Well, we started the month with way too many things hitting the credit card: 2 insurance policy renewals, a new insurance policy, air conditioning fix at a rental, and bathroom replacement at a rental. That eventually led to a $1500 charge for bat removal at another rental.

PERSONAL

My big news this month was handling my HOA’s annual meeting. We’ve been working so hard for the last year, and I tried really hard this year to increase communication between the Board and community. I think I did a good job because there wasn’t any contentious point of this meeting and there were very little questions. I received nice feedback on how I presented the budget and that I did a good job throughout the year. It was a welcomed win since there was a lot of heat in the previous couple of years.

The family’s big news is getting passports for a trip this Fall. The parents already have theirs, but we got the kids their pictures and submitted their application. So our credit card balance is higher than normal because we paid for flights and the cruise itself.

It took us until the last week of June to meet our deductible on our health insurance. It’s only $3,300, so that’s quite the impressive feat. I’d point out that my March surgery took until then to get processed correctly, but at least we eventually got there. I have very little faith that it’s all processed correctly though, so it’s on my to do list to verify that we’re not overpaying into that deductible, which they don’t make easy because they don’t show me prescription fills clearly.

We went on a trip for a long weekend to visit Mr. ODA’s aunt in WV. They have a vacation house there, so we didn’t pay for lodging. Unexpectedly, they provided all our meals. I bought them a gift card and some beer. So between that gift, gas, and the meals on either end of the trip, we spent about $200 for a trip, and it was one of the best vacations I’ve been on.

Two of the kids spent this past week at camps. One was 3 hours per day at a dance studio, and the other was 9.5 hours of all outdoor time for the week. He had a blast, and I’m kind of jealous that he got to play all those games and have a great week.

RENTALS

This month, I received an email from Rent App that a tenant was paying their rent. She didn’t give me a heads up, so I wanted to verify things with her. She said this app pays me in full, but it takes the first half of the payment from her account at the beginning of the month and then the second half of the payment in the middle of the month. They’ve lived with me for for 8 years, so I’m surprised she sought out this option instead of talking to me about a payment plan. The program was extremely sketchy and I didn’t feel good about a single step of it. I gave up the registration process at the point that it required untethered access to my phone, but I wish I would have followed my gut at the first personal information step, as if it wasn’t bad enough I had to give my bank account details for the transfer to happen. The payment eventually came through on the 10th, but I didn’t feel good about it.

Another tenant paid late with the late payment. And another tenant paid late with little to no communication and several follow up conversations. I can’t stand when I have to hunt down money. I’m willing to work with everyone who reaches out. She paid the first one with a (1/3), so clearly she knew the plan. And yet, on the 6th, I had to ask where the rest of the rent was. She said it would be done that day. A partial payment was made on the 7th. Then another partial payment on the 8th to finish it out.

We hired someone to clean out the gutters at two houses. Both houses are inundated with trees over the roof, so it’s something we need to stay on top of because they back up every 6 months. We could add gutter guards, but just didn’t see the point since we could do it. Now we don’t live there. He is also going to cut trees 10′ back from the roof on one of those houses.

And then the bats. One house had a bat show up last Monday. My property manager didn’t think much of it, so we didn’t do anything (I wasn’t even told about it at that point). Another bat showed up on Saturday. The tenant went for rabies shots and got boosters for her dogs. She then took a bat to get tested, which came back negative. She said she wasn’t comfortable staying there, so she stayed with a friend. We had traps set so bats could get out of the attic, but they couldn’t get back in. The pest people will go back next week to check on things.

We have two houses that will be vacant at the end of this month. We were supposed to have one at the end of June and one at the end of July, but the June one asked for an extension. I let them have it, but I’m not thrilled about my timing now. We won’t be able to truly get to work in there until mid-August, and it’s going to require a lot of work (not hard work, just time consuming). Then for the other one vacating at the end of the month, we don’t intend on renting it again. We’re going to let it sit over the winter and sell it in the spring.

NET WORTH

The way that I update our net worth each month involves overwriting the numbers from last year. So I can easily see that we’ve gained over half a million net worth since July 2024’s update. What’s nice about that is that it’s all appreciation, paying down mortgages, and the stock market with continued savings. We didn’t make any large financial moves that would have adjusted our net worth in one large move like buying a house. I had a conversation with someone about our net worth and goals recently. It would be nice to cross the $5 million threshold, but we’re not actively managing our funds in a way that will cause drastic swings outside of market movement. We crossed $4 million in March 2024.

We’re over $200k from last month’s update. Our credit cards are much higher than last month because of trip purchases and rental work that was unexpected, but needed. Here’s to the last month of summer.

*I’ve been working on this post for a week, so my numbers are a week old, but I don’t want to re-update them. I’m also posting on a Tuesday just to get this ‘out the door.’*

I’m starting to pull myself out of the overwhelmed hole I felt I was in. There’s still a lot going on, but I feel better equipped to stay on top of things. I had just been so exhausted, that I didn’t have the energy to do anything extra each day, and I was just getting by. Last weekend, I was able to work on pressure washing our patio and deck furniture (which was long overdue), and then I stained our deck. That’s been a pretty good springboard to me getting a fire lit under myself to get other things done, so that’s felt really good.

Our middle child graduated pre-k on Thursday. That was a big milestone, and my poor girl is so sad that she’s going to miss her teachers. She’s really struggled with my going to work and not being home all the time (although my time not home, while she would be home, averaged about 10 hours per week). I have things better organized at work, and I’m feeling good about my tasks and role in the office, so the hours I’m spending there are dwindling. I had agreed to about 20 hours per week, but I was closer to 26/28 each week. The biggest issue was waiting for someone to be available to help me, and then that everyone else is full time, so they don’t realize I’m trying to get out of here by 2 pm each day. This week our oldest graduates kindergarten and has many events around end of school.

RENTALS

One of the mortgages has been paid enough that the balance dropped from 6 digits to 5 digits. It’s still a lot of money owed there, but that felt like a nice accomplishment when I went in to capture the balance!

June is Richmond tax season for these houses. That means I’ll be paying out large chunks of money for the houses we have no escrow on.

We had a few maintenance needs come up. One house had the water heater flood the basement. Luckily, I think we’re OK on that front. We replaced the water heater. The gas wasn’t hooked up right, so the tenant called the plumber to get that squared away. This happened while I was in a different state, and I’m so grateful it happened in a house with a handy tenant.

We had some flashing fall off a roof line. This wasn’t a priority to address at the time, but the tenant started claiming allergies were flaring up because birds were getting in the attic. Sometimes you just need to accept that’s the story you’re hearing. We had a handyman go over there and verify there are no birds anywhere. The “hole” she thought she saw was just where the soffit was hanging a bit, but there were no gaps in the wood structure itself. He tacked up the soffit, and I contracted with another company to repair the one piece of flashing.

That handyman also went out and handled a wasp nest. At that house, the tenant says a window won’t stay open when she opens it, and we let her know it’s on our radar now, but it won’t be fixed just yet as our people are spread thin and that’s not an emergency. That house had a temporary tenant in it (housing with our current tenant). To cover the tenant and us, I asked for a $500 deposit. When they moved out, I had our tenant sign that there was no damage, and I returned the deposit.

We’re still working on the major termite damage that occurred at another house. There was quite the domino effect. Leaks from bathrooms and the laundry room created a very wet environment, which created a breeding ground for termites, which feasted on our wood all over that place. The crawl space got cleaned up, but we’ve been waiting over a month for the bathrooms to get replaced and fixed. I’m hopeful that it’ll start next week, but frustrated nonetheless.

I had a leak from a toilet bolt at another house. I was frustrated because we had just been called out for water on the floor at this house recently, but it turns out this was necessary. When the house is a certain age, things just wear away and need replaced.

We also had a limb fall from a tree at another rental. The tenant explained how much of a liability it was for me. I love when tenants instruct me on my level of liability (that’s sarcasm). We have a tree guy that’s been super useful for many things and he handled it the next day with no problem.

PERSONAL

We haven’t been spending much money. Most of our money these days goes to grocery shopping. On our current statement for our main credit card, we only have 11 transactions recorded for over 3 weeks.

We paid our last month of pre-school for our second. They are closing the school and they didn’t want to add on days for the snow days that occurred, so they gave us $50 off the last month of tuition to cover the 2 days we were owed for make-ups. Since the school is closing, everyone scattered, and we ended up not getting into another preschool next year for our youngest. So at this point, that’s an extra $375 per month in our pockets next year – unless a spot opens up for the littlest.

Mr. ODA took the buy out, which I think I mentioned last month. His last day of work was April 30th. He said he’s settling into the not working concept and starting to get over the desire to know what’s happening at work and with his programs he worked so hard on. He’s done a lot of work around the house here, including treating for termites in a very intense fashion, but that was cool to see.

NET WORTH

Two months ago, my job asked for my goals. It’s a specific document that I was to fill out. Someone else had mentioned their net worth goal, and our next big step would be $5 million net worth. Well, the market has been in shambles, and our net worth plummeted from where it was. I thought it prudent to not make such a goal when our net worth is completely reliant on the market actions right now (i.e., we’re not selling/purchasing or making any big moves that would drastically change our net worth outside of the market actions). We’re finally on the upswing and now at the highest net worth we’ve been, so that’s encouraging after those big dips recently.

Well, my desire to post every Thursday fell off there. I started a new job, Mr. ODA’s Federal job has been in limbo, and just general life things have been going on and keeping us busy. The kids started t-ball in the past few weeks, our youngest was waitlisted at both of the preschools we tried for, and the rentals have needed more attention than average. Let’s dive in.

NEW JOB

I was approached by someone I serve with on our HOA board. They were looking for a new person who has a financial background, was really organized, and could handle talking to people regularly. It appears that I made such an impression on him and his wife. I wasn’t ready to get back into the workforce. While I have enjoyed my temporary jobs I’ve done since I quit my career in May 2019, I always had a ‘sunset date’ on those activities. I knew that each job was only for a short period of time, and I’d get back to freedom/flexibility. This was a new territory they were asking of me – be on a set schedule and away from my kids.

I expressed that my need for entering back into the workforce was that I wanted to be part of my kid’s activities and I needed to work between school hours for the most part. They expressed a desire for me to work 30 hours, and that just wasn’t feasible. Based on what they told me about the tasks required of the job, I was able to come up with about 18 hours of work, knowing it would likely become 20 hours. So far, I’ve worked more than 20 hours each week as I’m learning, and things are not moving as quickly as I expected them to. I’m 2.5 weeks in, and at this point I can do all the main tasks. Where I’m struggling is the knowledge of all the “one off” transactions and how some people are treated a little differently than the standard.

Overall, I’ve been super grateful that Mr. ODA has given me the space I needed to get my feet under me these past couple of weeks, and I’m really enjoying learning these new tasks and being involved in this sector.

FEDERAL WORKERS

It’s been rough around here for almost two months now. While Mr. ODA is still employed, there is a daily concern that the news will come in. There’s no security like there used to be expected for a government position. The blows have become a bit more scattered than it being such a daily barrage, but there’s still uncertainty and daily updates and waiting for more information that’s occurring.

PRESCHOOL

Both old kids will be in regular school next year. Our youngest has a late-in-the-year birthday, so he wasn’t eligible for preschool until this coming school year even though he’s already 2. The preschool where both of the other two went to shut down. My middle is finishing out the year there, but next year, they sold the preschool concept off to a third party. The company that took over has terrible reviews, and everything about them screams ‘daycare.’ While people need daycares, and that’s fine, we don’t need that. I wanted a space that had a curriculum.

The school previously had a daily agenda and an expectation that the kids were there from 9 to 12. This new school has a come and go as you please set up, and they couldn’t provide me a break down of their daily schedule. The admissions person was actually quite rude and condescending to me, after taking 4 days to return my phone call. I’m not in a desperate need for our youngest to go anywhere, so I won’t be trying to enroll him there.

We had hoped to get into another preschool by our house, but the closure of our old school sent a mass exodus to the nearby preschools. I told Mr. ODA that I wanted to join their church so I could get 3 weeks ahead on signing up, but he said that wasn’t ethical and was more than just saying “I want to join your church.” So I didn’t. But several other families did. And they got in. And I’m still really sad about that. He’s waitlisted there, and there’s been no indication of hope that he’ll get off the waitlist.

I tried for a “moms day out” program, which would cover one or two days per week (I was looking for 2 days previously). He’s waitlisted there, but she gave me a glimmer of hope that even though they don’t have a lot of turnover, there is a chance a space opens up either right at the end of this school year or at the beginning of next school year.

I had originally ‘mourned’ the loss of my freedom with the preschool closing down. I have been at my kids’ beck and call for 7 years by the time our youngest would go to school. Even though it was only going to be 6 hours per week, I was excited to get things done that have been on my to do list for years and just run errands unencumbered. I’ve lessened my extreme feeling on that over time, but it still would be nice to have a few hours dedicated to me and my schedule at some point.

RENTALS: RENT RATE

I evaluated our current tenants and their rent rate back in December. I should have just written the letters at that point and been prepared for the deadlines, but I didn’t. So this week, I got those rent change letters prepared, printed, and mailed. We typically change the rent by $50 every two years for our long term tenants. That’s the approach we took here except for a couple that needed more catch up. One tenant has already responded and executed a change to increase their rent. I have 4 more out there waiting for the tenant to tell me they accept the adjustment or will be leaving at the end of their lease. I also have another tenant who will be staying another year, but I didn’t change their rate since I had changed it by $25 last year.

RENTALS: TERMITES

We have a house that we purchased with termite issues. We knew it going in. We had it treated, and then we fixed the really bad areas. We then didn’t get notification about an annual warranty payment they would do, so our coverage lapsed for a few years. We saw swarmer termites in one part of the house and called them back. They offered to let us backpay those missed warranty years, saving us about half the cost it would have been for a new treatment. Well, we’re paying for that now. For the last 4 years, they’ve checked the property once per year. They’ve noted termites actively being there with more damage, and they didn’t clearly communicate the concern of the condition until this month. We have major problems in the house. One wall in the laundry room is so bad that the termites ate the backing off the drywall and the drywall is all cracking off the wall because it’s not being held onto anything. It really hasn’t been fun, but I know we will be able to fix it. So far, we’ve had the crawl space cleaned out and relined with a vapor barrier, and some plumbing issues fixed that were creating a perfect moist condition for termites to gravitate to. We still have to rip up the carpet, fix the subfloor, lay LVP, rip out a shower insert, reinstall the insert, and get the shower operational after that. It’s a lot.

PERSONAL FINANCES

Mr. ODA reduced our monthly contributions to our investments. We were putting $3,000 per month in (3 separate $1,000 transactions), and now those have been reduced to $500 three-times per month. The kids still get $100 per month each into their UTMAs.

We’ve been so busy that we have hardly spent any money. Outside of insurance and medical payments, the only extra spending I’ve done is for our daughter’s birthday parties we’re having this month. I’ve bought some clothes since I’ve lost weight on my post-three-kids journey too. Usually, we’ve booked a trip by now, but we haven’t done that either. Overall our spending is lower than it has been.

NET WORTH

The market is well below where it has been, and all our numbers show it. We are over $189k lower than last month. I haven’t updated our property values yet. I’ll probably do that next month as the spring market ramps up.

We’ve hit some pretty big milestones financially. Mr. ODA casually mentioned a certain number by a certain age, but our goals were more associated with quitting our full time jobs. I quit my job in May 2019. We’re in a situation for a couple of years where we’ve been ready for Mr. ODA to quit, but we keep pushing the date back because his job isn’t preventing us from doing the things we want to do.

How did we get to the point where we replaced my income and I could quit working without scaling back anything financially? We took risks. Some of them were big ones. Some of them weren’t so big, but they felt big at the time. Most risks worked in our favor, but some did not.

RETIREMENT ACCOUNT LOAN

Mr. ODA and I both worked for the Federal government. Their version of a ‘401k’ is the Thrift Savings Plan (TSP). There were two loan options that were available: a primary residence loan or a general purpose loan. You then repay the loan back to your account with interest (the interest is paid into your account as well). When we took our loans, the rate was just over 2%. According to tsp.gov, the rate is currently 4.75%. There’s a fee of $50 to take a primary residence loan and a fee of $100 to take a general purpose loan.

While you’re missing out on the compound interest of your account when you take the loan, the ability to buy our own house, create that equity, and be at the beginning of our careers made the decision easy for us. We made extra payments during the repayment period, and we were able to adjust the regular payments up and down based on our financial needs each month. We have no regrets in our decision.

ADJUSTABLE RATE MORTGAGE

An adjustable rate mortgage (ARM) sounds scary. A variable rate. Most people are used to locking in a 30-year mortgage. I’d venture to say that most people also think they know what an ARM entails, so they don’t even consider it. We considered it. We looked into it in great detail. We couldn’t see why more people didn’t use it. We actually were very hesitant over this decision the first time because an ARM’s reputation is very negative. However, we took our time to lay out the numbers and see what would work best for us.

The first time we used an ARM, we knew we had no intention of being in the DC area for more than 5 years. By using an ARM, we saved thousands worth of interest in our mortgage payments over the three years we owned it.

There are several “fail safe” parameters in an ARM. For one, you do lock in a rate for some period of time. We considered 5 year, 7 year, and 15 year options. Then after that period of time, your rate can only adjust within the contractual terms. For example, we have one rate that can adjust 2% in either direction at the 5 year mark, and then 1% for each of the following 4 years after that, with a cap of paying a maximum interest rate of 7% (this is an old loan, clearly). The rate adjustments aren’t a given, and they’re adjusted based on the prime rate at that time, not based on the whim of the bank or the maximum it could increase.

We also ran the numbers based on the interest rates. An ARM’s incentive was that the interest rate is lower than the 30-year conventional loan rate. I don’t have the details since this post is more of an overview, but the ARM saved us money we paid towards interest. Interest is a higher percentage of those earlier payments in an amortization schedule. We either sold the house or paid the loan off early, so the ARM adjustment never came into play, and we saved all that interest cost.

BUSINESS/COMMERCIAL LOAN

A series of events had us asking a local credit union about loan options. They offered us a commercial loan. This one has a big catch though: there’s a balloon payment. Our loan is amortized over 30 years, which is how our payments are calculated. However, the balance of the loan is due at the 5 year mark. That balance is going to be about $175k. We have no plans to pay that off by that time (we aren’t even making extra payments towards it). We will refinance it. The pro here was that our interest rate for a loan closed on in 2022 was 3.625% (when mortgage rates were in the 5% range). Hopefully by 2027, interest rates are lower than they are today; this is a gamble at the moment.

PARTNER

There’s a cap in the “Fannie/Freddie” world of the number of mortgages a person can hold. That cap is 10. There was a point where we had completely leveraged ourselves and ran out of room. We had a Realtor friend interested in more rental properties, and he agreed to front our down payments, which we’d pay back with interest, and have a 50% share in the houses.

We signed an agreement with him that outlined our payments to him for the down payment he covered (which we paid off in about 3 months), and it established our 50% shares in the two houses purchased via this method. We purchased the houses in April 2018 and February 2019, and put them in a limited liability corporation (LLC). Each month, I collect rent from the houses and pay out our partner’s share. These houses don’t ask for much (one has been rented since before we owned the house and one has a tenant that has been there a few years), but if they need something, I handle coordinating the maintenance request. We should have set up a schedule where I’m paid for my time since Mr. ODA and our partner really don’t do anything for these houses, but luckily the requests are few and far between. We split all costs 50/50.

RENTERS WITH COMPENSATING FACTORS

I have several examples of entering into lease agreements with tenants that don’t have a perfect record. In these instances, we typically request some sort of compensating factor (e.g., a cosigner, an additional security deposit). We give everyone the chance to tell us about their financial and rental history before we run a background check on them (telling us doesn’t cost anything, but a background check does).

We had a prospective tenant not disclose a bankruptcy on her record. I could have immediately disqualified her and her husband, but I gave them a chance. They lived in that house for a year. They only moved because his job after grad school took them out of the area, but they set us up with a new tenant at their departure, and she stayed there for several years. Then they moved back to the area, and they requested a house of ours. We had one available, so we happily had them move into it. There’s one success story from giving someone a second chance.

I also have a couple that doesn’t have a happy ending. We had purchased a house without vetting the area. I had fully vetted a house two blocks away, but I learned my lesson that the crime of an area doesn’t need more than one block to change its ways. This house was in a bad area. The house itself was adorable. It attracted wonderful people to come see it, but they’d check the crime history of the area and decline applying (understandably). Someone came forward with a 448 credit score. That’s pretty bad. She wrote a really nice letter though. She disclosed everything up front and said she just wanted a roof over her and her son’s heads. I believed it. We then spent months and months struggling to get her to pay her rent, even offering her a payment plan several times and changing her lease structure to allow her to pay twice per month (hopefully eliminating the constant late fees she was accruing). We eventually gave her 30 days notice to vacate the premises due to lack of payment. She didn’t even make it a year. Instead of listing the property for rent, we ended up selling it. That was a whole other debacle where we entered into a contract to close by September of that year, but we didn’t close until the following January due to the lack of financial qualifications on the buyer’s end.

PAID OFF LOANS/MORTGAGES

This doesn’t appear to be a big risk. What could go wrong with paying off your mortgages? Well, if we didn’t have a cash reserve, and there was an emergency, then we paid off these loans with the cash on hand, leaving nothing to cover that emergency. However, those dooms-day concerns rarely come to life, and we had continued cash flow that replenished our accounts.

The positive here is that we freed up cash flow. Instead of having mortgage payments to make every month, we now have the cash to go into savings or towards any higher-than-expected bills. Besides the house we sold, we’ve also paid off 6 mortgages. That means that we’ve paid less interest to the banks, and that’s more money in our pockets.

We haven’t paid off any other loans because they’re all below 5% interest (they’re actually all below 4% except for 1 with our partner, and we would need his buy in the pay that off, which he hasn’t wanted to do). After payments to mortgages, our property manager, our partner, and utility payments, we have over $8,000 in cash flow per month. I will note that this doesn’t include things that I need to save up for each year to be able to afford (e.g., taxes and insurance), and it doesn’t include maintenance needs that crop up. Cash flow is important for us because if Mr. ODA quits his job, that’s less income to offset our regular personal expenses.

FINANCIAL AWARENESS

On any given day, we’re weighing several financial decisions fluidly. There are the givens that we have to pay the bills that are out there. I have to pay all the mortgages and utility bills. I weigh the best time of the month to pay each bill, which means that I may not pay them as soon as the statement arrives, but may wait until closer to the statement due date (but never carrying a balance unless it’s 0% interest). Then there are the options such as paying additional payments towards a credit card with a 0% interest rate, additional principal payments to a mortgage, or additional investment plans. We’re not looking to apply for any loans, so the $9k balance on a 0% interest credit card doesn’t have any attention of mine except the $500 I pay each month. I have it marked on my calendar when that 0% introductory rate expires, and I’ll have to pay the balance in full.

Our money is handled by a full, big picture, approach. Each day, there’s a chance that we come to a fork in the road and make a different decision because the variables changed slightly. We don’t put our money into “buckets” or “envelopes.” In my experience, people who handle their money like this end up overspending.

We hit our goal to replace my income well before our son was born, but then I kept working until he was 9 months old. While I was still working, we could have easily said, “we hit our goal, but since you’re still working, let’s put all that money into a slush fund of some kind.” When people see any “extra” money, they then look for their next splurge. They feel they deserve something for saving money instead of putting that extra money to work for you and your future.

There are those “autopilot” moments in our finances, but when it comes to making a big change, we put pen to paper and check the details. We aren’t going to take $100,000 out of our investment accounts to pay off a 2.5% mortgage. But one day, we will have to consider what to do with our loan that has a balloon payment, which shows it’s not a hard and fast rule that we won’t pay off anymore loans early (because if interest rates are still at 7.5% in 2027, it may not be worth refinancing that balance).

LIVE SMART WITH INFORMED DECISIONS

Take the time to make informed decisions and research the data for yourself. Run models with the projection of money to see for yourself if it works in your situation. Don’t spend your days listening to other people’s opinions on actions. If we had listened to opinions, we wouldn’t have taken a TSP loan or taken out ARMs.

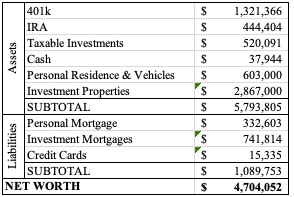

We’re at over $4 million net worth, have a solid cash flow (which is important because if our net worth of $4 million was tied up in a retirement account, that wouldn’t give us the ability to live comfortably now), and have plenty of money going into accounts for the future (for both us and the kids). Our spending is managed regularly with an ingrained thought process. Take the small, first step for yourself without other people’s opinions weighing you down.

If you want to live differently from everyone else, you have to take action and think for yourself.

We’re just going to cut to the chase – $4 million net worth! I mentioned that this was a goal for this year. Unlike other years worth of large jumps because of purchasing houses, this was less in our control (granted, our market allocation decisions are what’s driving it…. and by “our,” I absolutely mean only Mr. ODA’s because I don’t do anything in that realm).

RENTALS

Well, we’ve had a quiet month. What’s going to be funny is, I’m going to list the things that we did. Quiet doesn’t mean silent or without effort, but we’ve had a rough go of it over the last year, so this was a welcomed break.

We had termites at a property. We pay $98 annually for their termite warranty program, since we found extensive termite damage and live termites when we bought the house. We’ve had to treat the house several times, so this $98 is a steal. However, I’m wondering why we keep needing to treat the house.

We paid $125 for a plumber to go out to a clogged sink. When we received the invoice, it was for 2 plumbers to go. Between the phone call that they were on their way and the tenant saying they were great, only 35 minutes had elapsed. The company charged us almost $300. Mr. ODA called to ask why they choose to send two plumbers to do a one-man job, while also charging us for it. The owner said it was for liability purposes, which Mr. ODA fought back on. They agreed to a reduced rate, but we were only charged $125, which was less than agreed upon.

We had our third tenant move in, after we unexpectedly had to turnover three houses in the middle of winter. We also were given notice by another tenant that she’s vacating by the end of March. We handled increases for two houses (one handled by a property manager to increase $50/month, and one handled by me to increase by $25/month).

We had one tenant pay on the morning of the 6th with no communication, so I did have our property manager let them know that’s not going to be ok. We also had a usual suspect pay late, with the late fee. However, their communication was frustrating. They said they’d pay on the 6th. At the end of the 6th, they said the money hadn’t cleared like they expected. No communication on the 7th. I asked for an updated on the morning of the 8th, and they said it would be that day. At 11 pm, I hadn’t received anything and reached out. I was then told that money was going into the ATM right then so that she could pay. Sometimes I wish I could do a deep dive into tenant finances so that I could help them out.

PERSONAL

Mr. ODA has a trip in July where a group of guys will hike in the Rockies. Our family is going out before that trip is scheduled to do our own exploring. We booked 4 round trip plane tickets, and Mr. ODA handled the lodging booking for the guys’ portion. That’s almost $3,000 worth of purchases, so our credit cards are higher than usual.

Speaking of the plane tickets. We purchased gift cards from Costco for Southwest. The gift cards are essentially $450 for $500 worth of purchasing power at Southwest. We bought two, therefore saving $100 on the tickets. For an extra few clicks on the computer, and the 15 minutes waiting time before the e-gift cards were delivered to my email, that’s $100 that can be used somewhere else.

We bought a new vanity for our bathroom. That was about $700 for the vanity, faucet, toilet flusher, and mirror. I sold the old vanity (in rough shape) for $30. And because I’m proud that I did most of it on my own, here’s a picture. I needed Mr. ODA’s help with the supply lines because I lost patience with how tightly they were screwed on and my lack of progress. I cut the baseboards down to size, except I somehow measured wrong on one quarter round cut (I was cutting while it was on the wall). Mr. ODA cut and installed the replacement piece for me.

We finished up the ski season. The kids did great. I was really proud of them for sticking with it. We used our season pass well (i.e., exceeding the cost had we bought individual tickets for each visit). I took two of the three kids to the aquarium, and we took the baby for a procedure at a local children’s hospital. We’ve started tee ball for our oldest. Our March is very full and busy, so we’re getting into the swing of things and keeping track of the schedule.

NET WORTH

Well, we far exceeded that $4 million goal. The market went up big, with our biggest changes being in our retirement account, IRAs, and cash. Our cash increase is offset by the lower amount in our Treasury account. Some of the short term bonds were transferred back into our savings account, and we’ve kept that money in savings since our deck replacement is slated to begin.

Life is different these days. Our 3rd child was born on Thanksgiving, and we’ve been finishing up some projects around the house. We’ve had a few things happen with rentals, and, basically, I’m just tapped out to keep up with blogging. Mr. ODA asked me what our net worth is at these days, and so I’m updating our spreadsheet.

“JANUARY”

It’s January, so that means I have to create my two main Excel workbooks for the year: the paycheck to paycheck monitoring of our expected income and expenses, and the management of each rental property. The paycheck to paycheck spreadsheet is where I have a line item for each house’s rental income each month, each house’s mortgage payment (where applicable), and then all our bills owed (credit cards, utilities, investments). I break this down by paycheck because that’s the easiest way for me to make sure I have enough income to offset the bills owed during that two-week period. That worksheet in that workbook feeds my net worth calculations, where I also update loan balances. There is actually several tabs in this workbook, but those are the main two. I finally got that all set up today. I haven’t even started creating the investment property workbook.

January also means I have to go through last year’s investment property workbook to verify all the expenses listed are supported by receipts, that all receipts I have are recorded, and that my income is accurate. Then I read off the data to Mr. ODA, who enters it into an online tax portal to file our taxes. I haven’t started that daunting task either.

RENTALS

We had one of our properties flooded by a burst pipe. That’s a mess and is hardly making progress because the tenant’s renters insurance can’t get the tenant property out of the house. We had an electrical issue with a hot water heater in another property. That got fixed, but now I am in a position where I have to fight Home Depot about their shoddy installation a year ago and have them reimburse the cost of rewiring. I finally moved forward with the judgement against a tenant for destruction of property, and our attorney established that collections account.

Surprisingly, we didn’t have any issues with rent payments in December or January. Usually I hear from one or two houses that they need a couple of weeks to pay all of rent. While not everyone was on time, they communicated well and were only a few days late. One tenant reached out and asked if they could pay rent on the 6th (since that’s Friday, and pay day); I told them not to worry about the late fee and that would be fine. Little gestures like that can make a big difference for your tenant’s life.

I sent a letter to our property manager for the KY houses that we’re releasing them at the end of this month, so that’s a new development that is taking my time as well. You’d think my property management company would have a way to communicate this change with the tenants, but alas, that would be too logical. Wish me luck while I add 3 more houses under my own purview. While we moved to KY two years ago, it was easier to maintain status quo with having a property manager. Unfortunately, it has taken too much of my effort to manage the property manager and to fight for our money.

PERSONAL

We finished our master bathroom in the home we bought over the summer (and the room we gutted immediately… only took 6 months to get us to the finish line… and by finish line, there’s still paint touch ups to be had). We bought all the supplies to gut and renovate the basement bathroom in this house. Mr. ODA built a bench for our kitchen table so that we have more seating easier. We made the plans to get the mudroom bench and shelves in, and hopefully those supplies will be bought this weekend.

Truthfully, while I updated most of my net worth spreadsheet in December, I never posted it because I don’t even know where all our money is. When we sold our personal residence at the beginning of November, we were handed a large check. In the past, that check type mostly went towards a downpayment on a new house, but that wasn’t the case this time. Mr. ODA immediately started investing that money in short term treasury accounts that I can’t even begin to explain. Between that account, another savings type account, and our regular investment account, I can update what I see online, but I don’t know what I may be missing. I’m hoping Mr. ODA will chime in soon to describe the type of investment decisions he’s made.

NET WORTH

Several property value assessments declined over the last couple of months. So while our investments are on the upswing from November’s update, those updates to property values have caused a decrease to our net worth.

Back in May, I was a guest on Maggie Germano’s Podcast, “The Money Circle.” I shared some of our background and how we started investing in real estate. We brushed on topics like establishing an LLC, tax advantages, and how you don’t need to start big to just get started. It was a brand new experience for me, but I’m passionate about our real estate experiences, and I loved being able to share. I hope you’ll check it out!

Spring is a time for lease renewals or preparing to re-rent a house.

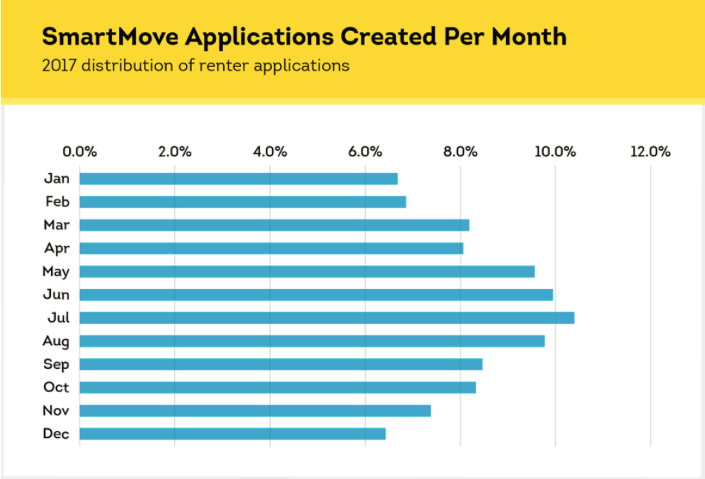

Spring and Summer are times when people are most active in the real estate market. It’s the best time to be listing your house for sale and for rent, which may yield you a better sale/rent amount because of greater competition. This timeframe is likely most active because of the better weather for moving and the school year – if a family is looking to move, they’re more likely to do it when they don’t have to transfer their kids to a different school district mid-school-year. Personally, when I was in college, nearly all the rentals were available in May or June. I remember being frustrated that I couldn’t get an August lease and had to pay for the summer months even though I’d be back living at my parents’ house. Now that I’m older and have more experience, it all makes sense. Below, you can see the increase in applications processed by SmartMove (the way we process tenant applications) that occur during the summer months, which indicates the most active time in the market.

We have seen this reflected in our days-on-the-market and rent prices. When we can list a house in the Spring months, we’re able to get it rented with very few days vacant. Houses that we’ve closed on at the end of the Summer (when school starts) and in the Fall have taken us more time to find a tenant, and we’ve had to reduce our asking monthly rent amount.

For those houses that we had purchased in a less-opportune time of year, we’ve worked to get them back to a Spring-time market for renewal.

We purchased two in September 2019 that we weren’t able to get rented until November 1st that year; we offered those tenants an 18 month lease so that their lease expiration would become May 31st.

We did similar with a house that we purchased in August. After that first year, a prospective tenant tried negotiating the list price for rent, and we said we were willing to reduce the rent a bit for an 18 month lease; they agreed, and we got our rental on a Spring renewal.

We recently had a tenant break their lease (with our concurrence), so that house has a lease expiration of October 31st now. We intend to offer a 6 month lease term to that tenant when the time comes.

With that said, we have lots of activity at this time of year.

We have 9 houses in Virginia and 3 in Kentucky. These markets are so different for us. We do our best to work with our tenants to encourage them to continue renting with us. I wrote about this in detail in my Tenant Satisfaction post.

Here’s a break down of how we handled all the leases that are expiring at this time of year.

In Kentucky, one lease was set to expire at the end of April and another at the end of May. These two properties are under a property manager. She attempted to increase the rent for a new lease term, but the tenants pushed back. Landlords don’t have a lot of leverage in a pandemic. Since the property manager is the one who handled the communication, I don’ t know what the details were. We believe both these houses are rented for less than market value, so that’s unfortunate. But, we’re grateful that both tenants renewed their lease for a year, so we don’t have to work to turnover the houses. Within reason, we’d always rather rent for a few bucks under market value than to handle turnover and lost rent (vacancy) by trying to maximize monthly cash flow.

In Virginia, we have an array of situations. Richmond was quick to acknowledge the property value increases that have occurred over the last year or so. This means that they increased our assessments, which effectively increases our property taxes.

We have the first two properties that we bought in that market, which are next door to each other and both have long term tenants (one since we before we purchased it, and the other is the second tenant who moved in a year after we purchased). We inherited their rent at $1,050, and then we increased it to $1,100 two years ago. With the property assessment increases, it was time to raise their rent again for this July. I initiated a letter to each of them stating the rent will increase as of July 1, which gave two options: they could leave the property by June 30th in accordance with their lease, or they could sign on for another year at the increased rent rate. Both chose to stay in the property, and they signed another year at $1,150. This is still below market value for the houses, but we’re happy with the lack of maintenance needs in these houses over the last 5 years. We’re in the middle of replacing the flooring in one of the houses. That house has a family of 5 and a dog living in it, so it’s not surprising that it’s worn out faster than the identical one next door with one person in it.

We have a 2 bed, 1 bath house that rents at $795. She’s been in the house since July 2018, which means that her lease ends June 30th of this year. Based on the 1% Rule (i.e., we’re looking for the monthly rent to be 1% of the original purchase price) for this house, our rent goal is $635. Since we’ve exceeded that goal for the life of our ownership, and the house hasn’t cost us much in maintenance, we chose to not increase her rent if she wanted to renew for another year, which she did. She has also spent some of her own money to spruce up the house and make it her home, and we recognize the value to us that her efforts also bring.

Another house reached out to us and asked if we were willing to renew her lease for another year. She’s been there since we purchased the house in 2017, and we’ve never increased her rent. She usually pays rent early and doesn’t ask for anything. The 1% Rule puts us at $660, and we’ve been collecting $850. Since we’ve been lenient on rent increases, I thought it a good idea to re-evaluate her terms. I plugged all the numbers into Mr. ODA’s calculation sheet to see how we were doing since the taxes increased so much on this house. Our cash-on-cash return (which we aim to be at 8-10%) came back at 19.8%. A rent increase for the sake of increasing rent isn’t worth it for such a good tenant, so we agreed to renew her lease for another year at the same rent. She wrote back: “omg thanks so much for the good news!” Happy tenants = good tenants, remember?

As for the others that I haven’t mentioned:

Two of our houses were put under a two year lease last year, so they didn’t require any action from us this year.

We have another house in KY that has a lease ending 7/31 and is under a property manager. We’ll offer a renewal option for them (i.e., we’re not interested in asking them to leave), but we haven’t worked out those details yet. Since we’re very hands off for our KY houses, we don’t know the satisfaction level of those tenants to gauge. Historically, we’ve had trouble renting this unit, costing us long vacancy times, so if we can renew their lease for even the same rent, we’re happy. Plus, having a 7/31 end date starts pushing us closer to the Fall for any future year-long rental agreements.

One of the houses that we have with a partner has a difficult tenant. I mention the tenants almost every month in the financial updates because they don’t pay their rent on time, and getting information out of them is like pulling teeth. They’ve rented there long before we owned the property, and their rent has always been $1,300, which is well below market value. We plan on offering them a drastic rent increase and a new lease term (we’re still managing under the previous owner’s lease agreement) in July for their September 30th expiration term.

While we don’t have any houses to turn over, we’re going to get into each house this summer. Since so many of our houses don’t typically have turnover, we don’t get into them as often as we should to make sure things are running correctly (i.e., don’t want small issues to go unnoticed and cost us in the long run). Specifically, we need to make sure that the HVAC filters have all been changed and verify there aren’t any red flags. I plan to give the tenants at least a month’s notice before we enter, so that if there are any maintenance activities they should have been performing, they have time to get it situated. I’ll walk through with our typical move in/out inspection form and note any concerns or areas of interest. I also understand that by being visible, I’m opening myself up to being asked for things that a tenant may not necessarily ask for via email or text, but I’ll cross that bridge when I come to it. For now, we’re just grateful that we have no houses to turn over and no expected loss of rental income for the year thus far!

This one has been pretty easy, but we did have an interesting issue arise with the first tenant.

This is our largest house at 4 bedrooms and 1.5 bathrooms, and 1281 square feet. It’s a cape cod style house, so the upstairs has slanted ceilings, the half bath is not anything to write home about, and the HVAC struggles to work up there. The carpet on the stairs could really be replaced (but it hurts me to spend money on stairs because they’re soooo expensive compared to carpeting a room!). But the house has a huge fenced-in yard with a nice deck that’s a great selling point.

The kitchen was renovated at some point, so that’s held up well – and lets face it, who doesn’t choose baby pink knobs for their new kitchen cabinetry? But the plumbing and roof have been painful.

I’ve already told many of the stories about this house through other teaching posts, so bear with me if things sound familiar.

LOAN

The house is in Richmond, VA, and the purchase was very simple. We offered $109,000, and the seller countered with 112,500 and 2,000 in seller subsidy (i.e., closing costs), which we accepted. It was listed on June 22 at $119k, and we offered on June 25, so I’m actually surprised we got the contract agreed to so quickly.

Quick note here: after reviewing real estate contracts in NY, KY, and VA, Virginia wins. Sure there are several states that I haven’t ventured into, and this is an extremely small sample size. The paperwork is simple yet thorough, all while being in plain language. So if you’re needing a template to work off of, look up Virginia’s purchase agreement.

We settled on a 30 year conventional loan at 5.05%. We received a $200 lender credit since we closed on several properties in a short period of time. This is the house that we refinanced and received an appraisal of $168,000! We had already started with equity in the house because it appraised at $114,000 at closing.

INSURANCE

Interestingly, we couldn’t insure the house through the company that we had gone with because they have a 5 rental limit. Our agent was able to quote us through another company though, so our process appeared seamless. However, the quote was much higher than we anticipated. We went through a friend to insure it, but shortly after closing (literally a week), we were able to find an even cheaper option – that was awkward.

THE NEIGHBORHOOD

Not a category that usually gets mentioned. I discussed the neighborhood of the one house we sold already, which was because I didn’t realize it was in a higher-than-average crime area that tenants honed in on. But this neighborhood is worth mentioning.

Rentals aren’t prevalent here. In fact, many of the homes are the original owners. While working on the house when we first purchased it, the neighbor across the street approached me. He as-politely-as-possible threatened me that this is a nice neighborhood, that everyone keeps up their property, and that they don’t want any trouble. I assured him we have good standards as landlords, and we haven’t had any neighbor complaints for any of the tenants we had in our houses.

The location also comes into play for our first tenant.

TENANT #1

This house is under a property manager for 10% monthly rent.

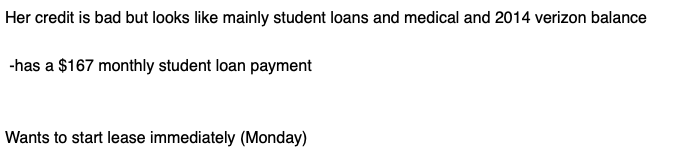

As with most of our tenant searches, no one fits perfectly into our requirements. We offset this by a higher security deposit or having another signatory on the lease. We had two prospective tenants – one was a mother/daughter combo (an adult daughter) and both had bankruptcies in the last year; the other was a man and his family that had an eviction 7 years prior. We chose the one with an eviction. His application actually said that he “will also respect the property to the utmost.” Boy did he.

He first requested that the carpet be replaced. It was actually a reasonable request because it wasn’t the best. Here’s the carpet on the second floor. Old, bottom of the line padding; a gorgeous blue; lots of wear spots.

We decided to refinish the wood floors on the first floor because 1) he wasn’t moving in for two weeks, and 2) it would save us in the long run to put that investment into the floors instead of carpeting every few years (and risking someone completely ruining it before its useful life was up). It was $1850 and the company was able to start immediately and get it done before the tenant moved in (granted, it was the day he moved in, but it did get done). And the refinish turned out great!

He asked us for a screen door, but we said that wasn’t a necessity. He asked if he could install one himself. We agreed, as long as it didn’t prohibit our access (e.g., he can’t lock it, give us a key). This later becomes an issue because he locks it after vacating and we need it rekeyed.

This tenant had a few late rent payments and struggled with paying rent on time, but overall he was a good tenant to have. He took care of the property and let us know when he ran into issues (it’s amazing how many people don’t tell us of a problem in a timely fashion).

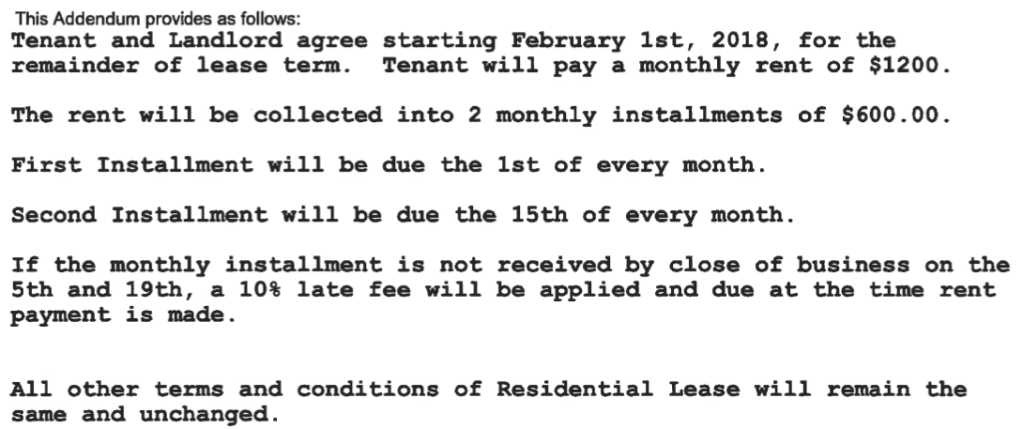

Just as we did on House 5, we offered this tenant the opportunity to pay rent in two installments each month. His rent was $1150 from August through February. He took the opportunity and we executed an addendum to change the rent to $600 twice a month. Again, it’s an inconvenience to us to collect two rent payments, but it theoretically should save the tenant money if they’re constantly in a position that they owe late fees (if he usually pays $1150+115=1265, then 1200 is a better position).

And then the fun happened!

I was at WORK one day, answered my work phone, and someone on the other end asked to speak to the owner of [this house’s address]. I barely used my work phone for work calls, so to receive a personal call on my work phone was very surprising. I informed her that I was the owner. She then went on to ask me questions about the tenant occupying the residence. I couldn’t answer a single question – hah! I let her know that I really didn’t know who was living there or the status of the home because I have a property manager. She was very nice and understanding, and she called my property manager.

She was with the school system. Apparently, our tenant had moved into the City public school district, but kept his kids in the adjacent county school system. It was April. I thought it was ridiculous that the school system would investigate this with 6 weeks left of school, but technically, he was in the wrong. And get this – he blamed me for it! Our nice tenant turned on us and went crazy. He claimed that he could just walk away from the house …. honestly I don’t remember his reason for it, but somehow he thought he had a case.

Virginia has a wonderful statute that says if the house is vacant for 7 days, the owner takes possession without any court interference. There’s also a statute that says we can’t collect double rent, and we need to be doing our best to rent it out if given notice. We tried to keep communication lines open with the tenant, but he was silent. We had told him that we were willing to release him from his lease obligations if we found another tenant, which we did. He was responsible for May’s rent and late fees, and we would have a new tenant move in June 1. We also informed him that he would be responsible for the leasing fee associated with finding a new tenant, which was basically considered the ‘lease break fee’ and is fairly generous ($300 instead of a standard two-months rent that’s typically seen as the fee). It kept going south from there.

On top of the rent owed, he had several lease breaches – room painting (clarification: rooms are allowed to be painted as long as it’s a neutral color or painted back to a neutral color before vacating), wall patching and painting, house cleaning, mowing, re-keying, and utilities since he turned them off. By mid-June, he still owed us $874.76. We made an arrangement with him that he’d pay a certain amount each pay check, but he failed several times. We finally threatened to take him to court, which would affect his credit score and increase the balance owed since court fees would become his responsibility. Since he had been working to rebuild his credit since his bankruptcy, we thought this would light a fire under him.

We went to court.

Court also added a 6% interest charge on the outstanding balance, which now included the $58 court fee.

It took him over a year to pay the balance. By the time the court judgment arrived, his balance (after paying $50 here and there was $660. The court doesn’t put a timeframe or process on the judgement, but leaves it to the two parties to determine the payment schedule. He didn’t adhere to it well, but we did eventually get the whole balance paid. Mr. ODA also took this opportunity to have fun with calculating interest payments on a declining ‘principal’ balance that isn’t getting payments on a predictable schedule!

TENANTS #2 & #3

These tenants were/are much easier. The second tenant in the house had several large dogs, but we didn’t see any damage to the house. She eventually broke the lease to buy her own house in November 2020; we can’t fault someone for wanting to take advantage of low interest rates! She gave the appropriate amount of notice, but the lease was going to be broken as of 10/31, which isn’t a great time to have a rental come open. She ended up being very gracious with the situation, paid us one month of a lease break fee, and we kept her security deposit.

Right after she gave us notice, we had an old tenant reach out to us. They had moved back into town (I’ve mentioned them several times) and asked if we had a 4 bed/2 bath house available. Amazingly, we did. We showed them the house and they signed a lease within a few days.

Since turnover was fast, and I didn’t really know the status of the house, I didn’t get a chance to paint the house. All the rooms had been white except for the one room that I repainted after the first tenant had painted it lime green. The house really needs a whole paint job, and so I offered her an incentive. If she wanted to paint any of the rooms, she could knock $75 off the rent per room. So far she’s painted three rooms.

MAINTENANCE AND REPAIRS

The plumbing in this house has been horrendous. We had the tub snaked as soon as the first tenant moved in ($150). We then had issues with hot water, which required several adjustments to the water flow rates to coincide with the tankless hot water heater ($325). We had the upstairs toilet serviced ($120). Then a year later, we had to service the hot water tank again ($570). Tenants had complained that the upstairs sink drained slowly. We had attempted to snake it and fix it several times, but it never seemed to work. We finally just bit the bullet and replaced the plumbing – from the second floor to the crawl space. That work and the drywall patching cost us $1563.

Then there’s all the roof work. Shingles had flown off during a storm, so we had those replaced ($350). We also had a leak in the flat roof over the laundry room. We had a roof guy come out, and he said the roof hit its life expectancy. He replaced the pitched roof ($4135), and not the flat roof. So we’ve still had issues there that will need to be addressed.

SUMMARY

That sounds like a lot of money, but we’ve owned this house for 4 years now with our rent being double the mortgage (slightly better now too with the recent refi). When purchasing properties, any good investor is going to build maintenance and capital expenses into their numbers that determine if it’s a worthy investment. Rent cash flow wins out, and all the rest is just the cost of running our business – not to mention the $60k of appreciation we have on paper in just 4 years. It’s also worth noting that these things took up about 10 days worth of action from us over those 4 years, so most months, we just collect the rent with no other action required from us.

No property is going to be perfect, and this business relies on people, the tenants, to make the business profitable. No path will take a straight line, and being flexible to the ebbs and flows of rental property investing help make it fun too!

This was a mess. I learned my lesson to research each property individually and not to make any assumptions. I also learned my lesson to hold true to our standards and expectations for a renter. We owned this house for a year and a half, but we learned a lot about tenants and the selling process. Hey, every struggle is a learning opportunity for next time, right!?

Mr. ODA showed me House 6 first (5 and 6 closed at the same time, and on my numbering list, this one came second… so try to overlook this awkward numbering!). I researched the area and the house’s history in detail, and I decided that it was worth pursuing. Very shortly after that, he approached me about House 5. The house was in better condition than House 6 and was literally only half a mile away. I assumed it was in the same neighborhood. I was wrong, and that’s where things went downhill fast.

LOAN

This house was so cheap that we needed an exception approved to get a loan. The purchase price was $60,000, which means a loan with 20% down is $48,000. The cutoff for even approving a loan with our regular lender is typically $50,000. Since we were below that threshold, we were ‘penalized’ by the rate.

I covered the closing snafu in the House 6 post, which also highlights the decision-making on the loan terms. Since this house was below that $50k threshold, our options were: 5.125% witha $200 credit or 5% with no credit. The higher interest rate would cost us an additional $1300 in interest, which isn’t offset by the $200 credit, so we chose the 5% rate. Hindsight: If we had known we would sell it just 18 months later, the credit would’ve been the better choice!

We purchased the house in July 2017. We immediately started aggressively paying towards the mortgage since it was the lowest balance and the highest interest rate.

We rented the house for $775, which far exceeded the 1% Rule.

WORK ON THE HOUSE

We did a lot of work in the yard. Here’s what the house looked like at some point before we owned it. It’s cute!

While it was under contract, the house sat vacant, so there were a lot of overgrown bushes, flowerbeds were filled with debris and no remnants of flowers having lived there, the lawn hadn’t been cut in a long time, and the tree in the front left had been removed at some point, leaving behind a mound of a stump and mulch that also collected debris. It’s a shame, and I kind of wish we had brought this little 2 bed/1 bath house back to life like it was in this picture. But I digress. Although this picture shows that the previous owner took care of the property, and that’s what attracted us to the purchase.

The floors were in immaculate shape, and the kitchen was quaint, but in decent shape. We purchased a new refrigerator before we could list for a tenant.

The bathroom needed a lot of help, but we didn’t want to overhaul it. The medicine cabinet wasn’t working anymore and the glass was cracked, so we wanted to replace it with just a mirror that covered the old medicine cabinet hole. Interestingly, we found a stash of 100s of razors behind it! (Apparently this is a thing from times gone by. You finish your blade and then you shove it behind the medicine cabinet for it to reside in the wall for all eternity.) We had several plumbing issues in the house. The drain pipe for the tub had multiple kinks in it, which caused the water to drain slowly and be more easily clogged. This would have been a major overhaul to get new plumbing installed in a way that was more direct.

The electric in the house was in need of work. We fixed quite a few electric-related-things while we owned it, but re-wiring the house was a major expense that would’ve come due in a few years.

TENANT ACQUISITION

The house was in great condition, had a big lot, was in a located close to the downtown area, and was on several bus routes (I even had a bus driver stop and ask me what the rent was on the house while I was working out front). It seemed like a great investment. We had several showings to qualified individuals….. who then went home, researched the house, and saw that it was in the highest crime area on Trulia’s crime map.

After sitting on the market for 5 weeks, we lowered our standards. There’s a reason you have standards as a landlord – it’s because if you select the right tenant, you’re saving yourself time, money, and headaches in the future. Here’s the email from our property manager. There are multiple red flags, and yet we gave her a chance.

The prospective tenant provided us with an employment verification letter showing that she had just started a new job, her most recent pay stub corroborating the employment verification letter, and wrote a decent introduction in her application. Between it being 5 weeks with no tenant and it now being mid-August (with it harder to rent in the Fall), we overlooked her credit score of FOUR HUNDRED AND FORTY EIGHT (448) and SEVEN (7) accounts sent to collections. I don’t recommend you do this. Oops.

EVICTION

This is the fun part to recount. It’s detailed, but I think it’s interesting.

RENT COLLECTION

She moved in August 2017. By December 2017, we already had enough issues that she wasn’t going to be trusted going forward. We’re very flexible landlords, and we’re happy to work with you on any issues as long as they’re communicated up front and timely (meaning, if we have to continuously reach out to you for rent, you’re not in a position to ask for favors).

We had allowed PayPal to be used to pay rent, but every month there was an issue. She either sent it in a way that incurred fees (after being told that she would be responsible for such fees) or it was sent in a manner that caused PayPal to hold the funds and not immediately release them. After December’s rent was late, the late fee wasn’t paid in full, and there were fees taken out by PayPal, we cut her off from electronic payments. Our property manager informed her that going forward, all rent had to be received by her office (either by mail or drop off) before the 5th.

Speaking of flexibilities – we noticed that she needed to send us rent based on each pay check, versus having all the rent money at the beginning of the month. She was paying us a late fee every month. Her rent was $775, and her late fee was $77.50. That meant every month, we were collecting $852.50, which really wasn’t necessary. We offered a change to her lease terms – rent was due on the 1st and 15th. As compensation on our part, rent would be increased to $800, split into two $400 payments. However, if rent was late, the late fee was now 10% of the late payment ($40) or up to $80 if she was late on both installments. She agreed to this, as it saved her money each month and set her up for success by being able to set up a system with each of her paychecks. We didn’t like that our relationship with the tenant had come to us hounding her over money, so we thought this was the best path forward for both sides of the party. Here’s the addendum to her lease.

And yet this didn’t change anything!! The addendum was signed at the end of January 2018. She paid February’s 1st $400 late. Then she didn’t pay February’s 2nd $400, and we had to reach out to her several times before even getting a response… after she also didn’t pay March’s 1st $400.

Our property manager filed unlawful detainer (eviction) with the court, and that got the tenant’s attention. She then had to pay the balance due, as well as the court filing fee, before March 30th (court appearance date) to dismiss the court action. She showed up to court with the cash to pay and then everyone just went home. You can’t evict someone who has paid in full, even if the process of collecting rent was unnecessarily burdensome.

And then came April. There was another story about a medical emergency and a new job on the books. We had agreed to a new one-time schedule for April’s rent payment, and she missed those deadlines and was incommunicado. We sent her another default notice on April 25. Note that this medical emergency was for her “husband.” This is the first that she had implicated herself that someone may be living in the house other than her and her son. She paid her balance owed on May 4th.

On May 8, she was given another eviction warning notice for lack of May rent (the 1st $400) and gave no response to requests for information on when to expect rent. After continued lack of payment after that notice, she was served with another eviction notice. On May 17, she was given 30-days notice to vacate the premises by June 17, 2018 at 5:00 pm. But then she paid in full and on time. We then changed her lease terms to state she was on a month-to-month basis and she would be granted 30 days notice when we (or she) decided to terminate the lease agreement. It was signed on July 16.

Guess what? She didn’t pay September’s rent. At this time, we also addressed her husband.

She was married when she applied, but we didn’t know. Justnow as I was looking back through our files to write this post, I saw that her pay stub she used for employment verification said that she was filing her taxes as married. I hadn’t seen that before. In all our visits to the house, there were always other people there. There was one man that seemed to be around 90% of the time. We overlooked it, but our lease did stipulate that anyone who stayed for more than 2 weeks was required to pass a background check and be on the lease. I strongly suspect that this individual was not going to pass a background check, which is why it was never disclosed to us that she was married and another adult was living there. Our property manager informed her that only she and her son were on the lease, and that if anyone else was living there, they had to be on the lease. She asked if we were referring to her mother-in-law visiting, our property manager said that it appeared to be her husband was living there, and then she ignored us.

We gave her our 30 days notice on October 5 to vacate, meaning she had to be out by November 5. Our property manager reached out to her on October 26 to see if she would be out earlier and set a time for key pick up. The tenant nonchalantly stated she wouldn’t be able to make it out by the 5th and she’ll be out by the 9th. Umm, excuse me, ma’am, but that’s not how this works. We held strong to the 5th and she lost it. Our property manager said that her lease is over on the 5th, and if she was not gone by then, the court fees would be her responsibility for us to get the court and local police department involved for her removal. She got angry and claimed that we didn’t handle the rental well at all, that we couldn’t charge her any court fees, and that she should charge us for not being able to use her tub because it was clogged (guess what on this one? The plumber removed things like a dental floss pick from the drain, immediately making it her fault (and at her cost) for said clog). She then said: “Lets just hope your (sic) as speedy with my deposit as you all were with terminating the lease.” I laughed out loud on this one just now. We should have terminated her lease an entire year before this discussion happened, but we kept working with her! Hysterical! Gosh, and to think this wasn’t our worst eviction process (more to come :)).

SELLING

A friend-of-a-friend was attempting to purchase a house in the same neighborhood as this house, and they ran into multiple issues causing them to walk away from other deals. Mr. ODA approached him with an opportunity to sell this house, which had similar specs to the one that they were pursuing. The buyer spoke to his wife and father about the deal and agreed to move forward. Of course, this deal was not easy.

The contract was ratified on October 31, 2018. We didn’t close until January 8, 2019. Our typical close time on our purchases is 4 weeks. We’ve done faster, and we may have done a bit longer if the time of month lined up better for our finances, but over 2 months was horrendous. Since our tenant was moving out on 11/5, and the closing was expected to be no later than November 30th, we didn’t pursue finding a tenant.

The appraisal was late being ordered, which was somehow allowable. Then it came in at the beginning of December at $65,000; our contract was for $68,000. We split the difference ($1000 from the buyer, $1000 from the seller, $1000 from the agent who was dual representing).

On December 18, our Realtor finally pushed back on the buyer’s side of the transaction to get things done. But it was Christmas time now. With so many offices closing for the end of the year, we weren’t able to get a closing date until the first week of January. The buyers were signing paperwork from Pennsylvania, which caused more delays because of having to send the paperwork back and forth for everyone’s signatures.

We sold in January 2019 for $67,000, after having purchased it for $60k just 18 months earlier. While this seems like a great deal, it’s not an automatic $7k in our pockets. You need to account for our closing costs from the purchase and sale (about $6,500), loss of rent for two months while trying to close the sale and the 6 weeks of no tenant when we purchased it, utility costs associated with vacant times, and costs to fix things around the house during our ownership. However, during that time, we had a tenant paying our mortgage (covering the loan interest and paying down the principal), and we were collecting more rent than projected because of her continued late payments.

1031 EXCHANGE

We made the decision not to pursue a 1031 exchange on this house. A 1031 continues to defer the depreciation to the next property, and it allows capital gains to be deferred. Based on current tax law, it can be done infinite times. However, there are extra lawyers and fees that come into play, so it becomes worth it when you have big dollars at stake, and that you have another property to purchase quite quickly after selling the first one.

The appreciation on the house was minimal given that it had only been 18 months since purchase, we had two sets of closing costs to add to the cost basis, and we hadn’t earmarked a place for that money to go upon selling. Plus, the cost of an intermediary would continue to eat into the “profit” versus tax paid, so we just went ahead and planned to pay capital gains taxes on it. Unfortunately, since we had depreciated the structure and the fridge over the prior 18 months, that paper money had to be brought back into the fold when calculating our taxes the following April. That’s several thousands of hidden money that is easy to forget about.

Depreciation is a great tax break when you own the property. The IRS assumes the value of your asset is being reduced by wear and tear and father time. This is true. It’s why if a landlord neglects the property and isn’t active with maintenance, renovations, and other replacements, the property will turn into a trash-heap in time. However, when you sell the property, you show the IRS that it in fact did not do that. If someone is willing to buy my property for more than I bought it for, then it obviously didn’t depreciate to a lesser value. I have to pay the IRS back for the depreciation assumptions that I was allowed to make over the time I owned it, plus pay the tax on the actual profits. Bummer, but logical.

In summary, we bought a cheap house and got a poor tenant. We had a TON of headaches with that tenant. We had to do a few house/yard projects over the ownership life of the property, but nothing worrisome and not already built into our numbers. Somehow, we made it work that eventually the tenant always paid up and then some (late fees). We made mistakes, we learned lessons. We figured out a set of streets to avoid for future purchases, learned how to sell an investment, and learned how to file taxes on an investment property sale. The story is fun to look back on. I’m glad we experienced what we did. But I don’t want to do it again.