the morning of the 6th with no communication, so I did have our property manager let them know that’s not going to be ok. We also had a usual suspect pay late, with the late fee. However, their communication was frustrating. They said they’d pay on the 6th. At the end of the 6th, they said the money hadn’t cleared like they expected. No communication on the 7th. I asked for an updated on the morning of the 8th, and they said it would be that day. At 11 pm, I hadn’t received anything and reached out. I was then told that money was going into the ATM right then so that she could pay. Sometimes I wish I could do a deep dive into tenant finances so that I could help them out.

PERSONAL

Mr. ODA has a trip in July where a group of guys will hike in the Rockies. Our family is going out before that trip is scheduled to do our own exploring. We booked 4 round trip plane tickets, and Mr. ODA handled the lodging booking for the guys’ portion. That’s almost $3,000 worth of purchases, so our credit cards are higher than usual.

Speaking of the plane tickets. We purchased gift cards from Costco for Southwest. The gift cards are essentially $450 for $500 worth of purchasing power at Southwest. We bought two, therefore saving $100 on the tickets. For an extra few clicks on the computer, and the 15 minutes waiting time before the e-gift cards were delivered to my email, that’s $100 that can be used somewhere else.

We bought a new vanity for our bathroom. That was about $700 for the vanity, faucet, toilet flusher, and mirror. I sold the old vanity (in rough shape) for $30. And because I’m proud that I did most of it on my own, here’s a picture. I needed Mr. ODA’s help with the supply lines because I lost patience with how tightly they were screwed on and my lack of progress. I cut the baseboards down to size, except I somehow measured wrong on one quarter round cut (I was cutting while it was on the wall). Mr. ODA cut and installed the replacement piece for me.

We finished up the ski season. The kids did great. I was really proud of them for sticking with it. We used our season pass well (i.e., exceeding the cost had we bought individual tickets for each visit). I took two of the three kids to the aquarium, and we took the baby for a procedure at a local children’s hospital. We’ve started tee ball for our oldest. Our March is very full and busy, so we’re getting into the swing of things and keeping track of the schedule.

NET WORTH

Well, we far exceeded that $4 million goal. The market went up big, with our biggest changes being in our retirement account, IRAs, and cash. Our cash increase is offset by the lower amount in our Treasury account. Some of the short term bonds were transferred back into our savings account, and we’ve kept that money in savings since our deck replacement is slated to begin.

I keep updating my investment property tracking spreadsheet to reflect the current costs of insurance and taxes. My tracking shows last year’s amount, which I use as an indicator on whether I need to look further into this year’s bill (e.g., is the amount a reasonable increase?). For so many years, most of our insurance policies changed by a few dollars; now, I’m seeing large swings in what’s being charged. Where jurisdictions were slow to change property assessments, they’re now catching up, which increases the taxes.

As a renter, your rent is increasing to cover these costs of the landlord/owner. Here’s a comparison of my fixed cost increases against my rent rate increases. As you’ll see, I’m not trying to get top dollar out of these properties because the market has increased so much (and that leaves me more exposed if someone doesn’t pay their rent on time). My rent increases barely cover the cost increases that are happening on some of these houses. Remember that while I’m showing fixed costs, this isn’t covering the maintenance calls that I receive and how they’re more expensive than they once were also.

ESCROW, CONCEPTUALLY

In most cases, for a traditional mortgage, an escrow account is set up. It calculates your taxes and insurance payments for the year, divides by twelve, and is added to your principal and interest payment for the mortgage. In addition to covering the total payments to be made, there’s also a requirement that the balance of the account never falls below twice the required monthly payment.

If your taxes owed for a year are $1500, and the insurance is $300, then your monthly breakdown is $150 ($1500+$300=$1800; $1800/12=$150). The minimum monthly required balance is $300 (twice the $150).

As taxes and insurance increase each year (typically), there’s an analysis done to ensure the projected monthly balance never falls below that $300 threshold. If the balance is projected to fall below the required minimum amount, then it triggers an increase in your escrow payment. Your escrow payment will increase to cover the shortfall, but also to cover the new projected costs to be paid. So while you may be offered the ability to make a one-time payment to cover the shortfall, your mortgage payment may still increase to cover the projected costs. For example, if last year, your tax payment increased to $1750, and your insurance to $350, then your monthly payment to cover those charges is $175 ($1750+350=$2100; $2100/12=$175). Your mortgage will increase by $25 per month because now your escrow agent knows the projected costs to cover are higher.

The analysis uses the current year’s amounts owed to project the coming year’s monthly balances; it doesn’t account for the probability that these amounts increase each year, which essentially means that there’s perpetually a shortfall. In other words, while in Year3, they know that there was an increase in costs from Year1 to Year2, they don’t inflate the costs of Year2 to cover Year3 projected payments.

I prefer to not have an escrow, but at this point, for any mortgages we have, they’re all escrowed. We have six of thirteen houses with escrow. While I pay more as my mortgage to feed into that escrow account, it means I don’t have to manage the annual or semi-annual payments. On the contrary, this means I need to be managing our finances to prepare for large outlays throughout the year on seven houses (in the last quarter of the year, I’m paying out over $8,000 to cover taxes owed).

ESCROW REANALYSIS

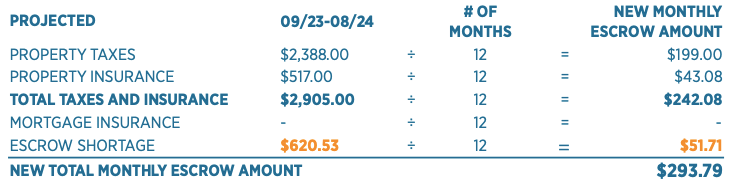

This post was prompted by a notification that an escrow reanalysis was done on a mortgage that was just transferred to a new company. I thought that their break down was the most clear I’ve seen. A quick note – your escrow will pay the bills that come due, regardless of the balance in the account, even if it means it’ll overdraw the account.

They clearly showed that the anticipated property taxes are projected at $199 per month (although, I’ll reiterate that this is based on last year’s actual outlay numbers, which aren’t accurate for the coming year). Then they show that the taxes are $43.08 per month. They then go as far to show the total of these two required outlays. There’s verbiage that explains the required minimum in the account must be twice the total taxes and insurance ($242.08 * 2 = $484.16).

There’s another detailed breakdown of each month’s escrow income and outlay (that I don’t have pictured here) that shows the month that is projected to fall below the required minimum. That month’s account balance is -$136.37. The difference between the required amount of $484.16 and the negative balance of $136.37 is $620.53 (pictured above). When that’s broken down by month, it’s $51.71. Take the total taxes and insurance payments and add the shortage amount to get the new monthly escrow amount of $293.79, a change from $222.25.

Below, they show you that there is no change in the principal and interest payment, then it shows how the current escrow payment is adjusted to the new escrow payment, along with the shortage amount.

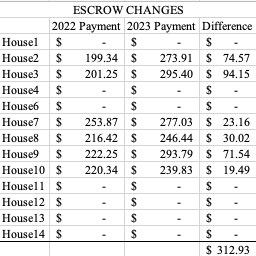

I created this table to show the differences between escrow payments over the two years. I kept the houses that don’t have an escrow because it can be compared to a future table in this post. There is no House5 in this table because we sold it several years ago (houses didn’t get renumbered because House5 still exists in terms of tax documentation).

TAX AND INSURANCE UPDATES

Each year, we see an increase in these amounts. Usually it’s across the board, but Kentucky districts had kept the housing assessments the same through the pandemic. As housing prices increase, your property assessment can be increased by your tax jurisdiction. The assessment increasing leads to an increase in taxes. This is why people getting excited that house prices in their neighborhood are selling higher than expected isn’t great if you’re not planning on selling any time soon; those increases in values means you’re paying higher in taxes.

In Richmond, VA, the property taxes are $1.20 per each $100 of the assessed value. In 2022, House2’s value $163,000. In 2023, the value was increased to $203,000. And let’s not forget that we purchased the house for $117,000. While it’s nice that the home values in the neighborhood are increasing significantly (and we knew the area was going to get better and better based on development happening), we can’t realize this gain until (and if) we sell. So in the meantime, we’re paying higher taxes on this amount. Although, I suppose the assessment could be even higher because the actual value of this house is probably more like $260,000.

Among 13 houses (don’t get confused – there’s no House5 up there because we sold it), I need to cover a total cost increase for taxes and insurances of over $4,500. This doesn’t include the higher costs of trades people if there are any maintenance calls, so this increase is the bare minimum for me to keep my same income.

RENT INCREASES

I constantly see complaints about the cost of rent, or that a landlord is increasing rent. Unless we’re looking for a tenant to move, our general philosophy is to increase rent $50 every two years. This worked fine because home assessments increased at a slow, reasonable rate until recent years. Now jurisdictions are capturing these larger increases based on those inflated sale numbers when competition was high in from 2020 through 2022.

In some cases, the rent for the area brought it in a higher amount than compared to our purchase price of a house. In those cases, we went several years without increasing the rent. Looking back, that probably wasn’t the best idea because now we’re behind on capturing how significant these last few year’s fixed costs have increased. However, the trade off to that is that we’ve kept great tenants in the house, haven’t had to pay to turnover the unit, and have minimal maintenance calls.

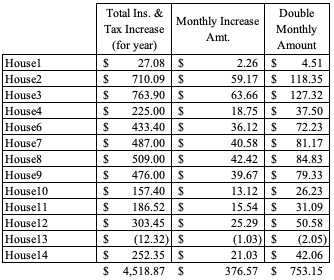

This table shows the total increase in insurance and tax payments from 2022 to 2023 in the first column. I divided that by 12 to get the monthly amount of that increase (second column). Then, since I said we typically increase our rent by $50 every two years for the same tenant, I multiplied that monthly amount by 2. I’m showing that if we want to only increase rent on long term tenants every other year, then I need to plan ahead on how much my costs are increasing.

This isn’t a perfectly accurate capturing of our cost increases since I’m not going back to 2021 to capture those changes in amounts, but it’s a general estimate. This shows that if I were to increase all houses by only $50 every two years, it’s cutting into my bottom line. Only 6 of the houses have increases less than $50 for two years.

SETTING THE RENTAL RATE

Let’s pause and talk about “bottom line.” Landlords have investment properties to make a profit. They’re looking for an income stream.

I regularly hear people say they can own a house for less than their rent, which is likely if you’re speaking only on principal and interest of a loan. However, you need to qualify for that loan. You may not have 20% down, so you may be required to pay private mortgage insurance (PMI). You may not have good credit, which means you’re probably going to pay a higher interest rate than I’m currently paying. You need to be able to cover taxes and insurance, which means you’ll have an escrow account set up, which increases your monthly mortgage payment. Then there’s all the other costs of home ownership.

That’s where people forget. When your hot water goes out, you call me. I spend $1,500 for about 2 hours worth of someone’s work to replace that. When you have a water leak, I spend $3,000 for a day’s worth of 2 plumbers’ work. When a storm drops a tree on your house, I’m the one spending hours on the phone with insurance, finding a contractor, getting quotes, and paying the contractor $3,700 before I get insurance reimbursement. Those are the big unexpected expenses. That doesn’t include all those smaller plumbing problems that cost $200 or $500 at a time.

Then in some cases, I probably put time and money into the house to even get it ready to rent to you. I didn’t always buy a house that was ready to live in. You may have projects that need to be done when you first move in also, so which costs money. Those are expenses that I’m trying to recoup through my rent rate also.

There may be other costs to my ownership that I’m trying to recoup through the rent, such as property management. I may have to pay someone else 10% of the rent, every month. I am projecting that there are going to be costs that I need to pay for also (e.g., water heater, roof replacement, plumbing issues). When I need to pay a plumber $3,000, I’m not coming to the tenant to say “I now need $3,000 to cover this cost.” Instead, I’ve set my rental rate the expect such a large payout on my part.

Not only am I trying to make sure that my rent is set at the right about to cover the costs that I’m putting into owning and maintaining the house, I’m also hoping that I’m going to make some money off owning this house so that I can live. I don’t get to pay myself for the hours I put into managing the property. Whether or not I have a property manager, there is still time that I put into managing the houses. Would you want to work for free?

BACK TO RENT INCREASES

While we manage each house individually on setting the rates (asking ourselves: do we think the tenant can absorb the increase, do we have to increase to cover actual costs now), this shows that our monthly income was increased by $475. If you look back at our total monthly increase in expenses of just taxes and insurance, it’s about $375; add in the cost increases for property management (increased rent means increased fees because fees are based on the rent price), and our fixed costs went up $415. On a whole, we’ve offset the increases.

However, you can see if we had one or two houses, some of those increases could be significant. House3 is costing us $64 more for each month, but our increases are typically about $50 at a time. We’ve had the same tenant in this house since we bought it. A $50 increase every two years hasn’t kept up with our costs. Since we have other houses, it helps cover the costs on House3.

House2 and House3 are identical in layout. House2 has been upgraded to all LVP, whereas House3 has carpet everywhere except the kitchen and bathrooms (granted, it’s new carpet two years ago). Since we purchased these two homes with tenants, rent was already set for us. House3 has been the same tenant since we bought the house, and the increases have brought us to $1200 per month in rent. House2 has been turned over 3 times: the first was a divorced lady who moved back in with her ex-husband; the second was there for several years, but we began having a lot of issues with her, and we told her the lease was up; the third was the one who flooded the house in December, and causing the need for the fourth. Now we’re renting that house at its market value of $1600. That means House3 is operating at a much lower rent than we could get if we rented to new tenants. However, the tenants are wonderful, and we’ve purposely not raised the rent on them in significant ways because we don’t want to cause them to move.

SUMMARY

Cost increases in rental properties can be significant over the years. With the rising costs of all goods and services, property values weren’t immune. The increase in property values leads to an increase in an assessment, which means an increase in taxes. That cost is relayed to the tenant, as this is a for-profit business. I’m trying to make an income for my family with rental properties.

I’m not trying to price gouge tenants, but make a fair living based on the costs of owning these houses. My first goal is to not turnover tenants, so I do what I can to make my tenants happy by taking care of the houses and not creating drastic rent increases each year. Secondly, I’m not going to set a price that my tenant can’t afford, thereby putting me in a hard position where I don’t have rent paid. Having multiple properties helps to offset the costs so I don’t have to play catch up on one or two houses worth of higher expenses, by putting my long-term tenants in an uncomfortable position where they can’t afford the rent.

Over the past year, I tried really hard to stay on top of sharing content here, until I finally had to throw in the towel. It started because we were renovating a house while I was pregnant and had two kids to take care of, so my posts dwindled down to just the net worth updates. Then Mr. ODA started investing in treasury accounts. There was so much movement of money in so many different accounts, that I couldn’t quickly update our net worth anymore. Other than updates of the net worth and rental property work, my last post was August 2022. I feel like I have the bandwidth to finish several posts that I’ve started, so I’m back.

NEW HOME

In May 2022, a house went on the market in our desired area of town. We weren’t ready to leave our house since we hadn’t owned it for two years yet, but this was an opportunity that was hard to pass up. We closed on the new house in June 2022. We floated the down payment through a Home Equity Line of Credit that was paid off through the sale of our house.

We spent the whole summer traveling back and forth between our then-current house and the new house because we had a lot of work to do on the new house. We demolished the master bathroom and started rebuilding that. I painted almost the entire house. We did a lot of little projects. It was a tiring time that culminated in having to do the physical move in the Fall and get the new house organized and set up.

NEW BABY

I was pregnant through all of the home renovations and move. Our son came 3 weeks early on Thanksgiving day. He was generally healthy, but he required extra medical attention than we weren’t used to with the first two. On top of that, he wanted to be held to be asleep; babies sleep a lot. Mr. ODA and I were taking turns holding the baby and sleeping. The two older kids basically survived on tv shows and chicken nuggets during this blur of life. Going from 0 to 1, and from 1 to 2 kids was pretty easy, but this 3rd kid was a new ballgame. Once he was 5 months old, I started working on getting him to sleep independently. Now that he’s 7 months old, he sleeps well in his crib for his naps and through the night; he’s happy during the day and plays well; and now I feel like a new person for actually getting rest and not being tied to a couch all day everyday. Mr. ODA took a lot of time off to help me through that phase. As he started working again, it was an adjustment for me to learn how to manage all 3 kids and the household.

PERSONAL

We had several trips last summer on top of the renovations that we were working on. Those created delays in us having the house ready for us to move. Then our oldest got sick and it turned into an issue in his leg so he couldn’t walk at all for about 2 weeks and couldn’t walk right for about 8 weeks. It was a rough time. He got better just as I was about to have the baby.

As we started to get into the swing of things with all 3 kids and coming out of winter, my mom got sick. She went downhill quickly in March and ended up passing away on my birthday this year. That was unexpected and emotionally draining. We just got back from a trip to see my family, and I feel like I’m more put together than I had been over the last 3 months.

In April, we had to submit our taxes. This is always a several hour process. I had documented in the past, but I just didn’t have time to juggle it this year. I have to verify that I’ve recorded all expenses, that I haven’t recorded expenses that aren’t supported by documentation (e.g., receipt), that my summaries are logical, and then it takes Mr. ODA and I 5-6 hours worth of entering data to actually submit.

Then we added swim lessons and soccer for the kids. We quit soccer early because it just wasn’t fun for our oldest (or us), and 3 months of swim lessons are over. Now our only commitment is whether or not we want to attend library story time for a half hour each week, and I’m appreciating the open schedule.

BUSINESS

The rentals have required a lot more than usual attention from us in the past year. We had a house flood from a burst pipe, so that had to be cleaned out, renovated, and re-rented. We had several plumbing and HVAC issues among multiple houses, as well as a raccoon removal issue. We had roof damage to a house, a tree fall on a house, and another tree fall in the yard of three different houses, all because of storms. We had to turnover a house, where the tenant had lived there for several years, had made changes that were not appropriate, and would not communicate effectively on her status of leaving. It has been a lot more than usual, requiring a lot of time to manage.

On top of the maintenance requests and the usual management of the properties, I also took over the management of the properties that are in Central KY in February. I was spending so much time managing the property manager, that it was finally time for me to just handle it.

Not that you needed all this background, but I felt weird just jumping back into content. We’ve been very busy in general, but adding a 3rd kid into the mix was the straw that broke the camel’s back. I finally feel like I can manage everything again, and I’ve had more and more thoughts for things to share.

Well, Mr. ODA didn’t like that I shared I didn’t know where our money was last month. They’re all kinds of Treasury accounts, and I’n just logging the transactions and leaving him to it. 🙂 I don’t have a lot of bandwidth these days, but I’m learning to juggle 3 kids and our finances.

PERSONAL FINANCES

We bought a new van this month. We’ve been wanting a new one for a while now. We bought our 2017 Pacifica in September 2020. It was a great deal, and it was a necessity as we were about to spend 7 weeks “homeless” and AirBnB/couch hoping. The car had some defects. We decided we’d keep an eye out for a newer version. Suddenly, Mr. ODA found a good deal on a 2020 Pacifica that had more options than we were actually looking for. We drove to Ohio about 36 hours later. They made us a good deal for our trade-in, and we went home with a new van! We put some of the purchase on two credit cards and then the balance with a personal check.

We’re currently paying close attention to credit card deadlines and our savings account. Where I used to pay a credit card bill almost after the statement closed so that it wasn’t hanging out there and I wouldn’t accidentally miss a deadline, I’m now leaving money in our savings account as long as possible. Our savings account is now earning 4% on the balance, so we’re seeing a significant amount of interest each month. I’m juggling managing our bills as close to their due date as possible, while also projecting future bills necessary since there’s a limit of 6 transfers out of the savings account per month.

All that was to point out that our credit card balances are high right now because of the van purchase, but the credit card statement hasn’t closed yet. Instead of paying the credit card balances down right now, the money is sitting in savings earning interest for 4-6 weeks between the purchase, to the statement closing, to the statement’s due date. More directly, we put $3,000 on one credit card for the van purchase. That was on 2/7. That statement, once it closes, will not have a due date until 4/20. That means that the money put on the credit card can sit in savings earning interest for about 70 days.

We also had to pay the initial payment for the restoration services on the rental that had a burst pipe. So while the insurance company sent us a check to cover the cost of this work, it’s still $17k sitting on our credit card, not being paid until the last minute. I should also note that our cash balance is inflated by about $50k because it’s the money from the insurance company that we’re waiting to pay the contractor as milestones are completed.

Had I seemed nonchalant about the plan? Because I’m definitely not. 🙂 I need to stay on top of how many transfers happen per month out of the savings account (while Mr. ODA randomly pulls money for investments), and not miss any deadlines and cost us interest charges or late payment marks on our credit. It’s stressful! Since we’re not doing anything that requires our credit to be pulled right now, it’s fine. If we were having our credit checked, having multiple cards nearly maxed out would be a problem. But we know we have the cash available to pay off all the credit cards if we needed to.

RENTAL FINANCES

I finally got through to someone on the issue with the improperly installed water heater. He says he submitted all the paperwork to send us a check for $200 to cover the plumber we paid to fix their issue. I haven’t seen any paperwork, nor have I received the check, but I’ll keep it on my radar and follow up in a couple of weeks.

I made all the decisions on the restoration of our flooded house. We’re expecting to hear a timeline for work to start next week, and then it’ll take about 40 working days to get the work done.

I paid a warranty for termites on another house. We had an infestation when we purchased the house, but we didn’t pay the warranty information. Our tenants found swarmers, and when we called to ask about treatment, they said they’d let us backpay the warranty and invoke that. We have a good relationship with this company and appreciated that offer, so we’re staying on top of the warranty payments now. The payment is $98 per year.

We received a surprise in the mail – the tenant had turned off the electric in the flooded house back on January 12th. The power company is supposed to notify me. I received an email on February 6th notifying me of an action on the account. So this was in my name from 1/12 to 2/1 for me to be billed $255 without my knowledge. Not to mention, there’s a bill hanging out there from 2/2 until the present that I’ll also get billed for. Mr. ODA sent our property management excerpts from the lease indicating that the utilities must be in their name for the entirety of the lease, that they’re responsible for this bill, and that they must get it back in their name immediately. We’ll see how that plays out.

RENTAL WORK

I picked up the keys from our property manager for the 3 houses I took over managing. I also worked on a rental here in town this week, which took about an hour including travel time, and I have another to work on later this week, which will be about 2 hours worth of work.

I sent a prospective tenant the pre-application we have, which he passed, so I sent him the application to submit. If all goes well, we’ll have that house re-rented with no vacancy period.

We have 3 leases that end at the end of April. We put a requirement that tenants give us 60 days notice, or that we give 60 days notice of any changes. That means that these leases need acknowledgement by the end of this month. So I ran the analysis on those 3 houses. We decided to increase the rent on 2 of them by $50 per month, each, and we’ll keep another house the same since it was increased last year. One house actually had an increase last year, but that house is well below market value, so we’re offering them to continue the lease with an increase because if they were to move out, we could get even more from the house based on it’s size and demographics. The 2 houses we’re increasing have a property manager, so she’s responsible for notification and signing an addendum before the end of the month. But once again, I need to manage the property manager and ensure we have action on time.

Surprisingly, I didn’t cover all our houses in posts last year. I was going to say, “let’s finish this up,” but we’ve since purchased #14! This is a long post. I tried to separate the stories, but since they were part of the same purchase, it was too convoluted to decide which story went with which house.

We spent the summer of 2019 living in Lexington, KY. Mr. ODA took a temporary job for 3 months, and we spent our summer looking for more rental properties to try another market. The housing costs in central Kentucky were less than central Virginia, but the rental rates were also lower.

We drove around with our Realtor for quite some time. We were hoping to find a multi-door complex. However, 4-8 door units have just not been well taken care of. We take care of our houses, and I didn’t want to inherit all the deferred maintenance of a poor landlord. Many of the places had long-term tenants, so there wouldn’t be a vacancy to ease getting work done either. Additionally, there were several that we saw where the tenant was home, smoking and telling us all that was wrong with the property. It was abysmal.

So after searching through many other options, we settled on two houses at the same time.

FIRST OFFER

Mr. ODA actually made an offer on a house in Winchester that I hadn’t seen. It was a large house that had been converted into 2 units. Mr. ODA and our Realtor went after work one day, and it wasn’t worth me packing up the baby and driving a half hour to meet them for one house. However, I did get to see some of it because I took on the home inspection appointment. Since I had never walked through the house, it was easy for me to objectively see the information on the inspection and convince Mr. ODA to walk away. There was just too many big-ticket items (e.g., not enough head room for stairs, water damage not properly cleaned up in multiple rooms, several code violations) and deferred maintenance that it wasn’t worth us putting the money into it. The tenants were sitting on the porch smoking during the inspection, and I didn’t love the idea of inherited tenants that were allowed to smoke in the house.

SECOND OFFER

I can’t tell the history of these purchases without this gem of a story. Mr. ODA found a house that was in a decent shape in Winchester.

Aside: We focused on Winchester because while the rent income was low, the housing cost was also low. Whereas in Lexington, the rent was low, but the housing prices were higher.

We made an offer on the house. In the offer, it lists the seller’s name. It was a State Senator! When we sent over the offer, the seller’s agent agreed to our details, but asked for a pre-approval letter before he’d sign. The amount of weight the people in Kentucky put on a pre-approval letter is absurd, in my opinion. We went through the effort to get the letter and send it over. About that same time, the seller’s agent said someone else came in with a better offer, so we could either submit our highest and best offer, or lose the deal. The sketchiness of the action floored us.

The house had been on the market for a month. We had a verbal agreement (that had even been put in writing, but not yet signed). What are the odds that someone came in at the same time as us with an offer over asking for a house on the market a month? We called his bluff, and we were wrong.

THIRD AND FORTH OFFERS – UNDER CONTRACT

In August 2019, we went under contract on two houses in Winchester, KY.

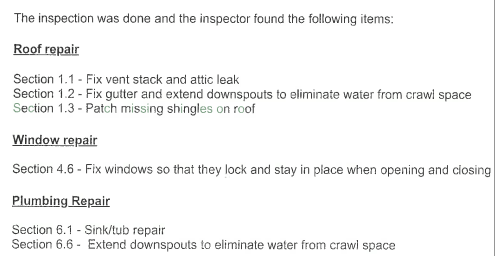

Property12 had been owner occupied and flipped to sell. The owner had lived there long enough that she wouldn’t Docusign the contract, and we had to wait for her to initial, sign, and date all the pages by hand. The house had been listed for 36 days when we made the offer. It was listed at $115,000, and we went under contract at $112,000 with $2,000 in seller subsidy (closing costs) on 8/7. It’s a 3 bed, 2 bath ranch at 1120 sf.

We received the home inspection on 8/14. We asked for the items below to be addressed, or to take $1000 off the purchase price. They agreed to fix the issues.

Property13 had been listed for nearly 3 months before we made an offer. It had been most recently listed at $105,500. Our offer was for $102,000 with $2,000 seller subsidy. We also included the following requirement in the contract: Seller agrees to remediate the water and mold in the crawl space, fix the down spout next to the crawl space door so that it channels the water away from the home, replace the missing gutter on the front of the house, and repair the rotted facia and sheathing on the front of the house.

Additionally, we had a home inspection on the house and identified the following items for them to repair.

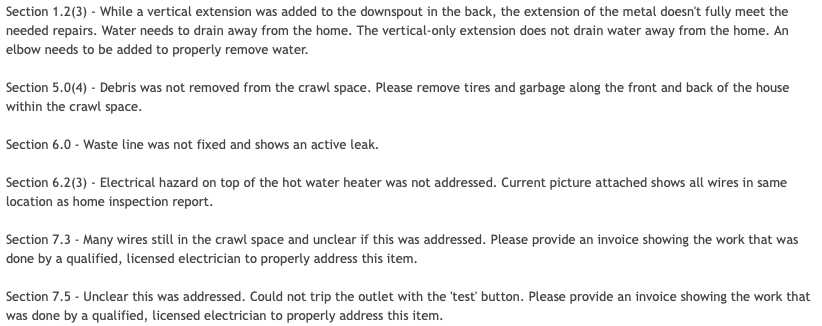

Getting the sellers to identify that these items were done before closing was not an easy task. We checked the day that closing was originally schedule for and noted that several things were not complete.

Then, at 7:30 pm the night before closing (which had already been delayed a week), we received one receipt identifying a couple of things were done. Eventually we received documentation that it was taken care of.

LOAN DETAILS

The options we typically ask for when considering the direction of our loan are as follows.

We chose the 25% down – 30 yr fixed option for both properties. Our goal is to not pay points, so that led us to the 25% down options. Since there was no incentive to take a shorter term (thereby increasing your monthly mortgage payments and decreasing your cash flow), we chose the 30 year option.

These loans were originated in September 2019. We processed multiple cash-out-refinances on some of our properties in December 2021; we used it to pay off about $66k on Property12 and about $74k on Property13.

LOAN PROCESSING & DELAYED CLOSING

We had a lender that we loved in Virginia. She couldn’t cover loans in Kentucky, but the company itself had a branch that could do it. She referred us to someone in Kentucky. It was the worst experience I’ve had in closings. Our closings are always annoyingly stressful in that last week, but this was bad throughout the month and then bad enough that our closing was delayed a week – completely due to the loan officer’s inability to manage the loan.

We had multiple issues over the course of the week we initiated our relationship just accessing the disclosures. They kept telling us to sign things we didn’t receive, or they’d tell us our access code and then when I say it doesn’t work, act like they never told us different information and give new information.

On August 16, I had to tell the loan officer that one of the addresses was wrong. THE ADDRESS. On August 26, we received conditional approval of our loan from underwriting. On August 27, we received our appraisal with no issues noted. But at that point, our August 30 closing was delayed a week already.

That’s where the problem was – our appraisal was ordered late, had to be rushed, and still didn’t make it in time for them to develop the Closing Disclosure (CD) and get us to a closing on August 30. The loan officer never once acknowledged that he ordered the appraisals late, causing this delay. It took asking for timelines from his supervisor, and piecing together emails we had on hand, to show that it was his fault.

On August 29, I finally made contact with the loan officer’s supervisor and was rerouted to someone else to get the job done. I had to repeat all of our issues and the errors that were found on the CDs.

On September 3, I was given disclosures that were still wrong. The new loan officer claimed that what she put in the system was correct, so she wasn’t sure what was wrong, causing me to once again outline all the errors.

On September 4, I was asked for more documentation that wasn’t caught during underwriting. I was furious.

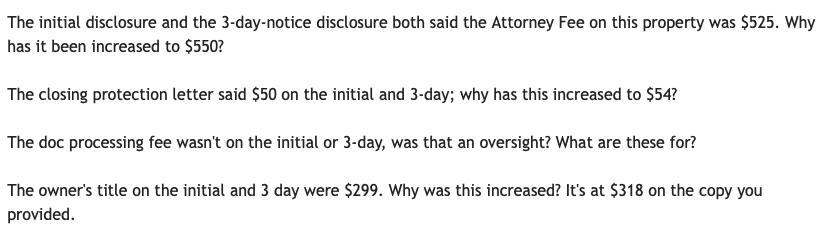

On September 5, I gave up talking to our lender about issues on the CD and spoke directly to the Title Attorney’s office, who was much more knowledgable and responsive. Here’s an example of what I’m questioning when I look over a CD. Some of these seem small (e.g., $4 difference, $25 difference), but you can see how these add up, both on a single transaction and when we’re processing several homes in one year. Not to mention – why pay more for something than you were quoted or you’re supposed to?

Another surprise that came our way was a “Seller Agent Fee” for $149 per transaction. At no point in time was an additional fee disclosed to us by our Realtor. A typical transaction has 6% commission paid by the seller, which is traditionally split 3% and 3% for the buyer and seller representation. Being that these were Rentals #12 and 13, in addition to 2 personal residences we had purchased, imagine the surprise when we, as buyers, were being charged for representation. We questioned why this wasn’t disclosed to us up front as a Re/Max requirement, and it was taken off our CD.

CLOSING DAY

I had planned to leave town the Friday after the original closing date because that was the last date that we had our apartment. I didn’t want to move me and the baby into my in-laws house and continue the poor sleep we had been dealing with by not being at home. So even though closing was delayed, I left. Mr. ODA had to be my power of attorney. He had to sign his name, write a blurb, and then sign my name on ALL those papers that are part of a closing….. times two. Eek. I didn’t know that at the time (but baby went back to sleeping perfectly once we were home, so it was worth my sanity 🙂 ).

At 11:30 am on closing day, the lender claimed that the power of attorney documents (from the lawyer…) were not complete enough to be counted as filed on their end. I appreciated the snip from the attorney when questioned.

I always wondered why tv shows always showed both at the closing table with a ceremonious passing of the key. We’ve had our share of weird closings (in a closet, in a parking lot, at our dining room table), but we never sat at the table with the seller in Virginia. We were so confused about how specific the closing attorney was being about the closing time options, and then we found out that the seller and buyer are at the table together in Kentucky. The seller for Property12 was so rude to Mr. ODA through the transaction! She kept grilling him on whether he addressed the utilities. The seller shouldn’t be allowed to talk to the buyer! We’ve since been able to process 3 transactions in Kentucky and avoid the seller at the table, but I’d like to advocate that Kentucky move away from this buyer/seller meeting process!

RENTAL HISTORIES

Property12 was listed at $895 on 10/2. Based on my birds-eye-view of the area, I thought $1000 was going to be easy to rent it at. Based on the 1% Rule that we had followed in Virginia, we should have a goal of $1,100 per month. However, we were trying for a Fall lease, which is more difficult than a Spring lease, so I thought listing at $995 would get quick movement instead of letting it sit for too long. Our property manager disagreed. She also said we were limited our pool of candidates by not allowing smokers; but, the whole house is carpeted and I was not budging on that.

We found a tenant on October 16 and allowed her to move in right away, but not start paying rent until November 1 if she agreed to an 18 month lease (we really wanted to be on a Spring renewal going forward). That was an unfortunate blow to our expectations – nearly two whole months without rental income on a house we didn’t need to do any work to.

We increased rent to $950 as of 6/1/2022 after no previous increases.

Property13 was listed for rent at $995 with no movement. We dropped to $875 and offered free October rent for however long was remaining in the month. A lease was established on 10/18/2019. Our property manager was supposed to establish an 18 month lease and didn’t. Luckily, the tenant agreed to a 6 month extension.

Property13 renewal came in April 2022. She had balked about the state of our economy in 2021, and we backed off the proposed increase at that time. Well, all the jurisdictions finally jumped on the increased assessments, and we saw a drastic increase in our costs. We told her that the new offer for a year lease is $950, which is higher than we’d typically increase in one year ($75 instead of $50). But we told her that we were willing to let her walk if she didn’t agree to it since she originally negotiated a lower cost and argued an increase at the 18 month mark, which we let go. She tried to fight it, but our property manager told her to check the rental options in the area to see that she’s still getting a deal. She agreed to the increase.

MAINTENANCE HISTORIES

Property12 requires a new heat pump in June 2021. We paid $3900 for a whole new system, which is a funnily low number just a year later.

The tenant there complained of high water bills. I asked to see a history of the water bills to know how much was considered higher than their average usage. The property manager agreed that the toilet was running and causing higher bills, but also admitted that they attempted to fix the toilet twice over a 3 week period, with multiple days between receiving a maintenance request and taking action. While I agreed that we could compensate her for the issue, I couldn’t quite pinpoint why this was my financial burden and neither the tenant’s nor the property manager’s. I followed up with more information from the property manager with questions like: Why did it take the tenant from 9/20 until 10/11 to identify the issue still remained and that there was a waste of water? They indicated that they believe they made a good faith effort to address the issues as reported. I eventually settled on a $25 concession on one month’s rent.

Property13 had several issues with the hot water installation that were eventually resolved, which was frustrating after we tried to manage issues with the hot water heater through the home inspection process and received documentation as if it was complete. The tenant requested pest control in July 2020 claiming that a vacant house next door caused an increase in pests. I was frustrated because that’s not how it works. I approved treatment at that time, and then she came back with another request in October. Luckily, I haven’t heard about pests since then. In my Virginia leases, we’ll handle some pest control requests, but if there are roach issues once a tenant has been there for some time, we don’t typically pay for that type of treatment.

SUMMARY

All in all, these tenants have been pretty quiet. They ask for random maintenance things here and there, but they’re not usually big-ticket items (except that HVAC replacement!). Our property manager has been more difficult than the tenants.

Being that we were used to the 1% Rule when we purchased these houses, it’s unfortunate that even at 3 years in, we’re not renting it at 1% of our purchase prices. Our cash-on-cash isn’t completely accurate right now because I won’t see our taxes for this year for another month or two. Being that jurisdictions kept the tax amount steady through the pandemic, I’m expecting to see an increase in assessments for this year. I’ve also seen big increases in our home insurance policies, so that will probably eat into our cash flow as well. Our cash-on-cash analysis on Property12 is about 6.5%, and it’s about 7.5% on Property13. These numbers are only slightly lower than our expectation/desire, with our average being about 8%.

In the upcoming year, we’re going to look to get rid of our property manager, so these houses may begin needing more attention from us. It’s been hard to take on more when paying a property manager has been a sunk cost at this point. However, the frustration of managing their management (e.g., making sure charges are correct, not getting a full picture of what work is being done, and then paying them a significant amount of management money and leasing money only for them to claim that checking on the property requires additional fees) has led to us wanting to take it on since we’re in town now. The current lease terms are up in April and May, so if we’re going to take on management, it should be before the possibility of paying them half a month’s rent for leasing it (not to mention they’re notoriously 4-6 weeks out in every leasing attempt they’ve done for us, whereas I’ve never had an issue getting a property leased within a week).

The market has recovered a good bit, so our net worth jumped. Our retirement accounts were at an intriguing low, but they’re back on track now. We also saw a few sales in the neighborhoods where our rentals are, so that increased our net worth based on the comps. We added a new property over the course of the last month as well.

NEW HOUSE IN OUR PORTFOLIO

We closed on a new house on March 24th. We worked on it for a few days, I held an open house, and we were able to get it rented as of April 8th. We had 16 days of vacancy. While showing it, most people were looking for a May or June start date, so we were lucky someone qualified for an April date. Back in 2016-2019, we were looking to follow the “1% Rule.” That means that if you buy a house for $100,000, your goal is to set rent at least $1,000 per month. This house isn’t even close. This market doesn’t allow for such a goal anymore because housing prices are soaring. The next goal would be to list for about $1/square foot. This house is 2100 square feet, but since the upstairs has smallish rooms and the basement is all open, we thought it wasn’t really worth pushing for $1/sf.

We bought it for $240k net, and ended up renting it at $1750. I wanted $1800, Mr. ODA wanted $1695, and when I went to list it, Zillow suggested $1750, so we went with that. Multiple people commented on how they appreciated the price, so we may have been able to get $1800 without an issue. I’m happy to have it rented, and I think these people are going to take good care of the house.

RENTALS

We put more money towards the house that we’ve been paying off, which is owned with a partner. We put our half towards it ($8,500), and it has a balance of about $600 now. The pay off quote required us to pay the anticipated taxes that will be paid out of escrow in May. We didn’t appreciate that, so we just went ahead and paid it down. We’ll let the May mortgage payment go through, wait for the taxes to get paid out of escrow in mid-May, and then pay it off. That’ll make 7 houses that are owned outright! But that also means I need to stay on top of insurance and tax payments.

We were just informed that one of our properties in Lexington that’s under a property manager hasn’t paid rent. She said it’s unlike them and that they aren’t even responding. She’s going to go to the house tomorrow to check on the situation. Since we’re paid a month after rent is received, this hasn’t affected us. A neighbor reported that they were moving out last month, but the tenant denied it. Perhaps they abandoned the property.

Once again, our two usual suspects didn’t pay rent on time. However, both of them actually made a better effort than they have been. One has paid this month’s rent in full, but has a balance of $286.31 (seriously…) to make up several late fees. I’m happy to waive late fees when it’s someone who communicates and isn’t always a fight to collect rent, but I’m holding this one to the balance owed. Another one told me that they wouldn’t pay until the last Friday of the month. I drafted an email to tell them that this is unacceptable because it’s been several months that they’re paying this late, and we need to work towards getting back to paying rent at the beginning of the month. Right after I drafted that, she sent half of this month’s rent. Better than nothing!

SPENDING CHANGES

Over the past month, we didn’t go out to restaurants very much. We haven’t been traveling because my family came into town for our daughter’s birthday party, and then I’ve been working on the weekend. Most of our spending went to gas (going back and forth to Lexington (half hour drive) multiple times per week!) and expenses to get the new house ready for a tenant.

I’m flying to my sister’s baby shower next month, so that another large and unusual expense on our credit cards ($250).

SUMMARY

We still have our state taxes to get paid. We went through the process of entering all our taxes, but we haven’t hit submit just yet. Surprisingly, we’re expecting a refund from the Federal side. The amount owed and the refund basically end up as a wash.

Our new property’s loan is a commercial loan, so it doesn’t get paid on the typical mortgage schedule, but on the 1 month anniversary of the opening. Therefore, the next payment is due on 4/24, and there’s no “1 month without a payment” type thing.

Clearly, our cash balance dropped significantly since last month because we had the closing. That was about $46k that we wired out, which was the expectation when we completed all the maneuvering with the cash out refinances in January. Our credit cards reflect our lower spending too, coming in about half what the balances were last month.

We filed our taxes. It just takes so long, but it’s easy. This year I recorded what I did and how long it took, so I wanted to share.

I’ve shared that I record transactions all year long. Inevitably, a few things slip through a crack. So I go through everything I have on file to make sure I can support a charge I’ve recorded (e.g., receipt) and that I haven’t missed entering something in my spreadsheet (e.g., I have a receipt for work, but didn’t put it in my spreadsheet).

DC TAXES

Mr. ODA works for a DC office, but lives in KY. The paperwork information got crossed, and he ended up paying taxes to DC for a little while. Apparently DC is used to this mistake. There’s a form he filled out, attached a copy of his W2, and mailed it to DC. He received a full refund within a couple of weeks! I couldn’t believe the timing of it and how it easy it was!

STEP 1

My first step was to load all my mortgage documents for the houses that we still have mortgages on. I need to know the mortgage interest for the year and what they paid out in taxes from escrow. For some reason, it never tells me the insurance payments made on the tax document, so I need to go through my email or look at the line-by-line escrow to see when and how much was paid for insurance. I estimate the mortgage interest each year, but I don’t have the final amount until January.

STEP 2

Then I go through my email files. I try to get most of my receipts via email (e.g., Home Depot and Lowes are good about tying your credit card to your email address so I keep everything filed electronically). This took me just over 3 hours. I went through each email receipt to see if I had it recorded properly. I found 2 or 3 transactions that I had receipts for, but they weren’t recorded in my spreadsheet. I also found out that I didn’t record any of my final December transactions (i.e., stormwater utility bills and property management).

STEP 3

After I go through everything I can electronically, I move on to my paper files. We have a lot of our insurance through State Farm, and they don’t email me receipts for payment, nor can I look up previous payments made on their website. So I keep a paper copy of all the insurance documents for each house. We had a huge debacle with two of our KY houses and insurance last Fall, so I had to make sure I had all of that recorded accurately. I used to rely on the paper stormwater utility bills that I pay directly, but this year I just went into our checking account and verified the amounts that I paid against what I recorded. Since most of my transactions are kept electronically (especially with having property managers, so they’re sending me the bills they receive electronically), the paper checking was only about an hour this year. It used to be longer, but I’ve streamlined my electronic filing so mostly everything is in there.

STEP 4

After just over four hours of “prep” work, we move on to the tax software.

Mr. ODA entered our W2 information, we both pulled up all our investment account statements, and then we got into the investment properties. It’s tedious, and each year we have to remember how we matched our terminology to the system’s terminology (why can’t I keep better notes on this?!). We got into a groove and knocked out half the properties in about 80 minutes before taking a break. We focused on the 3 properties that we received one 1099-MISC for first, which involved going back and forth on some screens. Then we knocked out some of the easier houses. The next night, we finished off the rest of the houses in about an hour.

We usually call it complete at that time, but we don’t submit right away. We take a few days to see if we think of something we may have missed (whether investment property or personal finance), and then we submit. We usually owe Federal and State tax every year, so we’re never in a rush to get this done and pay. Somehow, we get a refund for Federal this year, but we still owe the State.

SUMMARY

About 6.5 hours of tax work, after being pretty on top of it all year. People ask us why we don’t use someone to do it instead of putting all that time in. It’s not that easy. If we had to send our information to an accountant, we still would have to gather all our receipts and send them over. I think it’s easier to look at my receipt and record it, rather than gather all my emails and send them to an accountant (not to mention Gmail is not a great mail system in this regard because you can’t easily add emails to new emails). Then we have to field all their questions regarding the documentation that I send, which will inevitably be frustrating to me. It’s all around cheaper and easier to do it this way.

Our 11th purchase was a 4 bedroom and 2 bathroom house, which we were excited about. We only had one other 4 bedroom, and it only had 1.5 baths, so this was a new demographic we could meet. We again needed a mortgage, but we were tapped out (max of 10 mortgages allowed per Fannie Mae), so we went to our partner. I went through the process of establishing the partnership in the House 10 post.

The house had been listed for sale in July 2018, dropped the price in October 2018, and we went under contract on it on December 1, 2018. We went under contract at $129,000, which meant, according to the 1% Rule, we would look to rent it for at least $1290.

The house required a lot of cosmetic work (relative to our usual purchases) before we could rent it. The biggest hold up was the carpet replacement, but we had to do a lot of cleaning and painting also. We closed on February 4, 2019; got to work on the house on the 6th; and then had it rented on March 3, 2019. That’s a longer turnaround time than we’d like, but we thought the long-term benefits of a 4/2 house would be worth it. Plus, with our goal being $1290 based on the 1% Rule, we were happy that we rented it at $1300 and through March 31, 2020.

LOAN TERMS

We were given two options from the loan officer. Both options required 25% down. We could do a 15 year mortgage at 5.05% or a 30 year mortgage at 5.375%. The 15 year mortgage payment was $865, while the 30 year was $640. Since both options required 25% down and we aren’t concerned with our monthly cash flow (as in, we’re not living off of every dollar that comes out of these houses right now), we chose the 15 year. Escrow changes over the last few years have increased the mortgage to $941, unfortunately. However, we’ve been paying off this loan with pretty substantial chunks of money thrown at it. The loan started at $96,750, and the current balance is $21,350. We would have liked to have this paid off a few months ago, but we need to time our payments with our partner, who recently paid for a wedding, renovations to a new house, and a new tear-down property adjacent to his personal residence that he’s going to build a garage-type thing (city living = street parking for him).

We went under contract at $129,000, and the house appraised at $140,000, so that was a nice surprise. The current city assessment is at $148k, but it would likely sell for more than that.

PARTNERSHIP

Since the LLC was already under way when we purchased House 10, we needed to add this one to the LLC. We contacted our attorney. He processed all the paperwork, and we showed up just to sign everything in a quick meeting. At this time, we also requested an EIN be established for the LLC. To process adding this to an established LLC, it cost us $168 (which we paid half of since we’re split 50/50 with our partner).

PREPARING TO RENT

This house was probably the second most effort we had to put in to prepare it for renting. We had to replace quite a few blinds that were broken, do a deep clean of everything, install smoke alarms, paint, replace the carpet, and do some subfloor work.

We had to paint nearly every room (one room we even painted the ceiling the same color as the walls because the ceiling was in rough shape, and it wasn’t worth the time for precision of the edges).

The floor at the front door was rotted by termites. The guys had to cut out the floor and replace the wood before the new carpet could be ordered. We needed the house treated for termites at that point since there was an active infestation that we found. Depending on time and price, I’d rather replace carpeted areas with hard surface flooring for easier maintenance. Since we were already losing time with all the maintenance on this house to get it ready to rent and it was a small area, we just went the easy way out and put new carpet in. The carpet was only in the living room and hallway; all the bedrooms have hardwood flooring.

FIRST TENANTS

We were able to get a family in the house fairly quickly after we finished our work. We rented it at $1300. They signed it on March 3rd, and I had set the terms until March 31, 2020 (this comes into play later). The family had been renting with a roommate (and the husband’s boss!), and that guy had wanted to leave the house. In January 2020, the tenant said, “we signed the lease on March 3rd, so we want to be out at the end of February.” That’s not how leases work. The lease signed said until March 31, 2020. Some time between us telling him that he was in our lease until the end of March, not February, and the end of February actually coming, they decided they wanted to renew their lease. They signed a new lease with us on March 11 to cover 4/1/2020 through 3/31/2021.

In April 2020, the tenant received a job offer in Texas. He asked about a lease break, and we offered an option. All the communication was done via text message, so it was technically in writing, but there was never a “wrap up” text that identified all the agreed upon terms to allow for the lease break. I used this as a teaching opportunity for the 3 of us in the LLC that clearly documenting agreements in writing (preferably with signatures) is important.

The tenant offered to pay May rent without prompting, so we thought that was covered. The part that needed to be detailed was what was considered a “lease break” fee. We had agreed to 60 days worth of rent, and the security deposit couldn’t be used to pay that. Mr. ODA tried to contact the husband on multiple occasions to get rent paid at the beginning of May, but there was no response. I finally sent an email, detailing that they agreed to pay May’s rent, and that technically, they were on the hook for the entire year’s worth of the lease (quick aside: while that’s what the lease says, I think a caveat in the law actually means they’re not really liable for the whole amount because once the house is vacant for 7 days, it defaults back to our ownership, and then we have to show due diligence to re-rent it, leaving them liable for only the gap period). Well, as usual, the landlord gives us a guilt trip (their daughter was in the hospital in TX) instead of separating that from the concept of “pay your debts owed.” As a person, I feel for you on this; as a business owner, it’s not my responsibility to manage your finances and personal life.

The tenant called Mr. ODA and yelled at him. A few hours later, presumably with a more clear head, we received a fair response via text. He even apologized for yelling on the phone. He paid the last few hundreds that were owed, and we all moved on.

SECOND TENANTS

After our first tenants vacated the house, we had to get the house turned over. There was a good bit of work that needed to be done for just a year of someone living there. They had also left stuff behind that became our responsibility to get out of the house. We listed the house for rent. Our partner showed it to 3 younger people who would rent it together. They seemed great until we ran their background and credit check. They had evictions they didn’t disclose (claimed they didn’t know), so we shared the report with them and continued showing it.

We ended up showing it to a couple, and they liked it. After we accepted their application, we were able to get the lease signed on May 7, 2020. Since this was at the very beginning of the pandemic, we had to get creative. I signed this lease on a street corner (hadn’t realized that the place I had selected with outdoor seating was closed!), and they paid their first month’s rent, security deposit, and pet fee in cash that he handed to me in a sock (with a warning that told me this wasn’t the first time he handed someone cash like this haha). They’ve been great tenants, and they renewed their lease.

MAINTENANCE

The new carpeting when we first bought the house cost us $700. Between the termite treatments and other general pest control, we’ve spent $950.

Once the first tenant moved in, we learned of some other issues that weren’t apparent by us just working there and not living there. We had the plumber come out to fix several issues with the hot water that cost us $1450! Then we found out that the master bathroom shower wasn’t installed properly, and it was missing a p-trap; that cost us $325.

Our insurance carrier didn’t like that there wasn’t a handrail for the front steps of the property, so in March 2020, we had to have one installed at $190.

We had to replace the washing machine in April 2020 for about $500. As I’ve shared, we try to not include any ‘extra’ appliances because then maintenance and replacement are our responsibility. This was a fun one – we replaced it just to make the tenants happy and not deal with maintaining it, and then those tenants left right after that, and our new tenants brought their own appliances (so they just have two washers and two dryers in their kitchen).

We had an electrical issue with the master bathroom that cost us $150.

Luckily, I did the inspection over the summer, and nothing came of that initially. We did end up replacing a fan in the master bedroom because the light part of it stopped working with the switch. Since we don’t live near the house anymore, and our partner was in the middle of getting married, we went through Home Depot to have it installed, so all together (fan/light and install) it was about $175.

SUMMARY

This has been a good house. We didn’t realize that the house is located outside the city limits, so we needed to figure out trash pick up in the county (not included in the taxes). Other than a few maintenance hiccups, things have been smooth sailing. We’re happy with the tenants who are there, that they’re maintaining and cleaning the house, and we’re getting our desired rent amount (that they pay on time every month). The street is in a decently nice neighborhood with a lot of original owners, which helps it keep (and increase) its value.

This house was purchased in 2018, and it was actually purchased by our Realtor and friend, under the plan that we would formalize the partnership after closing. Mr. ODA had been searching for another investment property, but we had 10 mortgages already (9 investment properties and our personal home), which is a Fannie Mae cap (see the Selling Guide, section B2-2-03). One of our loans was a commercial loan, and we had hoped that it didn’t count against the 10 mortgage limit, but it did. Fannie says that the cap is the number of properties being financed, regardless of type, when looking to originate a new loan. Our Realtor had one rental property on his own and had mentioned how he wanted to purchase more properties to create an income stream through that option.

Mr. ODA and our partner went to see the house without me in March 2018. After the initial visit to see the house, they requested the information for the tenant that was living there. We received their applications, current lease, move in check list, and rent roll. They had started living there October 1, 2015, and while they had been late, they had always eventually paid rent with the late fee. During some of our initial searches, we had someone tell us that rent on the 6th was more profitable because they’re pay with a late fee. While we don’t encourage late payments (and we’re actually really lenient with late fees in general), this eased our tension when we saw late payments.

The house is a 4 bedroom, 2 bath, with a fully finished basement. The condition of the house was probably slightly lower than what I would have accepted based on the pictures, but I hadn’t seen the house in person. I actually had only seen one room of this house before our walkthroughs this past July. Our partner and Mr. ODA said that the pictures didn’t do the house justice, and it was worth purchasing.

After our partner purchased the house in April 2018, we established a Limited Liability Corporation (LLC). My last post goes through the details of why we established an LLC for joint ownership, but we don’t use LLCs for our personally owned properties at this point.

LOAN TERMS

We requested three different options for the mortgage numbers: A) 20 year fixed with 20% down was 5.125%; B) 20 year fixed with 25% down was 4.75%; or C) 30 year fixed with 25% down was 4.875%.

All of the options included ‘points’ without us being told upfront or requesting it. We questioned the reason for the quotes having these points and were given a half-hearted response that sounded sketchy. We ended up with a 30 year fixed, no points, and a rate of 4.875%. There wasn’t an incentive to go with a shorter loan (and therefore a higher payment each month) at a higher rate just to put 20% down. We went for the 30 year instead of the 20 year to increase our cash flow opportunity since we have a partner on the house and are only getting 50% of the income and taxable expenses.

PARTNERSHIP

Our partnership actually started with a loan for the down payment of this house. Mr. ODA and our partner agreed to allow us to pay him back over time for our 50% of the closing costs. We didn’t have the amount needed liquid, but we knew we could make up the amount owed over a short period of time instead of liquidating money from our investment accounts. We were able to pay most of what was needed for his closing, but we “took” a loan from him for $8,000. I used a loan agreement template that I found online and manipulated it for our purposes.

We established the loan terms to be the same as the mortgage he was entering into (4.875%). Most personal loans are for five years, so we chose that timeframe, even though we knew we’d pay it off much earlier than that. We could have just agreed to the terms and not documented it based on our relationship, but I’ve always felt better having things overly documented. I was basically an auditor in my career, and I’ve seen how “gentlemen’s agreements” over rental-related things haven’t worked out. I formalized the process through this contract and had all of us sign it. While the contract was mostly for our partner’s benefit (to make sure we paid him and he received interest), this was the only documentation we had that once he closed on the house, he then had to give us 50% share of the property ownership.

I established a simple amortization schedule through Excel’s templates. We established the loan terms as 5 years (60 months) at 4.875% (same as the mortgage being executed). When I made extra payments to him, I logged them in the spreadsheet. We only made two payments to him, but he made $44 for not having to do anything except accept our money. 🙂

We had to establish an LLC to be able to claim the tax benefits on this house for our 50% share. The attorney required us to have the tenants acknowledge the transfer of ownership to the LLC since we hadn’t executed a new lease in our names. The attorney then took care of the establishment of the LLC with the State and transferring the deed of this house to the LLC.

RENT COLLECTION

We’ve had the same tenants since we purchased the house. We inherited the tenants, who had moved in 2.5 years before we purchased it, and had rent established at $1300.

As a reminder, we purchased the house in April 2018. They paid that July’s rent late, and despite reminders about the late fee, they didn’t pay it. And so began this constant story with them. The main frustration was that they wouldn’t tell us to expect rent to be late, so we kept having to follow up with them. After two months in a row of it being late at the beginning of 2019, Mr. ODA actually explicitly said: In the future, it’s better to communicate issues with rent payment up front to see if there’s an opportunity for us to work with you. We had been lenient and informally requesting the status of rent, but this was their warning that we’d be sending notices of default going forward.

In January 2021, we hit a wall with rent payment. I sent the notice of default on the 6th of the month like usual. However, because of the pandemic, I had to adjust my verbiage to highlight all the rent relief options available and remove the late fee requirement. My understanding is that a late fee can still be collected in Virginia, but I can’t proceed with eviction just because they don’t pay the late fee portion (which isn’t something we’ve ever held any tenant to regardless). While the rent payment is typically due within 5 days from notice, Virginia now required me to give them 14 days to request a payment plan or pay rent owed. We then had to text and email them several times and never got a response. I finally sent an email with the following at the beginning:

We are very flexible landlords and willing to work with all our tenants. However, we are unable to work with anyone who does not preemptively share possible rent payment delays nor respond to requests for information. Please respond to this email by noon Sunday January 24, 2021 or pay the rent owed by that deadline to prevent proceedings for eviction filing with the court.

Virginia was very lenient with rent payment throughout the pandemic, but they were also fair. The lack of response from a tenant or the tenant not working with the landlord didn’t protect them from eviction. I finally got a response that the rent would be paid that week.

Since then, we’ve been told that rent will be late. We’re simply sent an email that says “you’ll receive rent on 2/12. Sorry for the inconvenience.” It’s as if they feel they have the upper hand and control. We hadn’t received any late fees until I finally sent an email in response to their “you’ll receive rent when we get to it” email for August’s rent that there’s a late fee due.

In 3 years, they’ve been late 14 times. When I put it in that perspective, it doesn’t seem that bad. In the moment, it seems like it’s a constant battle with this house. That’s probably because a majority of our houses pay rent without making it a painful process!

RENT INCREASE

We hadn’t raised rent in the 3 years we owned the house, and they had been paying $1300 since they moved in on October 1, 2015. That’s a great deal for them! Depending on our ownership costs, we would typically look at raising rent every 2 years, and likely around $50. We’ve raised the rent on only 2 tenant-occupied houses we have (meaning, raised the rent on people who continued living there, versus raising it between tenants); both were rented under market value when we inherited the house, and both have received a $50 increase every two years. We typically raise the rent during vacancy times, which has worked out pretty well for most of our other properties.

For a 4 bedroom and 2 bath house, $1300 is low. We mulled over our options. The house is currently on an October 1st renewal, which is a poor time to be looking for new tenants. I wanted to get the house on a spring lease moving forward. My original proposal to our partner and Mr. ODA was to offer them a 6 month lease (ending 3/31/22) at $1400. Our partner said we should include our expectation that we’ll be raising the rent to $1500 for a year long renewal as of 4/1/22. I struggled for weeks on the verbiage for this double proposal. Eventually, Mr. ODA said we should just risk it. We should lay out an 18 month lease at $1450 to split the difference, and if they don’t want it, they can leave or attempt to negotiate.

We offered them just that, and they accepted. Of course, true to form, they were a week late in meeting the deadline to sign the selection that they want to continue living there at the increased amount. Now the rent will be $1450 as of October 1, 2021, and their lease will run through March 31, 2023.

MAINTENANCE

We started with a clogged drain right off the bat. We had our partner go over there and try to unclog it with store-bought items, but it didn’t work. We ended up hiring a plumber for $300 to work on it. We’ve had several plumbing issues in this house, including a clogged sink that backed up and flooded the kitchen and basement. We ended up needing to have the line jet blasted and a camera put through it for $550! This plumber’s quote for the ‘fix’ was $6k. Mr. ODA sent the video footage to another plumber, and that guy said he didn’t see that anything was needed, so we didn’t proceed with the ‘fix.’ The jet blasting appears to have worked, and we haven’t had any damage reported. The other plumbing issues included fixing leaks in the basement bathroom and replacing that toilet.

The inspection didn’t identify active leaking on the roof, but our insurance company was hounding us over the condition of it. We ended up sending our roofer out there to do the items that came up on the inspection report. This was $350.

We then had several more issues with the roof that cost us $125 before we just decided to replace it. The replacement was quoted at $5,500 and surprisingly that’s what we paid. We expected to have additional costs for plywood replacement due to all the damage we had seen.

Interestingly, while not communicating about rent nor paying rent, they felt the need to tell us the washing machine wasn’t working. We ended up replacing the washing machine for them. We try to not supply any non-required appliances because then it’s on us to fix them or replace them, but since the tenants already lived there when we bought the house, we inherited that the washer and dryer are our responsibility. More interestingly, as I was writing this post and going through my receipts, it dawned on me that the washing machine that was in the house when I did my walkthrough last month isn’t the one that we just sent them in February.

While collecting rent has been frustrating with this house, and we’ve had a lot of plumbing and roof expenses, the house is still profitable and worth our investment. The house is in an area of Richmond that’s being revitalized, yet at the same time it’s in its own pocket of the city that’s also protected from big changes and is mostly original owners. Appreciation has really taken off, so even though our maintenance issues have eaten big chunks out of our cash flow, this house will be well worth it when we eventually sell it and move on to a new investment.

This little house has been made home by two families. It’s a 2 bedroom, 1 bath that is 719 square feet. While there have been a few issues with the house, it’s been pretty easy to manage because of the tenants taking great care of it.

I feel like the bathroom’s blue tile, patterned floor, and that peek at the door knob exemplifies the age of the house.