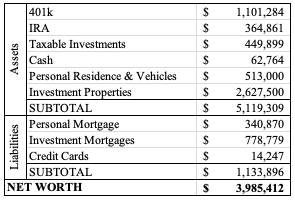

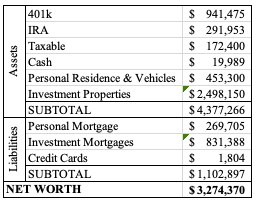

We’re just going to cut to the chase – $4 million net worth! I mentioned that this was a goal for this year. Unlike other years worth of large jumps because of purchasing houses, this was less in our control (granted, our market allocation decisions are what’s driving it…. and by “our,” I absolutely mean only Mr. ODA’s because I don’t do anything in that realm).

RENTALS

Well, we’ve had a quiet month. What’s going to be funny is, I’m going to list the things that we did. Quiet doesn’t mean silent or without effort, but we’ve had a rough go of it over the last year, so this was a welcomed break.

We had termites at a property. We pay $98 annually for their termite warranty program, since we found extensive termite damage and live termites when we bought the house. We’ve had to treat the house several times, so this $98 is a steal. However, I’m wondering why we keep needing to treat the house.

We paid $125 for a plumber to go out to a clogged sink. When we received the invoice, it was for 2 plumbers to go. Between the phone call that they were on their way and the tenant saying they were great, only 35 minutes had elapsed. The company charged us almost $300. Mr. ODA called to ask why they choose to send two plumbers to do a one-man job, while also charging us for it. The owner said it was for liability purposes, which Mr. ODA fought back on. They agreed to a reduced rate, but we were only charged $125, which was less than agreed upon.

We had our third tenant move in, after we unexpectedly had to turnover three houses in the middle of winter. We also were given notice by another tenant that she’s vacating by the end of March. We handled increases for two houses (one handled by a property manager to increase $50/month, and one handled by me to increase by $25/month).

We had one tenant pay on the morning of the 6th with no communication, so I did have our property manager let them know that’s not going to be ok. We also had a usual suspect pay late, with the late fee. However, their communication was frustrating. They said they’d pay on the 6th. At the end of the 6th, they said the money hadn’t cleared like they expected. No communication on the 7th. I asked for an updated on the morning of the 8th, and they said it would be that day. At 11 pm, I hadn’t received anything and reached out. I was then told that money was going into the ATM right then so that she could pay. Sometimes I wish I could do a deep dive into tenant finances so that I could help them out.

PERSONAL

Mr. ODA has a trip in July where a group of guys will hike in the Rockies. Our family is going out before that trip is scheduled to do our own exploring. We booked 4 round trip plane tickets, and Mr. ODA handled the lodging booking for the guys’ portion. That’s almost $3,000 worth of purchases, so our credit cards are higher than usual.

Speaking of the plane tickets. We purchased gift cards from Costco for Southwest. The gift cards are essentially $450 for $500 worth of purchasing power at Southwest. We bought two, therefore saving $100 on the tickets. For an extra few clicks on the computer, and the 15 minutes waiting time before the e-gift cards were delivered to my email, that’s $100 that can be used somewhere else.

We bought a new vanity for our bathroom. That was about $700 for the vanity, faucet, toilet flusher, and mirror. I sold the old vanity (in rough shape) for $30. And because I’m proud that I did most of it on my own, here’s a picture. I needed Mr. ODA’s help with the supply lines because I lost patience with how tightly they were screwed on and my lack of progress. I cut the baseboards down to size, except I somehow measured wrong on one quarter round cut (I was cutting while it was on the wall). Mr. ODA cut and installed the replacement piece for me.

We finished up the ski season. The kids did great. I was really proud of them for sticking with it. We used our season pass well (i.e., exceeding the cost had we bought individual tickets for each visit). I took two of the three kids to the aquarium, and we took the baby for a procedure at a local children’s hospital. We’ve started tee ball for our oldest. Our March is very full and busy, so we’re getting into the swing of things and keeping track of the schedule.

NET WORTH

Well, we far exceeded that $4 million goal. The market went up big, with our biggest changes being in our retirement account, IRAs, and cash. Our cash increase is offset by the lower amount in our Treasury account. Some of the short term bonds were transferred back into our savings account, and we’ve kept that money in savings since our deck replacement is slated to begin.

The rentals were expensive this month with $4600 paid out. This doesn’t include work that’s currently under way, but not paid for yet.

I paid for a water heater replacement, which was $1,904. I had to pay insurance on a larger property ($793). I paid the balance of the window replacement at one property, which was $1,064. I also paid for a plumber to address a leaking toilet and a rotted faucet ($325). We had a new tenant move into a vacant property, so we had that cleaned before her arrival ($165).

I had to pay for a plumber’s service call ($95) for clogged drains, for them to refer me to a rooter company ($250). I emailed that tenant that preventive measures need to be taken because I’ve not had so many calls to one property. She assured me they have taken appropriate measures and it’s just old pipes. The only problem being that we have several other properties with old pipes that never call for clogs.

We’ve turned over two properties and are about to turnover another property in the dead of winter. It’s so frustrating to be in such a position. All of those stories will be elaborated on in future posts. – On one property, we charged a lease break fee of one month’s rent to cover our losses (the fee was different based on the month in which they broke the lease). Luckily, that covered our entire month of January being vacant, but we found someone for 2/1. – Another tenant asked to leave a property because he lost his job. That was handled a bit different because we didn’t know in advance that this tenant would want to leave mid-lease. We told them there’s a fee of $250 (which is what it costs us to pay the property manager to find a new tenant), and that they had to pay rent until we found a new tenant. We didn’t lose any rent on that property. – Now, we have a newly vacant property because the tenant can no longer afford it. I’m not expecting to recover her unpaid rent at this point. We approved a tenant to start 2/28, leaving us with 27 days of lost rent. However, we sent a lease over for them to sign. They’re currently dragging their feet on signing because they want to pay with their tax return. I don’t love that idea. They’ve been easy to communicate with up until this point, just slow. I’m hoping this gamble works out.

PERSONAL FINANCES

I had to transfer money to Mr. ODA’s account to cover the purchase of our new back door and a new treadmill (although that was only $400). This is an interesting concept for us. Mr. ODA had an account before we met. His account was grandfathered in to new terms and conditions at this bank. He’s kept his checking account and credit card for the rewards (I have access to the account; my name just isn’t on it). Any online purchases go on that credit card. However, that account only receives $250 every other week from Mr. ODA’s pay check (occasionally it’ll receive rent via Zelle). So sometimes, we need to transfer money from our main checking account to cover that credit card payment. All our security deposit accounts are with that bank too. So I had to then transfer from a security deposit account into his checking account, and then have him send that money to our main account. It wasn’t our finest money management moment.

Not much else happened this past month. We’ve gone skiing with the kids some more, I went on a moms’ cruise (which was amazing), took a small trip to piggyback Mr. ODA’s work trip, and have done activities around town. We’re gearing up for a procedure at a local children’s hospital next week, which I’m expecting will wipe out our deductible. Luckily that’s only $3,000, but I’m sure we’ll hit it. We’ll actually be late hitting it this year; it’s usually done in January.

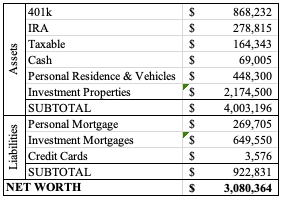

NET WORTH

One of this year’s goal is to hit $4 million net worth. I thought it was going to be a ways away, but the market has been up big recently. We’re only about $14k away from that goal now!

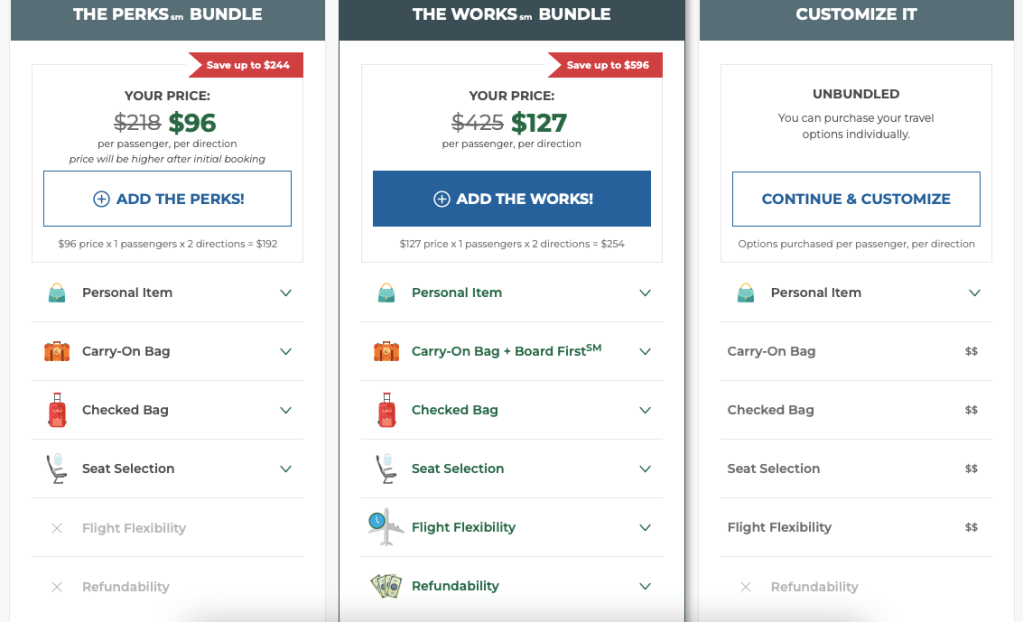

I recently went on a trip. We booked one of those “cheap” airlines, where you pay a la carte. Our round trip flight was about $50. In the process, I was amazed at the number of people who were frustrated by the rules, as if you don’t have ample opportunity to learn the rules in the process. So I wanted to go through a booking, to show you that there are plenty of warnings, and that it may or may not be cheapest to go this route.

I’m going to pretend to book a flight. From Cincinnati to Orlando, round trip, I found a flight for $87.96. The next page asks for my personal information. They then offer me a few options.

The price highlighted is for one way, and in smaller font, it indicates the round trip price. This could be a bit more straight forward, since my selection is for a round trip flight, so one way worth of baggage isn’t the expectation. I decide to ‘continue and customize.’ The next page is seat selection.

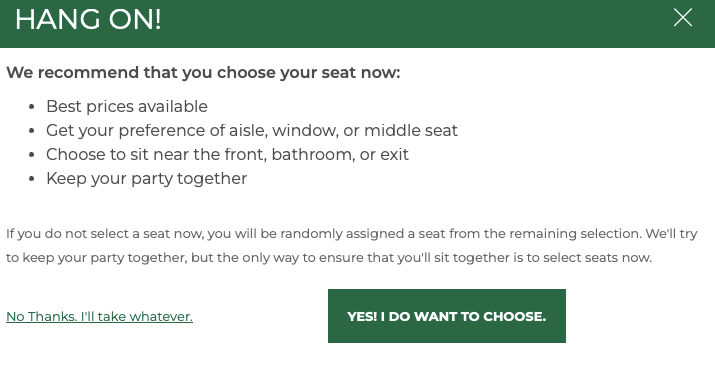

Every single seat has a price associated with it. Again, this could be more straight forward. Nowhere on the page does it clearly indicate that you don’t have to pick a seat. I click “continue.” There is a link below continue that says “what if I don’t pick,” but I didn’t check that. The next page causes me to pause and lets me know I should rethink my options.

I select no thanks. The next page provides my carry on and checked bag costs. I can select that I want to carry on and board first, just carry on, or have no carry on. I select no carry on and no checked bag. As I scroll down, it lets me know that I can have a personal item for free, and it lets me know the size restriction for this personal item. It tells me multiple times on this page that bags will be more expensive at the airport.

I click continue, without selecting any baggage, and it halts me again.

I then get asked a few questions about the check in process and any other add-ons. I decline everything, and I’m sent to the payment page. At the end of the page, I have to agree to several things, including baggage requirements, before booking.

The entire point here is that this airline has warned the consumer several times, through multiple pages and “clicks” that there are fees outside of the ticket price. So even if you didn’t know that the reason you found such cheap flights was because their pricing is a la carte, they’ve told you multiple times through the booking process. Similarly, you know going in, on any airline, that a bag over 40 or 50 lbs is going to be considered overweight.

It was frustrating to watch so many people get mad that they checked your bag size as you boarded the plane. You signed up for that. You could have checked the size. I read the wrong section when I packed my bag, so I had verified it as a carry-on size, which I didn’t pay for. I was able to move things around in my bag for it to be able to fit. If it didn’t fit, I knew that mistake was on me, and I’d pay the fee. The fee in the airport was $99. Yes, it seems astronomical to pay that fee for something that you can walk on with if you’re flying Delta or American, but it’s the rules for this airline, and I know that going in. I could have adjusted things for the flight home, so my total for this roundtrip would have been $150, still cheaper than roundtrips on other airlines.

For the pretend flight I went through above, if I had selected The Perks bundle, my total would have been $279. I’d get a carry on, checked bag, and the ability to select my seat at that price. Had I selected just a carryon each direction, my total would have been about $225. For the same dates, I could fly more inconvenient schedules (e.g., midnight arrival) for $209 through American.

When comparing the prices, you need to see what the best options are for what you need. If you can’t get by with just a personal item, then you need to factor that into the flight cost when comparing to other airlines. If you can’t handle the psyche of having your bag checked for size when you board the plane, then stick with the traditional airlines.

Be an informed traveler. Know the fees associated with your airline. Know the restrictions for each item. Plan in advance instead of having to move things around at the airport where you’re going to feel the stress.

We went on a trip to Indianapolis last month. We did more activities than we typically would have, so our spending was more than average.

The reason behind the trip was the Children’s Museum. We like visiting zoos around the country, so we used that to fill our other day there. The zoo was $91 for entry for 2 adults and 2 children, while our youngest was free. We had to pay for parking, bought lunch at the cafeteria, two kids rode the carousel, and we all rode the train; that came to $66.70 spent the day of our visit. The Children’s Museum was $90 for entry for the same group of us. It also had a carousel that we let the kids ride, I let them get a flattened penny (they used “their” $1 for it), and we bought lunch (parking in a parking garage was free); that came to an additional $35.88 spent on that day. The zoo’s meals were very reasonably priced, but the Children’s Museum’s meals were ridiculously expensive, so that free parking wasn’t exactly free.

We placed a grocery pick up order when we arrived, and that covered our breakfasts and dinners ($39.10, but we didn’t even use everything we purchased, so that’s inflated). We stopped at McDonald’s on the way there and as we left the city on the last day ($17.68). McDonald’s and Qdoba are sure fire ways to get our kids to eat and eat quickly, so they’re nice when we’re on the road.

On the first day, we went exploring the city. We had to pay to park in a parking garage, which was $5. On the last day, we did a Capitol tour and visited another museum (both of which were free), but we had to pay to park twice ($2.50).

We had booked an AirBnB for the trip. A series of events I won’t get into meant that we received a full refund from the originally booked location, had a coupon code for our inconvenience, and booked a new location right away. We ended up spending $574.32 for our lodging of 3 nights. We specifically didn’t book the cheapest place available because we wanted the comfort of multiple bedrooms for the kids. The two oldest can sleep together, but the youngest needs his own space so that it can be without a night light. We could have managed with two bedrooms because the youngest slept in the master closet, but I can never guarantee that there’s a closet big enough for a pack and play. This place had 4 bedrooms, but we didn’t use one of them. We also wanted a hot tub available, so Mr. ODA and I could hang out and watch tv after the kids went to bed. It’s an amenity we’ve grown fond of, and we even plan to purchase one for ourselves if our deck ever gets replaced.

In total, this trip cost us $922.18 (plus gas) for 3 nights away. This is a higher than normal 3-night trip for us, but we were ok with it since we hadn’t taken our usual amount of trips (newborn life). We could have planned ahead on our two big days to pack a lunch instead of buying there, but we chose the convenience of purchasing the meals over the potential savings, especially knowing that we weren’t spending anything outside the normal realm for our breakfasts (cereal) and dinners (easy, quick pasta meals). Although this wasn’t known at the time of booking, but it was once we started the activities, the concession from AirBnB more than covered our meals and extra activities on each day.

Our kids are 5, 3, and 10 months. The Children’s Museum was great for their ages. There were some exhibits for older kids that we bypassed. I thought the St Louis Science Museum was better at having interactive exhibits throughout (and is free!), but it didn’t mean that this place was bad. The zoo was nice too. There’s a lot of shade, which was appreciated on a very hot day, even in October. It felt smaller than the Cincinnati Zoo, which is where we usually go, but it was clean and the animal exhibits were nice. They had a lot of shows and “ranger talks” included with your admission too. There was a dolphin show that was included with admission that was significantly more than I would have ever expected as a free attraction!

The city of Indianapolis wasn’t great. We didn’t encounter a really nice area of the city; most of it is run down, and there was a lot of homeless downtown. It’s clear that there is a lot of updating underway, and that it’ll probably be a really cool place in a few years. I never felt unsafe, but it was noteworthy that we haven’t visited a city like this since Detroit (although we did find a nice place there, ironically).

All in all, we spent less than we originally projected. A 3 night trip where we were sufficiently entertained, but not overly exhausted (the kids got to bed on time!) for under $1000 was great.

I manage all our income and expenses (at a high level, like credit card payments, not individual line items). I have a spreadsheet that I set up in 2012 and have used religiously since then. I’ve shared how I set it up in the past, but we’ve entered a new phase that makes my spreadsheet even more important to me.

BACKGROUND

FIRE. Financial Independence, Retire Early. This isn’t a post about FIRE specifically, although it’s the movement that sparked Mr. ODA to go down our financial path.

The purpose of our rental portfolio was always for both Mr. ODA and I to quit working. We had covered my income before any kids were born, but I kept working because there was no reason to not be working. Once our son was born, I took 14 weeks maternity leave (not a separate bucket for Federal employees back in 2018; it came out of my own accumulated sick leave), then I worked about every other day for 8 months while Mr. ODA and I swapped child care roles, and I burned down my leave.

While we don’t plan to work full time, we do plan on keeping part time positions. We’ll work on things that bring us joy, rather than an office job with office politics. Since I stopped working, I’ve done odd jobs, part time. For example, I worked as a census taker and served beer at a local race track over the last 4 years. These were all seasonal, part time positions, with no long term commitment.

Now that I quit working, it’s Mr. ODA’s turn. We hardly skipped a beat when we left my six-figure salary behind (although a pandemic probably helped curtail spending on our behalf!). However, the thought of losing his salary as a safety net and losing insurance are two items that have caused some pause.

THE SPREADSHEET

For you to understand my panic that I’ll get into here, I thought a quick reminder was necessary. This is how I manage our money. It’s nothing fancy, but it works. I don’t miss payments. I can allocate expenses to a specific 2-week period against what income is brought in at that time.

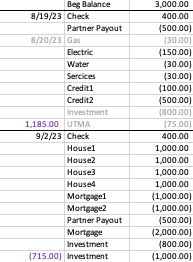

There are two parts to the spreadsheet. Well, there are about 10 tabs, but this first tab, with two sections, is what’s pertinent.

Part 1 is this section. This image is a very scaled down version of the section. We have 13 houses, 6 mortgages that get paid, 6 credit cards that get paid regularly, and a few other lines that I removed.

All numbers are made up place holders, except the investments. I deleted my IRA contribution line because it’s wonky (but I will max out IRA contributions), but I wanted to show how much we’re investing regularly. There’s $75, per kid, per month, going into their investment accounts. Then there’s general investing happening with one $1000 transaction and two $800 transactions per month. Mr. ODA is investing into his IRA to max it out ($6500/12=$541 per month..sort of).

You can see that I’ve listed Mr. ODA’s pay dates at the top, and then his salary income on the next line. The gray section accounts for all rental income. I’ve allocated the income into the salary two-week period that makes the most sense (about half pay me on the 1st or 2nd, and the rest pay on the 5th). The green section shows routine rental property expenses. The entire next section are our personal expenses. The blue is left over from when I was managing two personal homes last summer (but kept it to differentiate our house bills versus other bills). The next gray section (which I’m only just realizing is a second gray and should be a different color as to not conflate the two grays.. what a rookie mistake) accounts for expense that come out of Mr. ODA’s bank account. Finally, I have an “other” section. This is where I capture large expenses that don’t need their own line item because they only happen once or twice a year. Here I’ve put tax payouts that will be due in October (that’s 4 houses worth, and it’s last year’s numbers – because I want to know how this year’s amount owed, when it comes in, changed from last year’s to discern if it’s reasonable or if I need to dig into it).

This is part 2. Now, part 1 accounts for the general timing of income and expenses, but it doesn’t perfectly capture the due dates, scheduled payments, or whether I’ve paid it and it’s hit the account.

The top line is linked to the section that I update our checking and savings account balances. Then I transfer all the items per pay period into this list format. In this example, let’s say I’ve already scheduled the gas payment. So I mark it as gray and put the date in the left column. Similarly, our investments are automatic, so I mark them in gray as we get to that two-week period.

At each border lined, I put the total for that section. You can see that at the end of the 9/2/23 pay period, I project a negative balance. Truly, we seem to have more income than I project (rewards cashed out, someone paying partial rent a little early, etc.), so I don’t take any action until I need to. There are Federal regulations regarding savings accounts; so we can only make 6 withdrawals from the savings account before fees apply. I manage these projects to know whether I need to make a withdrawal. If I need to, then I project what other expenses I may have and transfer a little more than I deem necessary.

THE PLAN

So our first step to him leaving is to pretend we don’t have his salary. Mr. ODA set up a new bank account. The majority of his paycheck goes into that account. We still have $250 going into another account, and about $400 going into a third account because we need to meet the requirements of direct deposits to prevent any account maintenance fees.

Our general principals in account management was always to take money into our main checking account, pay out bills for that two week period, and put the balance into savings. However, that wasn’t creating any forced feeling of managing without Mr. ODA’s salary. I’m more of a visual learner, so I appreciated this concept of having the money automatically transferred to a completely separate account.

EXECUTION OF THE PLAN

The first month of this plan had me on edge. The accounting in the checking account meant I was constantly back down to a balance of about $500. When I worked in an office, I was at the computer everyday checking our money. Now that I’m responsible for 3 tiny humans, I’m rarely on the computer. I project out our routine expenses, but there have been plenty of times where a $100 or $500 charge goes through that I didn’t have listed in my expense column for that period. Therefore, I like to keep at least $1000 as a buffer in the checking account to cover those little expense that can add up. So keeping the projection to less than $500 in the checking account panicked me.

Now wait. It’s not that we only had $500. We have a savings account linked to that checking account. We have this online account that’s taking Mr. ODA’s salary and just building the balance because we don’t use that account for anything. We have Mr. ODA’s old personal checking account. And last but not least (as my adorable 3 year old says all day long), we have plenty of investments that can be liquidated within 24 hours. We have the money. It’s just the panic of having the money in the spot where the bills are being paid.

SUMMARY

I’m sure there are easier ways or “better” ways to account for this. I don’t like automatic payments for bills because I like scheduling them against our cash flow. I’ve used this exact set up since 2012, and it hasn’t failed me. Taking full responsibility to pay bills means I am very scared to miss a payment and cause a negative hit on either of our credit reports.

Now that we’ve eliminated about $5,000 per month of income, without changing our spending in any way, I’m interested to see how things go. We have a great spending mentality – we’re not spending on frivolous items and we weigh the cost benefit of a purchase to us. That’s not to say we can’t do better. I’m sure we can be more diligent about our grocery spending or at least cooking what we already have in the house (we don’t spend much at restaurants in a month). I’ve already started tracking our expenses month to be sure we can watch our trends and re-evaluate our spending if needed.

Now that we have this account growing with no need for it to pay the bills, we will use it for fun things. We’re not very good about doing fun things. Two summers ago, we wanted to buy a vacation home at a nearby lake. We decided that instead of spending $1200 per month on a mortgage to go to the same place all the time, we’d plan vacations each month and spend up to $1200 without “guilt.” It was great. We had so much fun. But it lasted 3 months. Having a newborn put a damper on activities, but we’re ready to do the same again.

Over the past year, I tried really hard to stay on top of sharing content here, until I finally had to throw in the towel. It started because we were renovating a house while I was pregnant and had two kids to take care of, so my posts dwindled down to just the net worth updates. Then Mr. ODA started investing in treasury accounts. There was so much movement of money in so many different accounts, that I couldn’t quickly update our net worth anymore. Other than updates of the net worth and rental property work, my last post was August 2022. I feel like I have the bandwidth to finish several posts that I’ve started, so I’m back.

NEW HOME

In May 2022, a house went on the market in our desired area of town. We weren’t ready to leave our house since we hadn’t owned it for two years yet, but this was an opportunity that was hard to pass up. We closed on the new house in June 2022. We floated the down payment through a Home Equity Line of Credit that was paid off through the sale of our house.

We spent the whole summer traveling back and forth between our then-current house and the new house because we had a lot of work to do on the new house. We demolished the master bathroom and started rebuilding that. I painted almost the entire house. We did a lot of little projects. It was a tiring time that culminated in having to do the physical move in the Fall and get the new house organized and set up.

NEW BABY

I was pregnant through all of the home renovations and move. Our son came 3 weeks early on Thanksgiving day. He was generally healthy, but he required extra medical attention than we weren’t used to with the first two. On top of that, he wanted to be held to be asleep; babies sleep a lot. Mr. ODA and I were taking turns holding the baby and sleeping. The two older kids basically survived on tv shows and chicken nuggets during this blur of life. Going from 0 to 1, and from 1 to 2 kids was pretty easy, but this 3rd kid was a new ballgame. Once he was 5 months old, I started working on getting him to sleep independently. Now that he’s 7 months old, he sleeps well in his crib for his naps and through the night; he’s happy during the day and plays well; and now I feel like a new person for actually getting rest and not being tied to a couch all day everyday. Mr. ODA took a lot of time off to help me through that phase. As he started working again, it was an adjustment for me to learn how to manage all 3 kids and the household.

PERSONAL

We had several trips last summer on top of the renovations that we were working on. Those created delays in us having the house ready for us to move. Then our oldest got sick and it turned into an issue in his leg so he couldn’t walk at all for about 2 weeks and couldn’t walk right for about 8 weeks. It was a rough time. He got better just as I was about to have the baby.

As we started to get into the swing of things with all 3 kids and coming out of winter, my mom got sick. She went downhill quickly in March and ended up passing away on my birthday this year. That was unexpected and emotionally draining. We just got back from a trip to see my family, and I feel like I’m more put together than I had been over the last 3 months.

In April, we had to submit our taxes. This is always a several hour process. I had documented in the past, but I just didn’t have time to juggle it this year. I have to verify that I’ve recorded all expenses, that I haven’t recorded expenses that aren’t supported by documentation (e.g., receipt), that my summaries are logical, and then it takes Mr. ODA and I 5-6 hours worth of entering data to actually submit.

Then we added swim lessons and soccer for the kids. We quit soccer early because it just wasn’t fun for our oldest (or us), and 3 months of swim lessons are over. Now our only commitment is whether or not we want to attend library story time for a half hour each week, and I’m appreciating the open schedule.

BUSINESS

The rentals have required a lot more than usual attention from us in the past year. We had a house flood from a burst pipe, so that had to be cleaned out, renovated, and re-rented. We had several plumbing and HVAC issues among multiple houses, as well as a raccoon removal issue. We had roof damage to a house, a tree fall on a house, and another tree fall in the yard of three different houses, all because of storms. We had to turnover a house, where the tenant had lived there for several years, had made changes that were not appropriate, and would not communicate effectively on her status of leaving. It has been a lot more than usual, requiring a lot of time to manage.

On top of the maintenance requests and the usual management of the properties, I also took over the management of the properties that are in Central KY in February. I was spending so much time managing the property manager, that it was finally time for me to just handle it.

Not that you needed all this background, but I felt weird just jumping back into content. We’ve been very busy in general, but adding a 3rd kid into the mix was the straw that broke the camel’s back. I finally feel like I can manage everything again, and I’ve had more and more thoughts for things to share.

The market has recovered a good bit, so our net worth jumped. Our retirement accounts were at an intriguing low, but they’re back on track now. We also saw a few sales in the neighborhoods where our rentals are, so that increased our net worth based on the comps. We added a new property over the course of the last month as well.

NEW HOUSE IN OUR PORTFOLIO

We closed on a new house on March 24th. We worked on it for a few days, I held an open house, and we were able to get it rented as of April 8th. We had 16 days of vacancy. While showing it, most people were looking for a May or June start date, so we were lucky someone qualified for an April date. Back in 2016-2019, we were looking to follow the “1% Rule.” That means that if you buy a house for $100,000, your goal is to set rent at least $1,000 per month. This house isn’t even close. This market doesn’t allow for such a goal anymore because housing prices are soaring. The next goal would be to list for about $1/square foot. This house is 2100 square feet, but since the upstairs has smallish rooms and the basement is all open, we thought it wasn’t really worth pushing for $1/sf.

We bought it for $240k net, and ended up renting it at $1750. I wanted $1800, Mr. ODA wanted $1695, and when I went to list it, Zillow suggested $1750, so we went with that. Multiple people commented on how they appreciated the price, so we may have been able to get $1800 without an issue. I’m happy to have it rented, and I think these people are going to take good care of the house.

RENTALS

We put more money towards the house that we’ve been paying off, which is owned with a partner. We put our half towards it ($8,500), and it has a balance of about $600 now. The pay off quote required us to pay the anticipated taxes that will be paid out of escrow in May. We didn’t appreciate that, so we just went ahead and paid it down. We’ll let the May mortgage payment go through, wait for the taxes to get paid out of escrow in mid-May, and then pay it off. That’ll make 7 houses that are owned outright! But that also means I need to stay on top of insurance and tax payments.

We were just informed that one of our properties in Lexington that’s under a property manager hasn’t paid rent. She said it’s unlike them and that they aren’t even responding. She’s going to go to the house tomorrow to check on the situation. Since we’re paid a month after rent is received, this hasn’t affected us. A neighbor reported that they were moving out last month, but the tenant denied it. Perhaps they abandoned the property.

Once again, our two usual suspects didn’t pay rent on time. However, both of them actually made a better effort than they have been. One has paid this month’s rent in full, but has a balance of $286.31 (seriously…) to make up several late fees. I’m happy to waive late fees when it’s someone who communicates and isn’t always a fight to collect rent, but I’m holding this one to the balance owed. Another one told me that they wouldn’t pay until the last Friday of the month. I drafted an email to tell them that this is unacceptable because it’s been several months that they’re paying this late, and we need to work towards getting back to paying rent at the beginning of the month. Right after I drafted that, she sent half of this month’s rent. Better than nothing!

SPENDING CHANGES

Over the past month, we didn’t go out to restaurants very much. We haven’t been traveling because my family came into town for our daughter’s birthday party, and then I’ve been working on the weekend. Most of our spending went to gas (going back and forth to Lexington (half hour drive) multiple times per week!) and expenses to get the new house ready for a tenant.

I’m flying to my sister’s baby shower next month, so that another large and unusual expense on our credit cards ($250).

SUMMARY

We still have our state taxes to get paid. We went through the process of entering all our taxes, but we haven’t hit submit just yet. Surprisingly, we’re expecting a refund from the Federal side. The amount owed and the refund basically end up as a wash.

Our new property’s loan is a commercial loan, so it doesn’t get paid on the typical mortgage schedule, but on the 1 month anniversary of the opening. Therefore, the next payment is due on 4/24, and there’s no “1 month without a payment” type thing.

Clearly, our cash balance dropped significantly since last month because we had the closing. That was about $46k that we wired out, which was the expectation when we completed all the maneuvering with the cash out refinances in January. Our credit cards reflect our lower spending too, coming in about half what the balances were last month.

We have been surprisingly busy around here. I’ve been juggling a few rental issues, staying on top of some billing issues, and trying to make it through a commercial loan process.

At one point, most of our loans were held by one company. That was a more simple life. Even though we’re down to 6 mortgages under our name, it’s through 5 different companies. I’m really struggling keeping up with them and getting in a groove after our most recent refinance. I’ve mis-paid things 3 times now. I’m always on top of our payments, but something just isn’t clicking right now for me. I just paid one of our mortgages due April 1 instead of changing the date to be an April pay date. At the moment, we have a buffer in our account because we’re getting to this closing next week, but we usually don’t, so hopefully I have this figured out now that I’ve made so many mistakes.

RENTAL PROPERTIES

LEASE RENEWALS

We had 3 properties process their renewals this past month. Each of them had cost increases to their lease renewal (875 to 950 effective 5/1, 850 to 900 effective 8/1, and 1025 to 1100 effective 5/1). We have another property that will have a renewal offer go out this week. Then we have 3 that will need action by the end of April because the leases expire 6/30, and one that will need action by the end of May because it expires 7/31.

MAINTENANCE

We had a tenant reach out to us that they found bugs in their bathroom tub. She sent pictures and, sure enough, they were termite swarmers. I have way too much experience with termites. I called our pest company, and they sent someone out for an inspection to confirm they were termites. Then I got a call that because we didn’t pay the annual fee to keep our warranty current for the last 3 years (we had the house treated for termites in February 2019 when we bought it because there were active termites and extensive damage by the front door that needed repaired), they could charge us $650 again. However, since we’re considered a business account, she’d be happy to let us back pay the termite warranty and they’re treat it. So I paid $294 for the treatment instead (split with a partner on this house). She also informed me that they had cut off the hot water to the kitchen sink because there was a leak. I don’t know why tenants don’t tell us these things right away! I had my plumber out there the same day, and he replaced the whole faucet. That was $378. That’s one of those charges that’s frustrating because we could have replaced the faucet on our own, but we don’t live there anymore. Oh well; it’s also a cost split with our partner, so that helps.

We had another tenant reach out saying that her kitchen sink drained slowly. She’s been with us since we bought the house and never asks for anything. She’s on top of communication and was super appreciative each time we agreed to renew her lease. We had done a huge sewer line replacement project at this house, so I was skeptical of the issue. It turns out there was a plastic fork lodged down there, but I just let it go (meaning, she’s then technically responsible for the cost). Our property manager let her know that if it happens again, she’s financially responsible, but we’ll cover the cost ($200) this time.

RENT COLLECTION

We FINALLY got the check for one of our tenants that had an approved rent relief application. They submitted an application in November to cover December, January, and February rent. By mid-December, they ended up paying December rent because they hadn’t heard (and the application expires, meaning their protection from eviction expires (not that I would have pursued eviction for this group because they’ve been great tenants for several years)). They received approval for 3 months worth of rent and 2 late fees on January 11. We received the check on March 4th. So frustrating in that process, but still better than an October approval and us getting those 3 months paid at the end of January.

We had our usual suspects not pay rent. On the one house, they didn’t tell us they weren’t paying rent for the longest time. Now, they tell us they’ll pay us on a later date. I let it go this month, but with them paying on the 23rd, that means we’re in a perpetual cycle of not getting rent on the 1st. We have a partner on this house, so I plan to address it next month if they claim another 3+ week delay in getting us the rent. On the other house, she let us know in February that she’d struggle to pay rent and she gave us random amounts throughout the month. I let her know she was still $106 short from February and that she was now in default of March’s rent, and I got no response. Then Mr. ODA had $1000 show up in his account on Friday. She still owes $371 between the two months, but at least we have the mortgage payments covered. She’s also the tenant that we plan on not renewing her lease because she’s caused issues throughout her tenure.

BUYING A NEW PROPERTY

We’re still in the process of getting through closing on a new rental property. We’re expecting to close not he 24th, so we’ll see how that goes. It’s a commercial loan, and it operates different from residential mortgage underwriting, so we’re in the dark. Communication has been next-to-nothing. We’re currently waiting on the appraisal to come back. That was our one hurdle to getting into the house. I said once the appraisal clears, then we (as the buyer) shouldn’t have any risk in getting to closing. Therefore, we were hoping to have the house painted before we close (I would do the painting), then we could refinish the floor and get the rest of the cleaning done the weekend after closing, and get it listed for rent for April 1. I suppose I wouldn’t be trying to get to the house before Friday, so I guess I can be patient and wait to see what happens with the appraisal for a few more days (even though the appraiser was on site last Tuesday, and I’ve never had it take more than a day or two to get the paperwork).

REFINANCE FOLLOW UP, STILL

We still have an issue with the mortgage that I ended up paying 3 times for the 2/1 due date. Our refinance was difficult, and the communication continued to be difficult after closing. I asked on 2/1 whether our loans had been sold yet because I was surprised I hadn’t heard. Usually, I see a note saying to pay the new company before the first payment, thereby not paying the first payment to that “first payment notice” place that comes with the closing documents. The company’s contact said to keep paying them because they hadn’t sold the loans yet. I didn’t open the attachments in his email because I assumed he was reiterating what he said in the email. Turns out, one of the loans was already sold, and I should have paid the new company. Well, I processed a paper check to go to a completely different company (started with a C, and I didn’t catch that I selected the wrong one in bill pay). Luckily, that company sent us our check back, saying they think our loan is closed with them and they can’t process the payment (thank goodness we once had a loan with the address I put in the memo line so they could clearly make a connection and say “we don’t want this!”). When I noticed my mistake on the 14th, I sent a handwritten check that I rushed to the post office at 4:55 to get post marked. In the meantime, I found out that I was able to set up an online account with the new company even though I didn’t have the loan number yet (they gave it to me over the phone). I paid the new company online to make sure I didn’t have anything on my record claiming I didn’t pay by the 15th and it was late. I figured I’d rather manage 3 payments being made than fight the credit companies to change my credit report. Well, the initial company cashed my handwritten check, but they still haven’t sent the money to the new mortgage company. They just kept telling me they have 60 days to get it to them, and I said that’s unacceptable that they’re holding my money. That was a week ago that I was told I’d get a call back, and I haven’t heard from them.

PERSONAL EXPENSES

Now that the basement is done, I had a strong urge to finish projects. There were several things that were starting but not completed. Those final punch list items always seem to take forever. I was impressed that Mr. ODA pushed to get some of the things in the basement done right away, even though they weren’t on a critical path. However, I didn’t uphold my end of the project by painting those things, so I got back to that. I mentioned several of the projects in a recent post, and I’ve done a whole lot more since that post. But all that to say, I’ve spent a lot of money in the last month. I bought a lot of supplies to finish off these open projects. I also had big purchases of cabinet hardware, a dining room table, a desk, and a wood. We haven’t done very much out of the house, so we don’t have a lot of other expenses than these projects, which means our credit cards are actually have the usual balances. We did book an AirBnB for a trip at the end of the summer with friends of ours. That was a big hit on the credit card for a week at the beach, but they reimbursed us for their half.

SUMMARY

It feels like I just keep lowering the balance in our investment accounts each month, but I went to look at February 2021 to see the total. Even though some balances have decreased, we’ve still contributed to the accounts, so overall they’re $21k higher than last year, which is encouraging. I guess I should also focus on the property values raising significantly. We’re over $500k higher than last year in our assets, and our liabilities (i.e., mortgages) are about 13k less than February 2021. We’re also still over $3M on net worth, even if we’re hovering right around that. We’ll add about $50k to our net worth by the end of the month, as long as we close on the new property on time.

This month is basically just story telling, from insurance tidbits to mortgage annoyances, while not addressing the decline in the market and our investment accounts. 🙂

It seems all my mortgage payments are increasing on 3/1, so I’ve been managing those changes. I mentioned recently that one of our houses had the escrow analysis done incorrectly. Luckily, that was addressed, and the increase in our mortgage payment is only about $100 instead of nearly $200. Our personal mortgage increased by $16, another property increased by $52, and then our last 3 mortgages were all refinanced in January and this ‘first payment’ has been a bear. The information out of the refinancing company has been contradictory, they requested a bunch of information weeks after closing to support all the money they already gave us, and it’s just been rough. Rough enough that I ran to the post office to get a check in the mail at 4:48 pm today, only to get home to an email saying that I had to send that check (due tomorrow) to a different address. Ugh.

I was excited to share some positive news this month, but that got overshadowed by these mortgage payments! Anyway, we came home to some surprises after our vacation.

First, I had a medical procedure done in January. It was originally scheduled for November, but the week of the procedure, I had my heart go crazy on me. That cancelled my procedure because I couldn’t go under anesthesia until they knew my heart would be OK. We got my heart sorted out enough that I was cleared for the procedure, but once I was able to reschedule it, it went into 2022 ….. a new deductible year. They said that I needed to pay half the cost of the procedure before they’d schedule it. Since I had been waiting since September for this, I wasn’t going to question anything, and I gave my credit card number for $1200. Well, my insurance hasn’t processed the procedure yet, but I guess since I paid in advance, some sort of system review showed I had overpaid, and they refunded me $1196. I don’t know how they decided to keep $4, but I’ll cross that bridge when I see my claim is processed on my insurance website.

Second, I’ve mentioned before that you need to stay on top of insurance! I received a bill for my heart-related-ambulance-ride for over $900. The last time I was in an ambulance, I ended up owing the full bill, which was $500 at that time. When I saw $900, I figured, gosh 10 years later and a new jurisdiction, and THAT is what I owe. It said “we billed your insurance, and this is your balance.” Hmmm. Log into my insurance website and see there’s no claim history for an ambulance ride. I then learned, for the first time ever, how to submit my own insurance claim. I let the fire department know I submitted the claim, and then they said they’d do it for me! Why did your paper say you already did?! Well, the surprise I got was that my insurance covered all but $46 for the ride!!! I couldn’t believe it. That’s the happiest I’ve ever been to spend $46.

The most random thing that happened was a check from our electric company from our Virginia house. We sold that house in September 2020. Our mail forwarding isn’t active anymore and it was sent to our old address, so I really have no idea how we got it. It was $31.09 due to a required review of all accounts every 3 years. It’s not anything crazy or life changing, but that was truly a surprise!

RENTAL UPDATES

We had our usual suspects not pay rent earlier this month. One flat out said they won’t pay until the 23rd. I’m not even sure how to handle them anymore. I keep reminding myself that we raised their rent $150/month to get them to leave, but they accepted. So at least we’re in a good position there? The other paid us $700/$1150 on Friday (late). She at least emailed us with the awareness that we shouldn’t have to hunt her down for rent payments, so she got a pass because I was about to send the default notice at 12:01 am on the 6th. I’m also once again in a position of tracking down a rent relief payment on another house that’s supposed to cover December, January, and February. While the tenant ended up paying December rent, we’ve still been floating the January and February finances. The approval of their application (that was submitted in November) was January 10. As of today, no information from the State and no check in the mail.

I got a tenant renewal processed this morning. We increased their rent by $50/month (starting 5/1 when their current term ends), after it having been steady for 2 years. Our usual baseline to keep a good tenant is a $50 increase every 2 years.

We gave two property managers notice to increase rents on 2 properties that are up for renewal on 4/30. We do 60-day notices. It’s not entirely necessary, but I look at it as a way to negotiate with the tenant for a month, and then if they don’t agree to new terms, we have a month to get it rented. One ‘cried COVID’ last year, and we let her by. She’s been there 2.5 years at the same rate, and she even got the house under market value originally because it was November (bad timing). She’s at $875 and we said we’d go to $950. That’s a larger increase than we usually do, but the market rate for the house is $950-1000. If she balks, we’ll manage the turnover and get a new tenant in there. For another house, they’re at 1025 and have been since October 2019. They even negotiated a discount back then for an 18 month lease, so they’ve been under market. Despite our efforts to grieve our taxes, the City thinks this house is in an affluent neighborhood and has charged as such. We’re offering them a bump to $1100. Again, more than our usual $50 increase, but it’s been more than 2 years and $1100 is under market value. Then we had a 3rd person say she wants to stay in the house, but her lease isn’t up until August. She’s been there since August 2017 and has been at $850 rent since then. We’re looking to increase her rent to $900. She’s an awesome tenant that never needs anything, and I know she’s in grad school without much money. We’ve made her so happy for the last several years by renewing her without an increase, so I hope she understands the need to increase it now.

I paid the insurance on our townhome, which is a property we own outright, so I need to manage the escrow-type transactions. That was $210.

After our cash-out-refis in January, we have been looking for a new property to purchase. We’ve made 4 offers that have been out-bid. Mr. ODA has been trying to work the off-market angle. We made a full price offer for one of the houses contingent on seeing it, and the guy said that he’d now prefer to sell off his portfolio as one instead of each individual house. He declined our full-price-off-market offer. Sketchy. Then another guy said he wanted to wait until the new flooring was installed in his house before letting us see it, and then he won’t respond to messages now a week or so later. Interesting. We’re now trying to work another off-market deal through our Realtor, but the seller and our Realtor are out of town. I ran the comps on it and come to $235ish, while they were expecting $250k. I don’t deny that they’d get an offer in this market at $250, but I don’t know that it’s worth it to us. Then again, to be done with this driving around, seeing houses, making offers, and losing out, may all be worth an extra $15k.

PERSONAL TIDBITS

This month, we went on a trip for just about a week. The flight was paid for in a previous month, so that’s not captured in our spending. We stayed with a friend, and she made us nearly all of our food. We paid for our brewery visits with her. It was a great trip, and I definitely recommend Bend, OR! We did a last minute change from Touro for our rental car to a ‘regular’ car rental place at the airport, so that charge shows up in this month’s finances. We also booked 2 last minute hotel rooms, once for the night of our arrival and one for the night of our departure (we flew in/out of Portland, which is about 2.5 hours from Bend, so it was easier with the kids sleep schedules to be near the airport those two nights instead of arriving really late or leaving really early).

We bought Hamilton tickets. We were late on that band wagon until we finally found a friend with Disney+ who wanted to watch it with us even though they had seen it 257 times. Since December 2020, we’ve watched Hamilton a whole lot. We got on right when tickets were being sold and were about to accept the $200+ ticket price until Mr. ODA found the ticket sales through the actual venue were only $130! It’s not until June, but that’s something to look forward to!

We finished our basement over the last year and have been using for the last month now. We had a projector on hand that we used as our TV down there, but it started to die shortly after we hooked it up. We bought a new projector and have been really happy with it, and I was happy with it only being $270.

While our electric bill was surprisingly low last month, it was surprisingly high this month. They did an estimated meter reading, putting the estimated kWh usage at the highest it’s ever been. When I questioned their estimation process and shared the current meter read, they said that next month will probably be an actual reading and since it’s not more than 1000 kWh difference, they’re not going to change anything. Sure, I can afford this $414 bill that may be offset next month, but many people can’t. Their estimation process shouldn’t put the projected energy usage at an all-time-high, thereby dumping surprisingly large bills on people. Regardless, it’s something that works itself out, and isn’t something I’m going to fight any harder on right now. It’s just annoying knowing that our energy usage was high last year because we had a broken unit without our knowledge, and then with a working unit, they’re estimating that we’ve used more than ever.

Mr. ODA changed one of our credit cards, so I’ve been all out of sorts here now. The credit card was a travel-related card, and they increased their annual fee by $100. He ran the numbers and determined the benefits didn’t outweigh the cost increase. Instead of closing the card, they agreed to change the type of card. However, all the things we used that card for are now on different cards, and this change “activated” an old card of mine. Our credit card usage is convoluted; perhaps I’ll do a new explanation and update my last post on it (and then maybe that’ll get me to remember all the changes!).

NET WORTH

Our net worth dropped about $15k from last month, but that was due to the market. While not fun to see those numbers go down, it doesn’t affect our day-to-day. Our cash balance is really high right now while we keep cash liquid for a downpayment while finding another investment property.

Why did we do so much traveling and activities this spring and summer? Most people probably assume all our travel was making up for a year of not traveling during the pandemic, but we came at it from a different perspective.

We’ve had a long term goal of a beach/lake/mountain home. After another failed search to make this dream come true this past Spring, we decided to redirect that money to trips this summer. I’ll run through the background, the financial decision, and how we spent our travel “budget.”

BACKGROUND

We first looked into a vacation rental in Snowshoe, WV – six years ago. Snowshoe is a ski resort, and one of the better available ones to those of us south of the Mason Dixon. It also has a draw during the summer with hiking and mountain biking, albeit not as constant of a stream of people needing a rental. The draw for us was that it was halfway between our home in VA and Mr. ODA’s family in KY.

We went as far as meeting a Realtor and looking at properties. If the house was off Snowshoe proper, it was a good distance from the ski lifts and not in great condition. If the house (condo) was on Snowshoe proper, it came with a lot of rules and regulations and costs. Everything near the ski lifts had to be under Snowshoe’s management, which included their cleaning costs, and their booking process. This meant that someone couldn’t necessarily go onto the website to book our unit. Someone would go on their website and book “a 2 bed and 1 bath unit” and the system would cycle through the bookings. With the high condo costs and the uncertain bookings for those units, as well as the distant location of the units that weren’t subject to the condo process and cost (plus finding a management and cleaning company for that), we stopped the search.

Since then, it’s been on the wish list, but we weren’t sure what direction we wanted to go.

When we moved to KY, we decided to look into a lake house. We want it to be close enough that we could just pick up and go (e.g., trying to keep it under 2 hours), we want it to be on a lake that allows motor sports (so this rules out anything that’s “no wake” or prohibits motors of any kind), and we want it to be lake front (we learned this during our recent search, and hadn’t fully realized how much we wanted this until we saw a house that wasn’t on the lake directly).

We looked at parcels of land and kept an eye on a few houses listed in the March/April timeframe of this year. Our initial thought was that we would purchase land and hold it until we were ready to have a house built. The parcels of land we looked at didn’t meet the criteria we wanted (good size, on the water, ability to build a dock). I started to feel like we were pressuring ourselves to make a decision for something that we didn’t actually need.

We took a break and just kept an eye on Zillow. We went to see a new construction house on Herrington Lake, but it wasn’t actually on the lake. It was next to the community pool, across the street from the community’s dock, had 3 bedrooms and 2 bathrooms with a loft, and it was brand new. It even had a two car garage, which wasn’t something on our wish list. However, the price tag was high; it had been listed for many months, and we didn’t feel the comps supported such a cost for it not being literally on the lake. We spent a lot of time mulling it over, but decided to not even put an offer in. Lucky for the seller, they did get a full price offer shortly after that.

I decided that we should wait at that point. I figured we may have better luck waiting until the end of the summer (perhaps people will think they’ll spend their last summer on the lake and then unload it?), and that we shouldn’t force this decision to not get exactly what we want for something that isn’t a necessity.

THE FINANCIAL DECISION

If we purchased a $250,000 second home, and I assume an interest rate at 4.5% (even with excellent credit, the rates you see advertised are for primary residences), we’re looking at a mortgage payment of $1,200. On top of that, we’ll have escrow costs, HOA costs, the possibility of management fees, and then even PMI costs. That was another big factor; we’ve been throwing any ‘extra’ money towards paying off two rental property mortgages, so we don’t have $50,000 liquid to cover a 20% down payment. Without having the 20% down payment, it wasn’t even guaranteed that we’d be able to get a loan for a vacation house.

Knowing $250,000 was even more than we expected to spend, I conservatively assumed $1,200 in monthly house costs. Instead of spending $1,200 each month to go to the same destination over and over again, why don’t we just mentally allocate $1,200 each month to travel and go to all different places? And so, months of a crazy amount of travel began.

HOW DID WE SPEND OUR ENTERTAINMENT ALLOCATION?

MAY: $618

We started with a last minute trip to Atlanta to see the Braves. We spent 4 nights in Atlanta, went to two baseball games, met up with family for lunch, visited Stone Mountain, and explored the city parks. We stayed in a 2-bedroom hotel room because it was cheaper than any AirBnB options, and I was highly focused on giving the kids separate sleeping spaces. The hotel experience was less than favorable (dirty, AC broken, limited breakfast, roaches … and a good name hotel!), and after some conversations with the hotel, we ended up not paying for it. They had credited us one night without us asking after the AC continued to not work after their “fix.” Mr. ODA then had a casual conversation with the manager about the stay as he was checking out, and the manager credited a second night. I thought we paid for the rest of the nights, but it never showed up on the credit card. Our total trip cost was $460.

Later in May, we went camping in the Daniel Boone National Forest with some family. We booked a “cabin” (I used that term loosely; it was walls, a roof, and platforms for sleeping bags, but it had electricity and AC!) for two nights. We went swimming, rode bikes, and hung out under a canopy while it poured on us for most of the main day we were there. Our dog got to come on this trip, so we didn’t have any pet fees. We brought groceries to cover our meals since there’s nothing close by. Since we’d be buying groceries anyway and gas is negligible since it’s an hour away, I’ll just focus on lodging, which cost us $158.

JUNE: $200

Almost a year ago, we planned a trip with the extended family to Hocking Hills. This shouldn’t really count against our “monthly allowance” mentality since it was going to happen regardless, but I’m including it anyway since we didn’t do any other June trip. Mr. ODA’s parents covered the cost of lodging, and the rest of us covered the cost of food and our canoe rentals. We went hiking, got rained on, and played games at our rental. On the last full day, we rented canoes and went down the Hocking River, which was a great experience. We went with 6 kids, 3 of which were under 3 years old. So if you’re a beginner or looking for something to do with little ones, this was a fun time for $52 per canoe! This trip cost us about $200.

JULY: $690

Before we left Virginia, we discussed doing walk throughs of our properties and being more present with them. There were some properties that we hadn’t seen since we bought it because they don’t have maintenance requests or we call someone else for the work. Well, it was a whirlwind to move, and we didn’t do that last summer. After the debacle with the flooring replacement at one of the houses, we knew we needed to get back there to tie up loose ends. We have a wedding to attend in the area in September, but decided this couldn’t wait until then. The first weekend we could go ended up being the 4th of July. Being in Richmond, VA, there isn’t a large AirBnB market for a normal sized family. All of the options that were available were meant for multiple families in a large house, and we just aren’t interested in paying $700 per night for ourselves. We went with a hotel halfway between Richmond and our old neighborhood, and because we stayed for 5 nights, it was considered “long term,” and it only cost us $525, which included $75 for the dog being with us. Since our entertainment was either working on rental houses or visiting with our old friends, we just had food and gas costs. The total trip cost was $690 (and most of that was tax deductible!).

AUGUST $1069

We learned that St. Louis is only about 4.5 hours away from us, so we looked to see the Braves’ schedule. They were scheduled for mid-week games for the first week of August, so we marked it down. Unfortunately, things were busy, and I didn’t make the plans in advance. I struggled to find pet care for our dog, and I ended up booking an AirBnB the morning before we left. We searched and searched, and this one randomly popped up that morning, and it worked out well. Lodging cost us $585. Our entertainment (tickets and parking) cost us $135. Food and gas cost us $213. Total trip cost was $933.

My plan to visit my family in NY in July didn’t come to fruition because we had to manage 4 days worth of our builder being here to fix things in the house, and then I had a doctors appointment pop up that had to be a specific time. Instead of driving there and back (12+ hours each way), we booked some flights. We’re able to go from Cincinnati to JFK directly (such a blessing with 2 kids under 3!). The flight was 2 hours, plus an hour on each side for driving (although, it took us an hour and a half to get to my parents’ house when we landed at JFK because a 3:20 arrival, plus what felt like a 2 mile walk from the gate to passenger pickup, put us at getting on the Belt Parkway at 4 pm – that’s not good for that area!), and getting to the airport an hour early. We left out of LGA, but it was still a direct flight, and we arrived 25 minutes early! We had hardly any wait at TSA for either leg, no issues with boarding or the flight, and we got our gate checked bags easily. I’ll take 5-6 hours of travel over 12+ hours. The flights were booked through our Chase Travel Portal, costing us the equivalent of $833 in points. The parking is $9 per day, the gas to get there is negligible, and we actually didn’t spend anything on food (I very much owe my parents for that!). Our entertainment goal was to go swimming in my parents’ pool the whole time, and that’s just what we did! The trip cost us $36 in parking and $100 for our dog’s boarding.

On top of these long trips, we also did a lot more activities that were just for one day. We went to 2 Reds games, the Cincinnati Zoo several times, a UK baseball game, Bernheim Forest, and random family/friend activities. It turns out we didn’t spend the $1200 per month we had mentally allocated, but we kept ourselves really busy and had a great time making memories!

Now it’s time to enter a new phase of life: preschool and sports! I’m pretty excited!