Early on in our investing in real estate, we were told to make regular walk throughs of the properties. We were taught to use changing the HVAC filters as the guise to get into the property and look around once a quarter, even if changing the filters was put in the Lease Agreement as the tenant’s responsibility. Realistically, we have mostly great tenants that will tell us what goes wrong in the house and take good care of it. But this isn’t always the case. Plus, once we added two kids to our lives and I no longer worked (i.e., no longer have a set schedule for being out of the house), the rental properties moved to the back burner unless a tenant brought something up specifically.

After our experience with House 9 – both the hoarder and the guys who just turned off the gas to the stove instead of telling us about a gas leak (yea….), we decided it was important to get into these houses at least once a year. In many instances, either one of us or our handyman is in the house at least once a year for a repair, so it’s not a big deal. But there a couple of houses we hadn’t seen in a while. Add in the pandemic, and we really haven’t been in houses all that much.

We moved out of Virginia, where we have 9 properties, last Fall. That means getting into these properties is more of an effort that needs to be properly planned and orchestrated now. We already planned to be in Virginia for a wedding in September. However, the issues that stemmed from the flooring replacement in House 3 made it imperative that we get there as soon as possible.

I emailed all the tenants to let them know that I planned to walk through the property for a quick inspection. I asked if they had any definitive times of day or times of the week that they would prefer I not arrive (e.g., works night shift, child’s nap time). I let them know that they didn’t need to be present for the walk through, that I would send them a document outlining anything I noted, and that I would try to avoid their times of being unavailable, but didn’t guarantee it.

Of the 9 properties, 3 are with a property manager. We took two off the list after they responded positively about how they replace the filters, had several conflicts around the holiday weekend, and we have been in these houses for repairs in the last 6-9 months. One is a house that we had been in regularly and knew she was treating it like we’d treat our home, and the other had our handyman in it recently, who said, “they seem to be by-the-book people.”

While there, we took pictures of the front and back of each house to give to our insurance company. We have a commercial liability umbrella policy, and the underwriters like to update the file every 3 years (details in a future post!). So instead of posting pictures of all the “dirty laundry” (literally and figuratively) I encountered, here’s a picture for this post that’s of our nice, pretty house with great tenants. (Note – Mr. ODA tucked in that piece of vinyl on the back right just after I took this picture!)

HOW DID IT GO?

Well, I started in a house that I’ve only seen one room of since we bought it (this is owned with a partner – he and Mr. ODA have handled most issues to date). I was overwhelmed. There were 5 full/queen size beds in the house, where the lease holds a husband/wife and adult daughter. There was stuff everywhere. We just replaced the HVAC in the house, but they had all the windows open, fans on, and the HVAC running. I knew that there was water damage from a plumbing issue, but I didn’t realize that it had affected the kitchen and the basement (thought it was just a part of the basement). It was a hard way to start. I should have started with an easy one that I knew would be in great condition. 🙂

From there, it went pretty well though. Most people obviously cleaned and changed the filter because I was coming. This is a good thing and a bad thing. If I don’t show up for a year, is the house cluttered and a mess? Then there was a house that I went in, where he didn’t bother picking a single thing up for my arrival. Dirty socks, things strewn about. It wasn’t to the point of hoarding, and I didn’t find any food laying around to attract pests, but it wasn’t how I would manage a household.

I ended two days of seeing 7 houses with a lengthy to-do list. Plumber, HVAC technician, roofer, electrician, pest control, and then a random assortment of things that I don’t know who to call for (e.g., replacing bedroom doors, closing in literally 2 sections of chain link fence that are missing). I also made note of things that will require our attention during a turnover, but that don’t necessarily require attention right now (e.g., removing old caulk around the tub and re-caulking it).

TENANT FOLLOW UP

I sent an email to each tenant. I thanked them for their time, outlined the items that I noted needed attention (e.g., vacuum HVAC filter cover, vacuum dust build up on bathroom, unblock exits), documented anything we did while we were there (e.g., gutter clean out, caulking), and sent a list of reminders that are the lease items we see most frequently broken (e.g., only adults that have passed the background check and are on the lease may reside there; any fines incurred by lack of yard maintenance will be passed onto the tenant who is responsible for yard maintenance per the lease; change air filters no less than every 3 months; all surfaces are to be cleaned and remain clear of food particles as to not attract pests).

Contractors are scheduled a couple of weeks out, so nothing is moving very quickly, but at least we’ll get into these houses for some preventative maintenance.

Lesson learned that when life gets in the way and active management of rental properties becomes a little too passive, the to-do list grows pretty long. There was nothing critical that we weren’t aware of, and we could handle these things during turnover, but I’ll try to get ahead of some of it in the near term, especially where we have long term tenants.

Back in May, I was a guest on Maggie Germano’s Podcast, “The Money Circle.” I shared some of our background and how we started investing in real estate. We brushed on topics like establishing an LLC, tax advantages, and how you don’t need to start big to just get started. It was a brand new experience for me, but I’m passionate about our real estate experiences, and I loved being able to share. I hope you’ll check it out!

I just shared the details of the home inspection contingency in the real estate purchase agreements in my last post. I was laying the foundation to share what we’ve encountered to invoke the termination clause of the home inspection contingency.

COMMERCIAL PORTFOLIO

There was a time where we were trying to grow fast. We wanted to work smarter not harder, so we investigated commercial portfolios instead of buying one single family house at a time. We worked with our Realtor’s office’s commercial team to find an off-market deal of several houses. The owner of all these single family houses had lumped several houses in his portfolio by geographic area of Richmond, VA. He had provided us with 13 ‘sub-portfolios’ to review, but he was willing to sell individual houses.

We went through the entire portfolio to decide which houses we were interested in. We were able to eliminate several from the start because his rent to purchase price ratio were far from the 1% Rule we aim for (the monthly rent amount (e.g., $1000) is 1% of the purchase price (e.g, $100,000). We identified 10 houses we wanted to see and met up with the owner’s property manager to get into each house. Afterwards, we went through the list of houses, the comps we could find for purchase price, and discussed the condition of each house as we saw it. We ended up making an offer on 5 houses.

We received the ratified contracts on May 9th of that year, and we immediately contacted our home inspector to come through the houses with us. We met with the property manager, our home inspector, and our Realtor to inspect the 5 houses in one day. We negotiated with our home inspector that he didn’t need to write a report for each of the houses; I would take notes as we went through everything, and he wouldn’t charge us full price for the inspections.

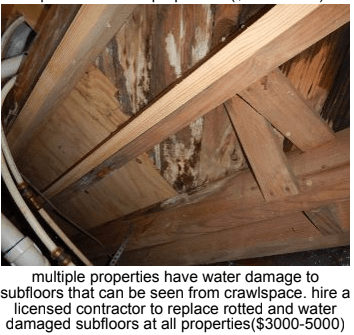

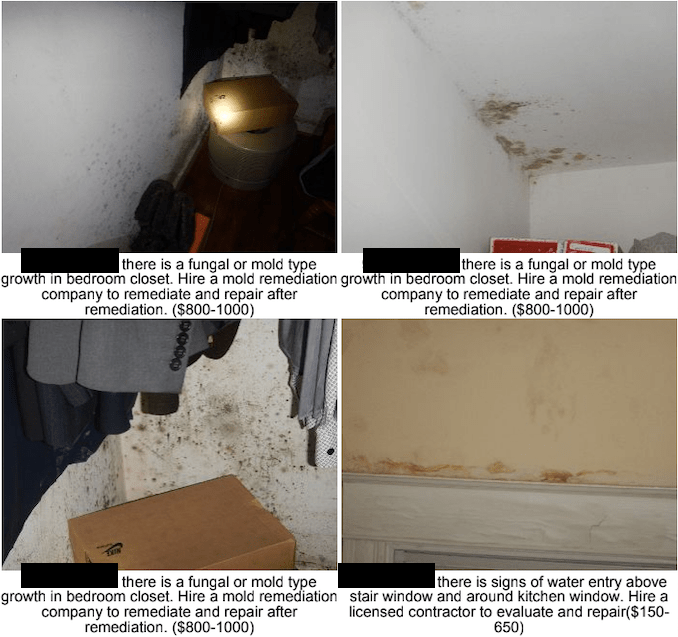

We knew the houses weren’t in great shape, but we weren’t prepared for all the details we found in the home inspections. During our time at the houses, the tenants were quick to complain about the maintenance on the properties, saying things would take a long time to get fixed or they wouldn’t ever be addressed. The inspection found strong evidence of mold, patch jobs in structural beams in the crawl space, appliances not in full working order, windows screwed shut, and several other minor things.

We attempted to negotiate by the seller providing $10,000 per house in seller-paid closing costs. We didn’t ask for anything to be fixed because we saw the work that had been done in these houses, and we wanted it done right. The seller denied our request for funds to address the home inspection issues, and we walked away from all of the contracts.

FIRE DAMAGE

This was a hard one for me to walk away from. The house itself was in a high-crime neighborhood of Richmond. However, only THREE! parcels away, houses were being torn down, rebuilt, and sold for significantly higher than purchased. I saw the potential of the area’s revitalization. But we were not in the business of flipping houses nor doing major repairs. Not only were we not interested in that because we wanted to be able to create the cash flow as fast as possible, we also want to be able to hold these properties as rentals instead of flipping them so we maintained a continuous income stream.

There were several concerns when we walked through the property. The kitchen was a mess, there were signs of water damage in multiple places, the floor felt soft upstairs, the upstairs deck didn’t seem stable, the house needed a lot of TLC with the overgrowth, and then best of all – clear fire damage to the structure of the home when we went in the basement.

This isn’t a picture from when we were looking at the house, but this is the condition 3 years later, which shows just how ‘great’ of a house it was. 🙂 This is the backyard.

We were under contract for $72,500 in May 2017. The house recently sold for $296,000. Although it seems we missed the opportunity that I felt was there, I found pictures of a failed flip attempt in 2019/2020 that uncovered even more damage behind the walls than we even knew (although we suspected), and none of the houses around it have sold for nearly $300k. Therefore, we don’t believe that was a reasonably-expected sale price had we taken this beast on. And what’s not known in those numbers is just how expensive the flip was to that owner, both in headaches and wallet!

A KENTUCKY MESS

Mr. ODA went to see a house in Winchester, KY without me (it was easy because he was working near there, and it wasn’t worth me packing up our baby to go walk through a house that we may not even want). He and our Realtor walked the house and decided it was worth putting an offer in. The house had two units set up inside it, which was a goal of ours (duplex = one building the maintain with two income streams). The cash flow on it was great, so he probably turned a blind eye to too many negative issues during that first visit.

The inspection was $500. I was there for the event, but didn’t walk the house with the inspector. He ran through everything with me after he was done, but the tenants were present, and I didn’t want to bring my baby into their smoke-infested house (first red flag because we don’t allow smoking in any of our properties).

The first thing the inspector said was that the roof needed replaced. He pointed out that several tree limbs were in contact with the roof, and the roof had considerable algae growth on it. Basically, everything on the outside of the house needed repaired or replaced: siding, decks, roof, gutters, removal of vines on the house, negative slope of ground towards the house. The doors and windows were old and broken, so none had the proper seal to prevent water infiltration, in addition to not being able to maintain temperature.

On the inside, there were several code violations with how the kitchens were built (e.g., venting for range), and several large cracks in the walls, some of which were patched poorly and never repainted. There were five or six electrical issues that needed to be addressed immediately because they were a fire hazard. There were signs of water damage in the ceilings, as well as in the bathrooms where the peel and stick tiles were ‘floating’ and warped.

As if that wasn’t enough, the straw that broke the camels back for me was the head room given for the upstairs unit entrance. The required head space by code is apparently 6’6”, and we only had 5’6”. This seemed to be a big problem because an average man is 5’9”, and the average height of women at 5’4” doesn’t exactly give much wiggle room.

I was worried about all the work that needed to be put into this house. The tenants weren’t taking good care of the house, so it wasn’t worth putting a lot of money into it, just for them to destroy it. They had been there for a while, so it wasn’t like they were going to leave voluntarily any time soon. The neighborhood wasn’t in great condition, so a fully renovated house wasn’t called for when it came to resale or the type of client looking for a rental there.

It was a difficult balance, but the house had way too much deferred maintenance, way too many things poorly fixed/maintained when there was an attempt, several unfinished projects, and too many code violations to move forward. Mr. ODA really wanted to buy a house in this area before the summer was up, and he was pushing for the cash flow side of it since it had two separate units bringing in income. But that cash flow is non-existent if you’re having to put it back into the house.

These are the three main stories that have stuck with me. We learned a lot about houses through the process, and we feel we made the right decision on each of them to walk away. Through these experiences, we solidified our decision-making to focus only on houses that have been properly maintained and require little work to get rented. Having a unit already rented with long-term tenants isn’t always the “diamond in the rough” that you think it is.

The inspection is buying you information. Once you find out that information, the money is a sunk cost, and you should use it to now choose if the house is still worth owning or not. While inspections aren’t exactly cheap and aren’t tax deductible if we don’t buy the property (if you have a legal strategy, drop it in the comments please!), that information gained is important. That $500 “lost” is better off because you’re not buying a money pit that will cost a lot more in the long run. Remember, this is a business, and it’s best to keep your emotions out of it. Don’t pinch pennies and end up costing yourself big dollars later on.

Most times you’ll do an inspection, find some things to fix or negotiate down on the purchase price, and even find yourself in a situation where the inspection “pays for itself.” Other times, it doesn’t work like that. Life lessons can cost money, and inspections can help point out duds so that those lessons don’t end up costing a lot more.

I had this post teed up to share at the beginning of the month. I thought the story line was going to be that I went on vacation while all new flooring was installed in a home 500 miles away with little effort by me. It’s no longer a positive story. This post is to share that there’s struggles, but they’re only a few weeks of the year. It’s not a cumbersome year-long process to have rental properties.

This house has the same tenants in it from the time we purchased it in 2016. They’re a family of 5 with a dog, so it’s not surprising that the carpet reached its useful life. I don’t know when the carpet was installed, but I assume it was right before these tenants moved in, which was a few months before we purchased the house. The carpet was matted down in the high traffic areas, and it was starting to separate at the seams. The vinyl between the kitchen and laundry room was also peeling back. While I wouldn’t typically look to do such a large project while tenants are still living there, we made the exception to keep them happy and wanting to stay even longer. We decided to replace all the flooring in the house, except for the bathrooms.

My first lesson learned: keep these major projects to vacant houses. While there are exceptions, such as these long term tenants, the tenant just doesn’t understand the work that’s going to go into it. We had a bad experience that dragged this out for multiple weeks, but even with that, the tenant had a lot of complaints about having to move their closet things and move their furniture. I kept reiterating that it’s short-term ‘pain’ for long-term gain, but he kept wanting to tell me how much work it was. It was hard to not retort that he asked for this and we could have said no.

PURCHASE PROCESS

The experience to purchase the carpet was less than satisfactory. We’ve had several positive experiences, so I wasn’t going to name the company over this one incident, but it just keeps getting worse, so here it is: Home Depot. Eight phone calls before installation, and that doesn’t count the mess I’ve managed for the last two weeks. Typically, I would just go into the store to make the purchase. However, our closest store is now a half hour away, and they have an 800 number, so I thought it would be fine. I should have just driven down to the store after the measurement was done.

I was trying to compare replacing all the flooring with vinyl plank against putting sheet vinyl and carpet back in. In a previous house, we spent slightly more by tearing up the old carpet and refinishing the floors under it. We saw it as a long-term investment. Instead of replacing carpet every 5 years, we just needed to mop the floors, and they’d last longer. For this house, since I knew vinyl installation was expensive (relative to carpet), I thought maybe it would be better for us to spend more to get hard surface flooring installed throughout the house instead of replacing in-kind. The house was built in 2007, so I didn’t have the prospect of beautiful hardwood flooring already being under the carpet.

Home Depot’s process to compare the two was painful at best, so I gave up on the comparison between carpet/vinyl and hardwood/vinyl plank.

They run a promotion that carpet is free installation if you spend $600. Apparently, that’s only for non-in-stock carpets. So I asked, “which aren’t in stock?” Their response? “I don’t know; we just need to try SKUs to find out.” Quite an inefficient process. Our carpet and installation came to $1.24/sf, so I quickly priced out of the SKUs that were less than that without installation in our trial and error process of finding carpeting.

The sheet vinyl always comes with a high installation price tag, so I was ready for that. I wasn’t ready to be told that several of the first ones I tried weren’t eligible for installation. I was left with one option, but luckily it’s a pretty gray-wood-look.

I finally approved the carpet and sheet vinyl options after 3 phone calls and the measurement appointment.

The receipt I received after I paid said that there were some items to pick up. Well, if I’m paying double the cost of the material for it to be installed, I don’t intend to go pick up product. That took 4 phone calls to get squared away. And honestly, it wasn’t even any of the calls I made that solved it; someone from the store called me to ask if I wanted to move forward with my quote (that I had already accepted and paid for in full), and she got it all figured out so that it was right. Or so I thought.

INSTALLATION DAY

The installer showed up to the house without the material. He missed the note that he had to stop and pick up the items because, for some reason, that’s not the norm. I truly am confused that I pay for the installation of a product, and it’s my responsibility to gather all the materials (lifting, carrying, organizing, storing) until the installation day. I hadn’t encountered this before. In the last house that we put vinyl in, we purposely saved $75 by borrowing a friend’s truck and bringing the vinyl there. That was an active decision to change their norm of delivery, so this was surprising.

The installer removed the vinyl in the kitchen, and then went to the local Home Depot and gathered the materials. He was gone from the house for 2.5 hours to do this, with the store 10 minutes away. When he returned to the house, he got the carpet completed (which honestly was impressive) in the rest of the house, and then around 7 pm told the tenant he couldn’t do the vinyl because of damaged subfloor in the laundry room. I’m frustrated because 1) he could have done the kitchen part and returned for the laundry room part, since there once was a seam, and I don’t think they would have tried to cut and mold around a doorframe to keep it all one piece; and 2) he could have told me this when he removed the vinyl before noon, so I didn’t lose a business day trying to get the subfloor taken care of.

I didn’t even know the whole story. I had to call the installation company (i.e., not Home Depot) to ask why I hadn’t been told the next steps. The customer service representative didn’t know what I was talking about. She had to call the installer to find out the story. The installer claimed that there was a “huge” “pool” of water on the floor and water was just continuing to pour into the house at the door jamb. I found this hard to believe. These tenants call us over every single weather crack in the drywall; there’s no way they had water coming into the house and didn’t tell us about it. Regardless of my frustration, the result was the same: I had to find someone to fix the damaged subfloor.

Our handymen options that we’ve used were unavailable for weeks, so we asked a friend of ours if he wanted to make some money and take care of it. He did a great job! He cut out the rotted wood and laid new plywood and luan. We would have preferred the installers handle this. It’s surprising because for a roof replacement, we sign off that they will repair any damaged plywood during their installation and bill us for each piece laid. Why can’t the flooring be the same set up? It became especially frustrating when we heard that the next installer was cutting wood on site.

INSTALLATION DAY: ROUND 2

Now we needed to reschedule the installation. I called as soon as our friend finished the job, and they said they had an installer who could be there the next day (a Friday)! I should have known it wasn’t a good thing that they could fit me in last minute. The arrival window, for this man coming from Maryland to Richmond, VA, was 10-1. At 12:30, he told me he was almost at Home Depot to get the materials. Well, the materials were at the house, which I told him. So then somehow, he took his sweet time, and at 1:30, he called to ask me where the address was. I told him the address and that no one else had an issue finding this house. He told me he had arrived at about 1:45.

At 4:00, my tenant called me to tell me that he helped the installer move all the appliances into the living room and that he hadn’t been in the house yet because he was outside cutting wood in the rain. Wait. I just had to repair my subfloor because of water damage, but you’re out there cutting wood in the rain to put into my house while it’s wet? I was also irritated that all the appliances were moved before the job was ready to be started. I called the installation company, and I was livid. I was already frustrated with the communication and process to date, and this was just icing on the cake.

As I was complaining to them about the situation, I received a text from my tenant saying that the installer said he was quitting for the day because of the rain and MAY be back tomorrow. He left, leaving the appliances in their living room, with no certainty that the job would be completed the next day. So my tenants were left without an operable kitchen (violation on me at that point) and with a cluttered living room, with no certainty it would be put back together the next day. Plus, this was originally a two day job. One day was already taken with ripping up the vinyl and replacing the carpet, meaning only a few hours should be needed to lay the vinyl. To be told this is going to be a two day job just for this installation is wrong.

The installation company tried to tell me to be patient because the installer is coming from Maryland. It’s not on me to account for this man’s 2-3 hour commute. I can’t work in DC, but live outside of DC (like many do), and say to my employer, “I live 3 hours away, so I can’t start before 11.” No. That man should leave his house at 6 to account for that difference, or you shouldn’t assign this man a job that’s too far away. Don’t inconvenience your customer, making a 3 hour job into a two day job, because your installer lives outside the region.

The company made the installer go back to the house to fix it that night. Instead, he just picked up the wet wood and tools, and left the appliances for my tenant to return to the kitchen.

INSTALLATION DAY: ROUND 3

I was adamant that installer #2 was to not return to the house. The next available date was a week later, and I said I’d rather it done right than fast. The new installer came and finished the job in under 3 hours.

RESOLUTION

The flooring is in. The communication and process was horrific. While managing the installation company, I also had to manage the tenant’s expectations and hear out his complaints. It took more effort than I anticipated, but it’s now over, and I shouldn’t have to deal with flooring in this house for another 5+ years.

This was self-inflicted. I chose to replace the flooring while a tenant was still in there because the flooring was degrading and they’ve been good tenants for over 5 years. In the future, I’d prefer to hold off until there’s tenant turnover, or I will more clearly communicate how the process works and how much effort it will take to manage while living there.

BONUS: TAXES

Quick teaching moment. The entire cost of full flooring replacement cannot be captured in this year’s taxes. The IRS expects the cost of flooring to be depreciated over its useful life, which is 5 years.

We’ll say the entire cost of the purchase was $4,000. I divide $4,000 by 60 months, which is 66.67 per month over the 5 years of depreciation.

Since I made this purchase in May 2021, I will only capture May through December for this year’s cost. The monthly cost of $66.67 is multiplied by 8 months (inclusive of May), which is a repair/maintenance cost of $533.33 for 2021 taxes.

For the years 2022, 2023, 2024, and 2025, I will capture 12 months worth of the depreciation monthly cost, or (66.67*12) $800.04. For 2026, I have 4 months left of the total cost that haven’t been claimed on my taxes, or the balance of the total cost that I incurred in May 2021, $266.68. However, if I claim this total, it will over-claim the total cost by $0.17, so this final amount should be adjusted to 266.51.

When filing your own taxes, the software typically calculates the depreciated amount for you. We enter the total cost, that we’re do a 5-year straight-line depreciation, and the amount already claimed on previous year taxes. The system will auto-calculate the amount to be claimed for the year. It’s important to keep track of these expenses year after year, to ensure you’re not claiming more than you spent.

We’re continuing our spring/summer of travel and activity, which is why there are fewer posts and lots more spending.

The stock market has increased, which has been the main factor in our net worth change. We paid $2,000 towards the mortgage we’re paying down, leaving a balance of $3,300. This mortgage will be paid off once all our rent is collected for July; it was pushed back a little bit because of the flooring replacement that occurred in one of our rentals, which is why our credit card balance is much lower than last month. We’re also still waiting for half of one property’s rent, which is the norm these days.

Utilities: $250. This includes internet, cell phones, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant.

Groceries: $518

Gas: $268

Restaurants: $165. Our credit card reimburses for many of these expenses; we received credits totaling $120.13 in the last month.

Entertainment/Medical: $1,093

Investment: $1,100

Insurance Costs (personal and rentals): $845

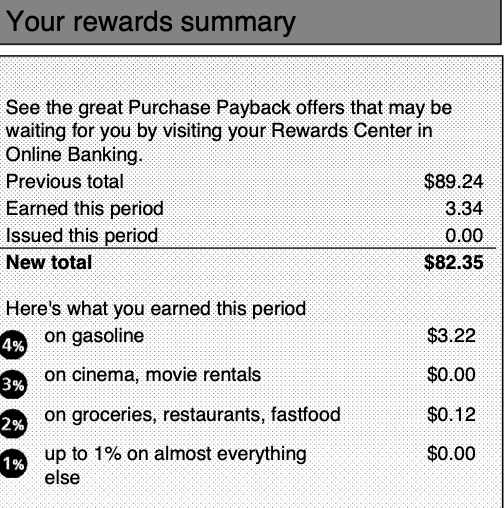

VIGILANCE ON CREDIT CARD REWARDS

Mr. ODA discovered that our PNC credit card rewards balance was decreasing, despite earning new rewards this cycle. He investigated further and noticed that we had been losing rewards for a few months now. PNC has a policy that they don’t issue their rewards until you hit $100 worth of rewards. Once we hit $100, PNC sends us a check in the mail. Since they send a check, we still receive paper statements, even though we regularly check our financial accounts online. Over the past few months, both of us checked the balance to see “ok, we’re nearing $100,” but didn’t put any more effort into knowing the details of the balance. Mr. ODA happened to notice that the statement didn’t make sense.

$89+3 somehow equals $82. There isn’t a single section on our statement or via our online account that identifies the loss of rewards Mr. ODA called PNC to ask for more details and learned that our rewards expire after 2 years, despite their policy of not issuing a check until you hit $100. They basically said, it doesn’t matter that your account is over 10 years old, or that credit has been used less in the last year due to the pandemic, or that they don’t clearly identify the expiration of rewards and just identify a lower balance. As a comparison, and I keep going back to Chase, but Chase changed up their reward categories to allow the consumer to earn more rewards during the pandemic (e.g., in addition to giving rewards in the travel category, since consumers weren’t traveling, they added grocery and home improvement stores as major reward categories).

The PNC customer service representative reinstated 60 days worth of lost rewards and issued a statement credit. We don’t want a statement credit because we no longer want to use this credit card, earning rewards that we’ll never be able to capture. If we use this credit card to use up the statement credit, that’s rewards that could be earned on a different credit card. Now Mr. ODA is fighting for the credit to be applied to our checking account or to have a check sent to us (which is the preference on our profile) and fighting for the reinstatement of the rest of the rewards lost.

Without PNC, we’re down to 4 credit cards in our regular rotation. We have 3 cards that we use for categories (gas, grocery, restaurants, travel, home improvement stores), and then we have the Citi Double Cash card that is for “everyday purchases.”

Here’s something different. Medical insurance isn’t something I’m going to pretend I understand fully, but I know enough to protect my money. So here’s two quick stories about how due diligence saved us hundreds.

First, an overview.

When you see a provider (e.g., doctor), they bill your insurance on your behalf. The claim that’s submitted is reviewed by the insurance’s benefits administrator, and any coverage is paid out. Your insurance will likely have a “disallowed” amount (what your insurance deems is too expensive to be billed for the given service), a benefits paid amount (what insurance pays on your behalf), and then a member responsibility amount (what you owe). Once the claim is processed, these are outlined in an explanation of benefits, or an EOB. If and when you receive a bill from the provider, verify against your EOB to ensure that it aligns with your insurance benefits.

Here’s an example of an EOB. By using a provider that is in-network (in a negotiated agreement plan with my insurance company), the doctor and the insurance have agreed costs for services provided. My insurance’s “allowances” are negotiated with each provider who participates in the network. Allowances may be based on a standard reduction or on a negotiated fee schedule. For these allowances, the provider has agreed to accept the negotiated reduction and you are not responsible for this discounted amount. In these instances, the benefit paid plus your coinsurance equals payment in full. So here, for the services that I received, the insurance company is saying, “I see you billed for $115, but we agreed that this service only costs $65.34, so that’s what we’re allowing.” You, as a covered member, are not charged for the ‘disallow’ amount of $49.66.

In our case, we have a high deductible plan, which means we have to spend a certain amount of money on covered services before the insurance pays out benefits. Ours is $3,000. This means that for the first $3,000 worth of doctors visits to in-network providers, we’re paying the total allowed amount (e.g., our son had to go to the ER, and we paid $609 for the visit, which is the fully allowed amount). There are plans out there where you don’t have a deductible, but you have a copay (e.g., I had a plan where I paid a flat $20 for each doctor’s office visit and $125 for each hospital visit, but I was also paying a higher premium for that coverage type). In a future post, I will share how we compared our plan options and chose a high deductible plan.

After we meet the deductible, most of our services are covered at 95% (i.e., we’re responsible for paying 5% of the allowed charges). In the example above, we had to pay 5% of the $65.34, or $3.27.

There are tons of nuances to insurance though, but hopefully this broad overview helps understand how to read the EOB. I have more stories of where my interpretation of the coverage in my brochure doesn’t seem to match the benefits administered, but those are for another time. For now, here’s how we protected hundreds of dollars by staying on top of our coverage.

MR. ODA’S STORY

Speaking of nuances, here’s one of those. Preventative care is covered at 100% (e.g., maternity screenings and annual physical exams). Mr. ODA needed a physical to qualify for his agency’s wellness program (they’re given 3 hours per week to exercise). When he went to get the physical, it got coded as a sports physical because the doctor had to sign off on a paper that said he was healthy enough to participate in the wellness program. A routine annual physical is fully covered by insurance, regardless of deductible. Apparently, a sports physical is not the same concept and regular coverage requirements apply.

Mr. ODA had to call back to explain that the exam was routine with a signature on paper, and not any more in depth to be considered a sports physical. The doctors office offered a reduction in the amount owed, twice, but eventually realized they were spending more in postage and phone calls than the bill was worth while Mr. ODA fought the coding, and they wrote it off.

MRS. ODA’S STORY

I saw a doctor in December 2019 when having pregnancy complications. In February 2020, I received a bill, which I promptly, and erroneously, paid. A few days ago, I received a check for the amount I paid a year and a half ago. So it wasn’t a quick resolution, but I wasn’t going to let $300 go.

The bill said: Charges to Date: $451.00 Payments/Discounts to Date: $157.85 Remaining Patient Balance: $293.15

I had seen multiple doctors in a short period of time, so I was just in auto mode to pay all the medical bills that I had. After I paid it, I realized that on the back of the bill there were more details about that “payments/discounts” line item. There were three columns: Insurance Payments, Patient Payments, and Adjustments to Date. The total $157.85 was in the Adjustments to Date column, and the insurance column said $0. I checked into my insurance claims online and didn’t see this date of service. Well, I’m insured, so this should have been submitted to my insurance for review first. I called the hospital to indicate that there was an error made, and I shouldn’t have paid this in full, even with an “uninsured discount” they graciously offered me.

I called the hospital to ask why this wasn’t submitted to my insurance and discovered that my name was spelled wrong, my insurance was entered wrong, and this claim wasn’t tied to all my other hospital-related claims I had processed. Supposedly, they updated my information and resubmitted. I still didn’t see it on my online claim history after the 30-45 day window they told me, so I called again in April 2020. I was told they would resubmit. Two months later, I was managing a newborn and we were just deciding to move, so this fell off my radar. Then all of our things were in storage for two months. By the time I got this paperwork back out, it was March 2021.

I explained my story to the hospital again and asked for it to be properly submitted. I was again told they would submit the claim, but this time they’d submit by paper handling. Again, nothing showed up in my insurance. I called in April 2021 and was again told that they would try submitting again. This time I escalated to a supervisor. I said that this was unacceptable, and I didn’t want to keep being told they would try again, delaying my reimbursement by another 30-45 days each time I called. The supervisor said she would ensure the paper claim was sent out and call me back in a week. I never got the call. On May 18, I called again, immediately asking for a supervisor. This supervisor said that my account showed a refund was approved, but he needed to issue it (why couldn’t that just have been done?!).

Well, on June 1, I received a check in the mail for $293.15. That’s the amount I paid back in February 2020 for a December 2019 date of service. I could have written this off in my mind a year ago and not made these five or six phone calls, taking about 90 minutes of my time in total. I could have said to myself, “I called. There’s nothing more I can do.” But we wouldn’t be in the position we’re in now with our finances if I kept saying “oh well, that’s all I can do.”

The moral of the story is that you should be an informed consumer. If you know how to determine your benefits and calculate your coverage, you can make sure the proper payments are made to the provider, and that you aren’t overcharged.

This is a good one. This is the one we use when people say “how can you handle all those properties,” and I respond, “if we survived this one tenant, we know we can handle whatever gets thrown at us.” Hoarding, mice, court dates, eviction. But its not always like that. The sun shone down on us for the current tenant though, who signed a two year lease and take care of the house (like, even power washed it on their own accord). The stories below show that you need a thick skin and a smooth temperament to be a landlord. Treat this as a business.

LOAN

This house was purchased ‘as-is,’ but we still had a home inspection contingency in the contract. It was listed at $139,500; we purchased for $137,500 with $2,500 in seller subsidy. We went under contract on 8/14/2017 and closed on 9/22/2017. The appraisal came in at $141,000, so we were content with our decision.

We refinanced the loan in May 2020. Our original loan had a balance of $105,800 at the time of the refinance. We rolled closing costs into the new loan and cashed out $2,000, making our new loan amount be $111,000. The refinance reduced our interest rate from 4..875% to 3.625%, shaving $104.25 off our monthly payment. I went into detail about the refinance in my Refinancing Investment Properties post.

Following the 1% Rule, we would be looking for $1,340 in rent (net of seller subsidy), but we haven’t received that yet. The first tenant’s rent was $1,150 and the second at $1,250. For the third potential tenants, we listed at $1,300, but the new tenants negotiated to $1,280 for a 2-year lease.

TENANT #1: OUR WORST

The application. It’s hard to not give someone a chance when their application is borderline, but I suggest letting the information on the screen speak to their character. Before the official application was run (which includes a background check), she admitted to a felony that she served 2.5 years for, and she filed bankruptcy due to a stolen identity while she was incarcerated. It seemed like she paid her dues and was building a new life. We got her application about two weeks after closing, so it wasn’t like we were desperate to rent it at that point. But she was quick to fill out an application and provide necessary documentation, so we decided to give her a chance. She moved in on 10/1/2017 with her 3 children, one of which was born days after she moved in. Her rent was $1,150.

We didn’t have any unreasonable situations with her in the first year. We did have a maintenance call for a leak under the kitchen sink, and we noted that the house wasn’t tidy. It seemed like she was a coupon-er, where she stocked up on a few items and probably resold them, which supported how she kept wanting to pay us in cash. The house wasn’t to my standard, but I didn’t look close enough to notice that it was dirty in addition to cluttered. I wanted to say something, but didn’t know my place at that point. Hindsight: I should have told my property manager and had her issue a written notice. This won’t matter down the road for legal proceedings, but perhaps we could have saved ourselves some headaches if she took the notice to heart; I was just afraid of offending her. But, other than that small concern at the time, we had no issue renewing her lease for another year.

The tenant complained about seeing a mouse around February 2018. We informed her at that time that pest control was up to her because of her living style that was attracting the pests. She claimed to have a quarterly treatment through Terminex. She complained further of mice in November 2018, but I wasn’t part of that conversation. It appeared to be that she was upset that there were still pest issues while she was paying Terminex. Well, that’s an issue to take up with the pest control company, not us. Our property manager gave her the information to our pest control company and shared that it would be a bit cheaper for the quarterly plan too. We heard nothing more until all hell broke loose in April 2019.

She sent pictures of mice poop all over the house on April 9, claiming that she had been out of the house from March 31 through April 8 and came back to this sudden mouse infestation and would be leaving the house. Well, that’s not how it works. She claims that was her ‘prompt’ notification, as if mice set up camp in a lived-in house that’s well maintained out of nowhere (news flash: it wasn’t well maintained and clean). She claimed that because of the living conditions (that she perpetuated), this would be her last month in the house. We knew we had the lease to fall back on, so we continued to remind her that this wasn’t on us and she couldn’t leave us with the financial burden and walk away. We had our pest control company go to the house as soon as possible, and we received their report on April 12.

But wait! While complaining about the condition of the house (that she caused), she wanted to know if she could buy the house!!!! Logic always seems to abound in these situations; it’s hysterical. We offered her to purchase the house from us at $148,000. She ignored it after that offer.

Both the pest company and our HVAC person noted a dog on the premises, which was in violation of the lease. HVAC was called out to fix a wire on the outdoor HVAC unit that the dog had chewed through. She also wasn’t taking care of the yard, and the City of Richmond was fining houses that violated their weed and grass clauses, which we notified her of on May 9.

She didn’t pay April or May rent, so we had a court date set for May 10. We had told her that she had to pay all overdue rent and late fees for us to cancel the May 10 court date. She didn’t pay, so our property manager went to court. The judge awarded us possession of the property, but since there was such outstanding rent and damages, another court date was set for July 1 to award us the money owed. In front of the judge, the tenant handed the keys over to our property manager, saying she was moved out. Immediately after leaving the court house, the property manager arrived at the house to do a walk through, only to find several people inside. She called the police.

The officer assessed the situation. He said that since they’re still moving things out (and there was a lot to move out), that it was a benefit to us that they were still working on it. He suggested asking their input on when they thought they would be done. One guy said at 3 pm. We agreed to let them stay, and I would go by after work to change the locks.

I showed up at 4 pm to change the locks, only to find people still coming in and out of the house. I called the non-emergency police line and waited for the cops to show up. It’s officially trespassing, and we were prepared to press charges. The officers knocked on the door and asked the people inside (none of whom were the tenant on the lease) to leave. One woman started a whole spiel about how she’s on probation and everything that she’s been arrested for, so she didn’t want to be arrested. The officer was funny to watch, and he just kept saying, “I’m not arresting you. I just want you to leave.”

After they drove away, the officers let me walk the property to ensure everyone was out. The place was destroyed!

By Virginia law, we are required as landlords to make every attempt possible to get the unit re-rented and let the old tenant “off the hook” for unpaid rent. Meaning, we can’t hold them to the entire term of the lease and have a vacant house. Regardless of this, we wanted to get everything fixed and replaced in the house so that we had an exact amount to claim during the July 1 court date.

The linoleum replacement was the critical path. She had destroyed it (looked like some chemical ate through it) beyond repair and it had to be replaced before we could re-rent the house. Home Depot’s timeline was really behind, and they weren’t able to get us scheduled for installation until June 20th (after she had “vacated” May 10th).

I compiled a list of lease violations with my documentation to support the claims in which she violated the lease on top of the obvious (e.g., dog on premises, smoking in the house). We had invoices from the pest company, the HVAC company, the trash removal company (over 40 cubic yards of garbage was left in the house when they finally vacated), and the “hazmat” cleaning company, all corroborating an unclean and unkempt living condition.

We went into court with a claim of $9,250. This was unpaid rent for 3 months, late fees, junk removal, pest control, HVAC fixes, professional cleaning that included a ‘hazmat’ charge, and all our paint and flooring charges.

We won the first judgement in court, simply because the defendant didn’t show up. We were awarded $9,250 plus the court fee and 6% interest. Well, somehow the court accepted her plea of needing another court date after not showing up to this one, and that was on July 10th. The judge that day reduced our rent and late payment owed by one month, and reduced our reimbursement total by a bit more than the security deposit we had already kept, bringing the judgement to about $6,600 plus the court fee and 6% interest.

Per the court process, we were required to work with the ex-tenant to develop a payment plan. We offered her a payment plan via email that was never responded to. From there, the next step is to retain an attorney for wage garnishment.

I contacted the attorney we use to help with wage garnishment, but he wasn’t experienced. He referred me to someone, who let me know that he’s already representing someone who has a claim against her. He said that he could still represent me, but I’d be second in line to any money they get from her. He offered me another attorney’s name to see if that one could help me instead, but that attorney said he couldn’t represent me because he already has another client looking for money from this woman. Interesting that two attorneys had different answers, but we went with that first. We haven’t seen a dime. Once the money was spent and we paid off the credit cards, it wasn’t on our radar anymore. Anything we get from this woman will be a bonus at this point.

TENANT #2: BLISSFULLY UNAWARE OF HOW LIFE WORKS

Two kids just out of college were our tenants that came in after that mess. They were great tenants, but a bit unaware of how the world works. They didn’t get the utilities into their name timely, so we charged them for the bills that came to us. After that, they paid their rent on time, and even when their restaurant jobs shut down at the beginning of the pandemic, they prioritized paying rent over other things they could have spent their limited income on; I was impressed. At the end of their lease, they were a bit lost too. Our lease requires 60 days notice of your intentions – either leave, or renew. Our property manager reached out to them at the 60 day mark, and they said they weren’t sure what they wanted to do, but were looking for other places. Since, realistically, we weren’t going to list the house for rent at 45 or 60 days, we told them that was fine. They came back after a week and said they were going to move out.

We moved forward with listing the house for rent and vetting new tenants. We had our property manager show the house on June 10 for what would be a July 1 lease. About a week later, the current tenants asked if they could stay longer because they didn’t get the place they were looking for. Sorry, but that’s not how it works and it’s already rented. The new tenants were OK with moving in July 15, so we allowed the college guys to stay until July 10. Then we hustled to get the house put back together before the new tenants. Specifically, one of the tenants was an artist, and he hung a huge canvas on one of the bedroom walls to paint on. Well, the paint bled through.

They also didn’t tell us that the range wasn’t working. When we asked about it, they said something to the effect of, “oh yea, we smelled gas, so we just cut it off. That was back in March.” Goodness!! So we quickly ordered a new range. We also had to have the carpets professionally cleaned, which was especially frustrating since they were only a year old. Luckily, the ladies who came to clean the carpets worked their magic, and they came out looking good as new. The microwave handle was broken off, and when we looked to buy a replacement, it was essentially the same cost as a new microwave, so we installed a new one.

While we were working in the house, we noticed that the air conditioner wasn’t keeping the house cool. We had an HVAC tech come out to the house, and it was either $1,400 to repair (after we had already previously put money into the HVAC unit), or $5,000 to replace it. We decided to replace it after it died shortly after the third tenants moved in.

TENANT #3: SOME OF THE BEST

These tenants have been wonderful. They’re both pharmacists at the local college and have been very self-sufficient. They’re great about alerting us of issues, but not in a way that it seems like they’re nitpicking. For instance, they wanted to store their lawn mower and other things in the shed out back, but the handle was broken off it. We told them that if they wanted to purchase a replacement, we would reimburse for the cost. Then they noted that the closet dowel was broken and they replaced it. I told them I would pay for that, so just take it off the next month’s rent. When they sent me the receipt, they had only taken the rod itself off the rent, but not the brackets to hang the rod. I immediately sent them the rest of the cost!

They’re one year into a two-year lease, and we’re very happy with them. They always pay their rent on time, they communicate regularly, and they’re taking care of the house.

MAINTENANCE AND REPAIRS

Since I’ve covered a great deal of the repairs we’ve managed in this house through each of the tenant stories, here’s a quick summary of other items.

Shortly after the third tenants moved in, they politely let us know that their dishwasher wasn’t cleaning the dishes. They very clearly identified the problem and the steps they had already taken to attempt to fix it, but it wasn’t working. We purchased a new dishwasher the day after they let us know. So in the matter of a month, we replaced the built in microwave, range, dishwasher, and HVAC. The only appliance we haven’t replaced in this house now is the refrigerator.

There was an electrical issue that we had sort of noticed before, but hadn’t pinpointed it without having things to plug into all the outlets. We had an electrician go out and fix the switches and outlets that weren’t working in master bedroom.

AN OVERALL LOOK AT THIS HOUSE AS AN INVESTMENT

Remember how real estate investing provides multiple avenues for wealth building? Here’s how they’re looking for this property.

Cash Flow – As we have had to replace nearly all appliances, including HVAC, and all the flooring among several other smaller issues, our total cash flow on this property is nearly nothing. But, like mentioned before, we shouldn’t have any big purchases coming and will start to be able to pocket the profits on this house once again.

Mortgage pay-down – The tenants have paid our mortgage for us, but due to closing costs of refinancing and choosing to take $2,000 cash back from that refi, our principal is actually higher than when we bought it.

Tax Advantages – We always depreciate the cost of the structure for paper losses that help offset profit on properties for tax purposes. All those repairs and appliance replacement expenses that eat into the profit margins are written off. So come April 15, the silver linings of those expenses are realized.

Appreciation – This one is good for us. This house is in a developing neighborhood and the area around it is being revitalized. Coupled with standard appreciation and the *hot* real estate market we’re in now, the value of the house is 150% of what it was when we bought, in less than 4 years.

SUMMARY

We’ve put about $10,000 into this house at this point. But that means we have a lot of brand new things in it. Now isn’t the time to give up on the house, since we should be in a position to not deal with many maintenance requests. Rent continues to climb, increasing our cash flow, while we just brought our mortgage payment quite low with the refi, and the property will continue to appreciate in value.

We learned a lot about the eviction process, even dealing with local police officers in the process. The court system and law enforcement are fairly simple to work with, as long as you are a fair and respectful landlord, keep documentation, and follow landlord-tenant laws. When the tenant doesn’t live up to their end of the bargain, justice will be served.

Spring is a time for lease renewals or preparing to re-rent a house.

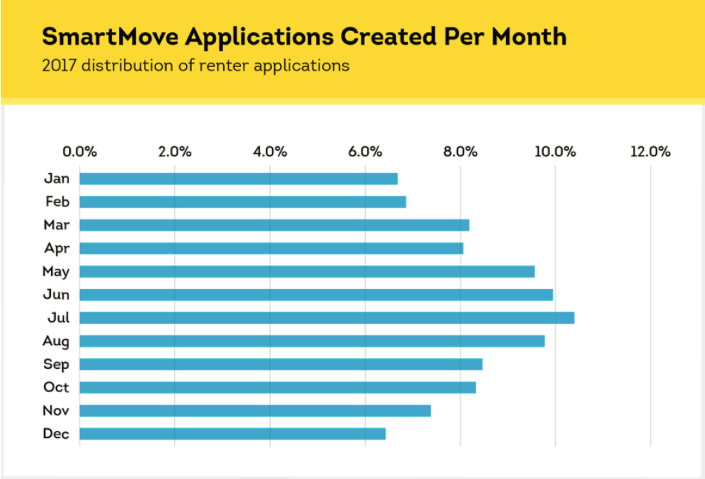

Spring and Summer are times when people are most active in the real estate market. It’s the best time to be listing your house for sale and for rent, which may yield you a better sale/rent amount because of greater competition. This timeframe is likely most active because of the better weather for moving and the school year – if a family is looking to move, they’re more likely to do it when they don’t have to transfer their kids to a different school district mid-school-year. Personally, when I was in college, nearly all the rentals were available in May or June. I remember being frustrated that I couldn’t get an August lease and had to pay for the summer months even though I’d be back living at my parents’ house. Now that I’m older and have more experience, it all makes sense. Below, you can see the increase in applications processed by SmartMove (the way we process tenant applications) that occur during the summer months, which indicates the most active time in the market.

We have seen this reflected in our days-on-the-market and rent prices. When we can list a house in the Spring months, we’re able to get it rented with very few days vacant. Houses that we’ve closed on at the end of the Summer (when school starts) and in the Fall have taken us more time to find a tenant, and we’ve had to reduce our asking monthly rent amount.

For those houses that we had purchased in a less-opportune time of year, we’ve worked to get them back to a Spring-time market for renewal.

We purchased two in September 2019 that we weren’t able to get rented until November 1st that year; we offered those tenants an 18 month lease so that their lease expiration would become May 31st.

We did similar with a house that we purchased in August. After that first year, a prospective tenant tried negotiating the list price for rent, and we said we were willing to reduce the rent a bit for an 18 month lease; they agreed, and we got our rental on a Spring renewal.

We recently had a tenant break their lease (with our concurrence), so that house has a lease expiration of October 31st now. We intend to offer a 6 month lease term to that tenant when the time comes.

With that said, we have lots of activity at this time of year.

We have 9 houses in Virginia and 3 in Kentucky. These markets are so different for us. We do our best to work with our tenants to encourage them to continue renting with us. I wrote about this in detail in my Tenant Satisfaction post.

Here’s a break down of how we handled all the leases that are expiring at this time of year.

In Kentucky, one lease was set to expire at the end of April and another at the end of May. These two properties are under a property manager. She attempted to increase the rent for a new lease term, but the tenants pushed back. Landlords don’t have a lot of leverage in a pandemic. Since the property manager is the one who handled the communication, I don’ t know what the details were. We believe both these houses are rented for less than market value, so that’s unfortunate. But, we’re grateful that both tenants renewed their lease for a year, so we don’t have to work to turnover the houses. Within reason, we’d always rather rent for a few bucks under market value than to handle turnover and lost rent (vacancy) by trying to maximize monthly cash flow.

In Virginia, we have an array of situations. Richmond was quick to acknowledge the property value increases that have occurred over the last year or so. This means that they increased our assessments, which effectively increases our property taxes.

We have the first two properties that we bought in that market, which are next door to each other and both have long term tenants (one since we before we purchased it, and the other is the second tenant who moved in a year after we purchased). We inherited their rent at $1,050, and then we increased it to $1,100 two years ago. With the property assessment increases, it was time to raise their rent again for this July. I initiated a letter to each of them stating the rent will increase as of July 1, which gave two options: they could leave the property by June 30th in accordance with their lease, or they could sign on for another year at the increased rent rate. Both chose to stay in the property, and they signed another year at $1,150. This is still below market value for the houses, but we’re happy with the lack of maintenance needs in these houses over the last 5 years. We’re in the middle of replacing the flooring in one of the houses. That house has a family of 5 and a dog living in it, so it’s not surprising that it’s worn out faster than the identical one next door with one person in it.

We have a 2 bed, 1 bath house that rents at $795. She’s been in the house since July 2018, which means that her lease ends June 30th of this year. Based on the 1% Rule (i.e., we’re looking for the monthly rent to be 1% of the original purchase price) for this house, our rent goal is $635. Since we’ve exceeded that goal for the life of our ownership, and the house hasn’t cost us much in maintenance, we chose to not increase her rent if she wanted to renew for another year, which she did. She has also spent some of her own money to spruce up the house and make it her home, and we recognize the value to us that her efforts also bring.

Another house reached out to us and asked if we were willing to renew her lease for another year. She’s been there since we purchased the house in 2017, and we’ve never increased her rent. She usually pays rent early and doesn’t ask for anything. The 1% Rule puts us at $660, and we’ve been collecting $850. Since we’ve been lenient on rent increases, I thought it a good idea to re-evaluate her terms. I plugged all the numbers into Mr. ODA’s calculation sheet to see how we were doing since the taxes increased so much on this house. Our cash-on-cash return (which we aim to be at 8-10%) came back at 19.8%. A rent increase for the sake of increasing rent isn’t worth it for such a good tenant, so we agreed to renew her lease for another year at the same rent. She wrote back: “omg thanks so much for the good news!” Happy tenants = good tenants, remember?

As for the others that I haven’t mentioned:

Two of our houses were put under a two year lease last year, so they didn’t require any action from us this year.

We have another house in KY that has a lease ending 7/31 and is under a property manager. We’ll offer a renewal option for them (i.e., we’re not interested in asking them to leave), but we haven’t worked out those details yet. Since we’re very hands off for our KY houses, we don’t know the satisfaction level of those tenants to gauge. Historically, we’ve had trouble renting this unit, costing us long vacancy times, so if we can renew their lease for even the same rent, we’re happy. Plus, having a 7/31 end date starts pushing us closer to the Fall for any future year-long rental agreements.

One of the houses that we have with a partner has a difficult tenant. I mention the tenants almost every month in the financial updates because they don’t pay their rent on time, and getting information out of them is like pulling teeth. They’ve rented there long before we owned the property, and their rent has always been $1,300, which is well below market value. We plan on offering them a drastic rent increase and a new lease term (we’re still managing under the previous owner’s lease agreement) in July for their September 30th expiration term.

While we don’t have any houses to turn over, we’re going to get into each house this summer. Since so many of our houses don’t typically have turnover, we don’t get into them as often as we should to make sure things are running correctly (i.e., don’t want small issues to go unnoticed and cost us in the long run). Specifically, we need to make sure that the HVAC filters have all been changed and verify there aren’t any red flags. I plan to give the tenants at least a month’s notice before we enter, so that if there are any maintenance activities they should have been performing, they have time to get it situated. I’ll walk through with our typical move in/out inspection form and note any concerns or areas of interest. I also understand that by being visible, I’m opening myself up to being asked for things that a tenant may not necessarily ask for via email or text, but I’ll cross that bridge when I come to it. For now, we’re just grateful that we have no houses to turn over and no expected loss of rental income for the year thus far!

I left my career exactly two years ago (on the 8th). My son was 8 months old. Honestly, I could have left my job years prior thanks to what my husband set up for us, but without kids, there was nothing to fill my time. I enjoyed my work a lot, so every day worked was another day of money ‘saved.’ I now have two kids and haven’t looked back. I’ve ‘retired,’ but I haven’t stopped producing some income in addition to managing our finances (although I managed the finances while employed full time also).

First, some background of my career.

When I first started working, I was very driven. My goal was CFO by my early 30s. That seemed crazy, until our CFO stepped in shortly after I started working there, and she was 32. Goal marked. I was on the General Schedule pay for the Federal government. I started as an intern in 2007 (GS-4) and joined the training program (GS-7) that gave you a salary increase every year (with acceptable performance) until your position’s max (GS-12 by 2011). I needed to devise a plan that got me to a GS-15 as fast as possible because in 2011 I was 25 years old, which meant I had 5-7 years to climb 3 grades (which takes at least one year in each grade). Not a lot of wiggle room. Well, I soon realized that there was more to life than climbing the ladder as quickly as possible.

I met my husband at work, and we ended up moving to DC for personal reasons and took a GS-12/13 (this means that I started the position as a GS-12, and after 52 weeks ‘in grade’ with acceptable performance, I was promoted to the GS-13 – in theory, not practice). I was warned that it would be an uphill battle to go from the 12 to the 13, and it wouldn’t be as easy and automatic as it had been to get to the GS-12. Commence years of frustration and extremely poor communication from my leadership on expectations. Without getting the promotion within my position, I applied for another position within the same office, and I got it. This was a GS-13/14. I never got the 14.

My experience within the CFO’s office was so hard on my psyche, and I felt that being a young female, rather than my excellent experience, production, and reputation, were playing into the decision making by my leadership to not promote me. I left and went “back into the field” instead. That position was a GS-13 with no promotion potential within that role. By that time, it didn’t matter to me. I didn’t want any more responsibility than what I had; I enjoyed the work I was doing.

My experience in the CFO’s office taught me that I preferred to be at home with my family and experiencing those things. Before my relationship with my husband, I didn’t realize how much I wanted to spend time outside of work traveling, playing sports, and being with my family.

MY LAST DAYS

When my son was born, I took 14 weeks off work (using my own built up leave since at the time the government didn’t provide maternity leave). The typical 12 weeks got me to just before Thanksgiving, and then I worked one or two days per week until after Thanksgiving. The goal was to work and burn my leave to zero before quitting instead of being paid out on it. If you’re paid out on it, then the tax bill hits hard and all at once. Plus, by burning the leave while still employed, I gained even more time off to burn during those pay periods, more 401k (TSP) matches, and added a few months to my back end pension calculation.

Based on my leave balance, being responsive at work, and managing child care, we first set a goal of January. Then, my husband pointed out that January and February had holidays, and I should try to work through those holidays to get those ‘free’ days off. The goal became March because March is long and without any holiday time off! Well, the Federal government shut down that winter for several weeks. My husband’s job was affected by the furlough, but my type of position was funded through a different mechanism that meant my agency still worked (and if you want a lot of detail on that, I’m always happy to talk about it, but I won’t bore the majority here 🙂 ). So I worked full-time while he stayed home with our son. This meant I wasn’t using my leave, so I could work the part-time schedule longer once he went back to work. We then set my goal for May. I probably could have made it longer, but I was afraid that if I got near Memorial Day, he’d say “work through that holiday,” and then 4th of July wasn’t too far away, so I forced my last day to fit.

I had a such a good reputation for the work that I did, that I still get asked questions by friends I made in the position. Plus, I help my husband get through some work things here and there since his position is similar to one I used to hold. I miss the work, but I don’t miss the office politics and red tape, so I’ll take these random questions from friends!

WHAT AM I DOING IN RETIREMENT

There are days that I miss the work I did. I certainly appreciate the flexibility we have now.

FLEXIBILITIES & MOBILITY

We had the opportunity for my husband to work in KY for the summer after I quit. We were able to capitalize on the per diem given for living away from your duty station, and my son was able to spend time with his cousins. I also learned to be extra grateful for our normal-sized house and that I wasn’t trying to live in a one-bedroom apartment for very long.

Since my husband’s job required fairly frequent travel, my son and I were able to join him for those work trips. We went to Orlando and Glacier National Park together! We also took several trips just for fun, like to the Braves Spring Training games.

Pandemic life made us realize that we wanted to be closer to family earlier than we had intended. We loved our neighborhood, and the schools were going to be great, but having to isolate from people for so long was hard. It was also a logistical nightmare to get things done sometimes without family to help watch the kid(s) in a pinch. Since I’m not working, we decided to move to KY to be near Mr. ODA’s family – a lot earlier in life than we had intended. We discussed the possibility in May, discussed it more seriously in June, had our house listed in August, and closed on it in September. Nothing like a hasty decision with a newborn and no house lined up to move into on the other end of this decision! But had we both been working and both needing to be employed once we moved, we wouldn’t have been able to make such a move as quickly as we did. You can read more about these decisions in my ‘Moving States’ series posted recently.

It’s been nice to be able to do activities with the kids during the week when things are less crowded. Sure, a pandemic limited our options for the last year, but we still have more freedom. I enjoy seeing all the things they learn in a day. There are hard days where I crave more adult conversation or the ability to sit quietly and get something done without being asked for the 90th snack of the day, but I still wouldn’t go back to work.

WORKING

I’m the type of person that wishes I knew the inner workings of so many things and have a strong desire for efficiency. When I took my first job in DC, I kept pushing that I wanted to bridge the ‘headquarters’ and ‘field’ communication gap. For instance, there was a process that the field would submit to headquarters for action. Headquarters had their own internal process of tracking and executing it, but the field didn’t know that process. Therefore, headquarters spent a lot of time answering “what’s the status of my request” type emails. I explained the process to the field, and then we were left to spend more time processing the actions than managing questions.

All this to say: I’m quick to jump at new opportunities where I’ll learn something. I like knowing the process for things and find these details help me better connect with other people. While not being employed full time, I’ve kept my eye open for short term and part time opportunities to do something different.

ENUMERATOR

In February 2020, before the pandemic started, I applied to work for the US Census. We don’t “need” the money, but it gave me something to do that’s different. The application said Census field work was expected to be conducted in April and May. This was going to be hard since my daughter was due at the beginning of April, but I figured I wanted to be in the mix for information instead of assuming I wouldn’t be physically able to do work. Well, the pandemic delayed everything. I didn’t get any information until June, went to training, and then started work in July.

I was able to set my schedule in advance, which was nice. I learned at the beginning that it was hard for me to manage pumping and for my husband getting our daughter down for naps. So I changed my future schedules to be in 2-3 hour segments so that I could go home to feed her and put her down for her next nap. I was given a cell phone that had my work assignments (addresses to collect census data) and my day’s hours. I went door to door trying to gather census data from addresses that hadn’t responded. Most people didn’t answer their door, which meant that I probably had to knock on neighbors’ doors until I could identify at least the number of people who lived at the address in question. That was probably the hardest part because I would introduce myself and immediately be met with “I filled mine out!”

The work was in my geographic area. The furthest I had to travel for my assignments was 25 minutes. We ended up moving out of the area in September, so I missed several opportunities to work more, but most of the work was dwindling by then (the work started to send us further and further from our ‘home base’… even an ability to go to other states).

Honestly, I wanted to be the number crunchers in the office, but that position wasn’t available. I thought if I started with the field work, I could get my foot in the door. Our move hindered that a bit, but I’m glad I did it. I learned how the Census gets tracked. I made some money. I have some good stories (encountered several types of animals, including being surrounded by two large dogs that got my adrenaline running; left a few houses because my gut said it wasn’t safe). The application used to track information needed help, as it assumed we were all working in cities, whereas I was usually out in the country (e.g., no close neighbors). I boosted my confidence with glowing remarks from my supervisor since I put more than bare minimum effort in and was efficient in getting the work done.

the giant dogs that circled me, but eventually let me back in my car

SEASONAL CHANGE RUNNER

A local race track had thought that a limited number of patrons would require less staff. Unfortunately, once the race meet started, they were surprised at where their deficiencies were. Less patrons doesn’t necessarily mean less activity at concessions and bars, for example. Mr. ODA and I were approached about an opportunity to fill this gap. We’d have to be ok being on our feet for 6-8 hours, pass a background check, and pass a COVID test (interest fact: this is my only COVID test I’ve taken).

The race meet is only 15 days. We were approached after the races had started. We needed a COVID test, but didn’t want to pay out of pocket for it, so we had to wait until the next Wednesday to get that. Between all these factors, we were left with only a few days that they needed help. One of those days, we already had plans to attend the meet as patrons, so we didn’t want to lose that ticket. Mr. ODA worked one day of the meet, while I worked 3. I then also picked up a shift for their Derby celebration (although it’s not where the Derby was held).

We had a security guard escort and walked between all the bars and concession stands making change. Patrons tend to start their day with large bills, so the cashiers need smaller bills changed out. That’s where we came in. On the first day, I walked over 26k steps – while wearing ballet flats. My feet and calves weren’t happy about it.

It was an interesting experience. I enjoyed watching the transactions that took place, and the time passed quickly. We didn’t even know what our hourly rate was until our first pay checks, but we thought it was something new and different, so we jumped at the opportunity.

BREASTMILK DONATION

I’ve breastfed both my children. For my first, I worked while he was 3-8 months old, so I needed to pump to leave him with someone else. I learned that I produced a healthy amount of milk and looked into donation methods. A friend of mine had donated milk to a milk bank that works with NICU babies, so I explored that option. I went through their rigorous approval process and took their oath on health standards. I donated over 1200 ounces to the bank that first time. They weigh the milk upon arrival, and I was paid $1 per ounce weighed.

It was a lot of work, don’t get me wrong. I agreed up front to provide 350 ounces per month for 4 months. I didn’t hit that mark. It was mostly to my lack of knowledge on how to freeze the milk so that it took up the least amount of space when packing a cooler. They also had a requirement that not more than 6 ounces gets put in a single milk bag, so that added up. I struggled with their packing mechanism; no matter how many of their videos and attempts I made, I couldn’t seem to get 350 ounces in one cooler. It’s nerve wracking when you’re trying to get frozen milk from a freezer to a cooler while it’s 80 degrees outside (garage freezer), and you feel like you only have one shot to do it right or you jeopardize your entire stash from arriving frozen and being worth all that time and effort. I digress.