When looking to rent your house, you should do your due diligence. Our concerns are whether a person has a history of late payments, collections accounts, and if they have a criminal history.

We do two steps of initial screenings before asking a tenant to pay an application fee. The first two steps given them the opportunity to disclose anything that may be seen as unfavorable or not meet our rental criteria. This way, once they pay the application fee, it’s a verification step, and they’re not wasting any money for me to find out that I’m going to decline them.

Here are the details of how I go through the evaluation process, and specifically how I just did it for our new rental.

RENTING CRITERIA

First, I send everyone interested an “Interest Form.” We ask for their legal name, contact information, credit score, employment data, number of occupants, whether they smoke, if they have pets, if they’ve been evicted, and if they’ve been convicted of a felony. I also ask them to provide any other information they think I should know that may affect their ability to rent the house. I send this form to everyone who expresses interest, and it’s the first step before scheduling a showing. I request the data before scheduling a showing because I don’t want to waste my time or theirs showing the house, when they had adverse responses to our criteria. This was more important when I was scheduling individual showings, but I now conduct an “open house.” I set aside two hours to be at the house and ask they come during that time. If that doesn’t yield a tenant, then I’ll evaluate who couldn’t make it and field new requests to see it to determine if I’ll show it individually or host another open house.

We have this at the top of our Interest Form.

Properties are offered without regard to race, religion, national origin, sex, disability or familial status.

Required standards for qualifying to rent a home are:

• Each prospective applicant aged 18 or older must submit a separate application.

• We limit the number of occupants to 2 per bedroom.

• Your combined gross monthly income must be at least $4,000.

• You must be employed and/or be able to furnish acceptable proof of the required income.

• You must have a favorable credit history.

• You must have good housekeeping, payment, and maintenance references from previous Landlords.

Compensating factors can include additional requirements such as double deposit and/or a cosigner.

Our typical rental actually requires 3x the rent as the monthly income, but since our last house was more expensive, we put the requirement as a dollar amount threshold instead.

Then I would historically review those who say they’re interested and pick the one that appears to be most qualified. I’d send them a “pre-application” form to fill out. However, for our last tenant search, I asked everyone interested to fill out the “pre-application.” The tenant screening system doesn’t tell me their last landlord information or their employer, which are both necessary for making phone calls and checking their information given. The “pre-application” repeats some of the questions on the Interest Form, but the pre-application requires them to sign the form as an “affidavit” that the information is accurate.

If they tell me that they’re going to have a low credit score, it helps me to know the reasons for it up front. Additionally, by letting me know any issues up front, it saves them money. If they self-report that they have several collections accounts, then it could be cause for me to move on to a different person interested. If they don’t tell me that they have some issues in their history that may be unfavorable, and I send them the application, then they’re spending $40 per person only to potentially not get the house. I prefer to use the online tenant screening as a final verification step than an initial screening and potentially waste someone’s money.

One time I got through all these steps, had 3 different people submit an application for a house, and the report came back with an eviction. We asked why they didn’t disclose that to us originally. They told us a story about how they were asked to leave somewhere, but they didn’t know that it was reported as an eviction. We told them that they were disqualified. We went with our “runner up,” and they’ve been in the house almost 3 years without any issue or late payment.

We also had two people submit an application and then a bankruptcy was reported on the credit report (it was before the pre-application step I implemented). She said she didn’t see a place to explain a bankruptcy, so she didn’t think to mention it. For future reference, if I ask for your credit score and you have anything concerning in that credit report, it’s helpful to be upfront about it. In that case, everything else was fine and her explanation for the bankruptcy was clear and thorough. We gave them a chance, and they were amazing. She was rebuilding her life after taking on a lot of new bills after a divorce, juggling single-income life, and it was a way to consolidate the debt.

DECIDING BETWEEN TENANTS

In this last situation, I had several people express interest in the property.

I held the open house, and I asked everyone to let me know by noon the following day if they were interested in pursing an application after seeing the property. I received 6 or 7 people who were interested in the house.

I don’t look at one factor. I weigh all the information given to me in my head. In a perfect system, I may assign a weight to each data point, but that’s more effort. I’m reviewing the data and trying to see who has the best, well-rounded criteria.

The house is big (2100 sf with 4 bedrooms), and rent is higher than anything we’ve ever managed. I looked at what they are currently paying in rent. If they’re currently paying $1500 per month, then that made me more confident that they’d cover the $1750; if they are currently paying $400 per month, then I was concerned that they weren’t prepared to cover such a large expense difference. Along those lines, I also gave more credit to someone who has a stable job that they’ve been at for more than a year, versus a few people who said “I’m starting a new job at the end of April.” We have a tenant that goes through jobs every 1-3 months and is always a pain with rent, so I’m probably more scarred by job history now.

I gave more credence to those who had at least a 600 credit score, but I didn’t rule out anyone with a credit score less than that. One woman did have a lower credit score, but she had other good information, so I didn’t rule her out.

Finally, the determining factor came down to availability. My top two contenders had different desired move dates. One said early April, and another said June 1st, but May 1st may be ok. When I asked her to explain about her move date, I received a detailed story that didn’t have any conclusion on when she was available. Since this is a business, and I had a qualified group interested in the house sooner than others, they were the ones selected. If I didn’t have someone qualified for an April move in, then I would have waited for a May 1st rental instead of lowering my standards.

Luckily, I had enough interest in the property that I could select someone who was well qualified and get it rented sooner than later.

APPLICANT SCREENING

Once I’ve given someone these two opportunities to disclose unfavorable information in their credit or criminal history, and they’ve provided favorable responses that meet our criteria, I send the link for the application. The potential renter enters their data into the system, which helps keep their information secure (e.g., I don’t have their social security number) and helps eliminate any typographical errors that I may make transferring the information into the website instead of them entering the data they already know. Additionally, the tenant pays the fee (currently $40) directly to the website, which helps them understand that once the report is run and the fee is paid, it was for a service so it’s not refundable. I heard multiple stories this past week where people paid “application fees,” but were later told that they weren’t the first to respond. That’s not fair. I don’t need to know everyone’s detailed reports and cost people money if they aren’t going to get the property. So here’s how I handle the tenant screening process.

The system generates a report for me to see that includes their credit history, criminal history, eviction history, and income verification.

– The credit history shows any missed or late payments; collections accounts; bankruptcies filed with the chapter, date filed, and amount settled; and their score. I’m more concerned about late or missing payments than anything else there. The collections accounts are typically related to medical bills, but if they’re for general credit cards or an enormous car loan, I’d find it more concerning. I’ve also not ruled someone out simply because they’ve filed bankruptcy; two of our tenants actually have a bankruptcy in their report.

– The criminal history tells me if they’ve had any judgements against them. I’ve seen traffic violations, misdemeanors, and felonies. The report also tells me if they’ve been listed on any sex offender registry. If they have felonies, multiple misdemeanors, or are on a sex offender registry, it’s automatic disqualification. I’ve gone down the road of giving people chances, and it hasn’t gone well. This report isn’t fool-proof either. I know how to use the court record system where we have most of our houses, and I now look them up in all the nearby jurisdictions to be sure there’s nothing reported.

– The eviction report will tell me if they’ve been formally evicted. This doesn’t capture any times where a tenant and landlord agreed on the tenant’s departure outside of the court system. This also may miss some jurisdiction evictions. We had someone show up in a separate jurisdiction when I went looking for their information in the surrounding areas, but it didn’t show up on the report. Don’t think that this report is fool-proof.

– The income verification comes with a built-in caveat. I don’t know the details on how the report is run, but the result is something along the lines of “we believe that the self-reported income is near accurate.”

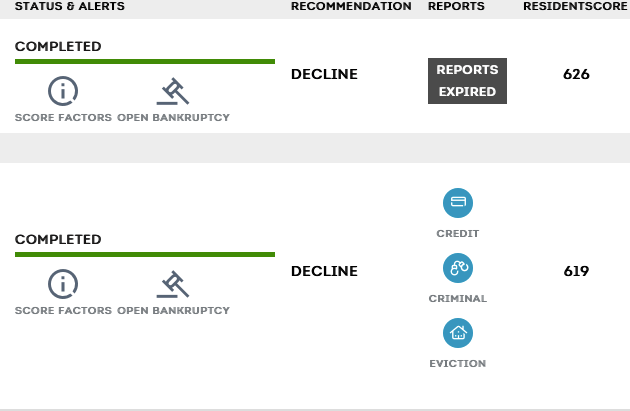

The report suggests whether to accept or decline the applicants. I suggest reviewing the data and making a decision for yourself. Some reasons why the recommendation will be to decline include: criminal history, bankruptcy, and low credit score.

We have given several people “chances” that don’t perfectly meet our criteria. Below is a screenshot where the recommendation was to decline. However, we ended up asking for more information and giving them a chance. They ended up spending a year in a rental of ours, moving out of the area, and then asking for our rental availability when they came back to town. They always paid on time, hardly asked for anything, and took great care of the house.

We have also accepted tenants that had some concerns in their report, but the system recommended we accept them. We tried to overlook the issues, but we’ve ended up regretting it. We have one tenant who has a criminal history (forgery) and we ended up having to release her roommate from the lease because of a domestic violence and restraining order issue. She’s also consistently late on making rent payments and doesn’t keep communication lines open. We plan to ask her to leave at the end of this lease term. We also had a tenant with a 480 credit score who wrote us a letter about her low credit and asked for a chance. She ended up consistently paying late (she always paid, but it was always a fight); we threatened eviction when it got to a breaking point where she was combative, but she left on her own terms. That’s a good example where she was a terrible tenant, who we gave multiple opportunities and even restructured her rent, but her eviction report won’t say anything to that effect.

DEPOSIT

Once I have an approved application, I request a deposit to hold the property and remove the listing. Typically, the lease signing doesn’t occur immediately. In those cases, I want protection of my cash flow that I’m holding the property for someone specifically. I’ve had a couple of houses that have signed a lease immediately, but typically there’s a lag between “acceptance” and the lease being signed (forming a contract).

In this last instance, the tenant was accepted on Friday, but the lease wasn’t going to be signed until the following Thursday. I requested a $400 deposit, which will be applied to their balance owed to get the keys transferred to them. I originally was going to request $500, but I realized that the week’s worth of time at the rent per diem rate came to $408. If they back out between now and Thursday, then I haven’t lost income if I had chosen someone else and not held the property until the date they wanted a lease. Ironically, they ended up paying a deposit of $500. For them to obtain the keys, they owe a security deposit ($1750), the first month’s pro rated rent (about $1300), and a pet fee of $500. Their total is $3,550, but the $500 I’ve already collected is applied to that balance. Therefore, on Thursday, they’ll owe me $3,050 for me to hand them the keys.

Usually, I require the first month of rent to be the full amount, and then the proration is applied to month 2. Since for this tenant, they already paid rent at their current address for the month of April, and the rent here is higher than our average, I went ahead and prorated the first month so they didn’t have to put so much cash out of pocket in a short period of time.

SUMMARY

You can see how I am not making black-and-white decisions. I’m not hanging my hat on one or two factors. I’m being reasonable in my decisions and understanding that there’s a person, and maybe a family, on the other end of this transaction.

Be fair. Utilize a variety of factors in making your eligibility determination. Keep your communication lines open with potential renters until you have a deposit and/or lease signed on the property.

Treat this as a business and make informed, logical decisions instead of emotional ones, but be reasonable.