Welp, I haven’t posted in a month. We have been so busy and exhausted.

We bought a house on June 15. That process was not smooth in the week before closing, even through the day of. Our attorney had to come to our house the next day to have us sign other papers. Our lender was great, great, great, until they weren’t at the 11th hour. As always, everything went through, and we have ownership of the house. And that week will be a distant memory soon. But why does the mortgage industry get away with operating this way? I feel like there hasn’t been a single transaction we’ve done where there wasn’t a “where’s my paperwork????” or “why’s this wrong the day before closing???” moment (or my favorite, when we begged for the HUD-1 to review it before closing, and a traveling notary showed up at our house, only for the HUD-1 to be different than the closing disclosure and the numbers to be wrong on both documents).

We used our HELOC on our current house to pay the downpayment and closing costs on the new house, so that was a quick debt addition. We started with a balance of about 86k and have paid it down to 75k. We didn’t necessarily need to take the whole amount from the HELOC, but it was easier to get one cashiers check from the HELOC and immediately pay towards it than to transfer some from the HELOC and do a wire from our checking account.

This new house will be our personal residence, but it requires work. We’ve gutted the master bathroom, and I’ve been painting nearly all my free waking moments. I have the first floor mostly done (including making a ceiling go from navy to white.. ugh) and the kids’ bathroom done.

We opened two new credit cards in the last month, but I’ll get into that in the next post. Just note that our credit card balances are higher than our usual, and will remain that way.

We had opened a checking account for rewards a while back, and the account required $500 of direct deposits each month. It was one more account to manage, and it was no longer serving a purpose, so we finally closed that. Now we just manage two checking accounts.

RENTAL HOUSES

We have a vacant rental house as of June 30th, which I’ll also get into in a future post. The good news is that one of our houses that’s a repeat offender of not paying rent is now out of the picture. We still have one house that never pays on time, but I’ve at least got them paying half the rent by the 5th so that we aren’t constantly floating their mortgage and bills until the last Friday of every month.

We had two rental increases go into effect this month. One was for $20 (good tenants, long term, told us in advance they wanted to renew, but we also needed to cover our cost increases) and another was for $50.

Our property manager in KY hasn’t been easy. We’ve had to do a lot of managing the manager. All of our paperwork says not to charge the 10% fee on contractors. The document that they put in our file says it, and that’s the same document they put the charge on. I keep having to ask for all the documentation. Once I ask, they note the 10%, but it’s not until I ask.

We paid a plumber to fix a shower handle in one of our houses. On June 1st, she texted that it was loose. She didn’t really explain the situation, and I asked her to tighten the screw and let me know. She texted me on July 8th that it didn’t work. Where have you been for a month?! Then she said “let me know when the plumber is coming so I can wake my husband.” Um, you waited 5 weeks to tell me that it’s still broken, I’m not rushing a plumber out there today.

One of our insurance companies dropped us once they found out we don’t live within a certain radius of the houses. We have a property manager, so this rule doesn’t make sense to me. They let us finish out our policies, but they wouldn’t renew. Our agent quoted one company that doubled the cost we had been paying because the roof “may have been last replaced in 2000” (and we couldn’t prove otherwise). I said nope, and I asked another agent to give a quote. Their increased our cost by about $100, but it was better than $300. I executed that at the beginning of this month.

We had an HVAC go out, but luckily it was able to be fixed (for 225) than replaced.

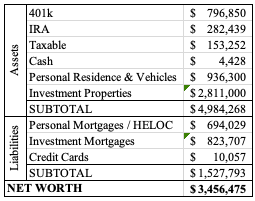

NET WORTH

Well, even though our investments are declining and we took on a lot more debt, our net worth increased by 75k from last month. Truly, I’ve focused on the work we’ve had to do over the last month, and not necessarily on the spending or the market. At some point I’ll need to get through all our expenses and identify how our spending has changed, but perhaps that’s a job for another season while we continue to work on a new house and work towards moving our family in the coming months.

We ramped up our travel this month, which has actually led to us canceling a few trips that were planned for this next month. I went to visit my family for my sister’s baby shower, we went on a family trip for a long weekend, and then Mr. ODA was gone all week for work. We’ve done a few local activities, but several of our plans have been cancelled or postponed due to the current gas prices, which are about $4.75. Even Sam’s Club and Costco, which were holding strong in the low 4s, are both at $4.69 right now.

We’re working towards closing on a new house next Wednesday, so that’s been the stressor right now. We had a month and a half for closing, which is literally the longest we’ve ever had, and then yesterday I got asked for tax information. Seriously, what have you been doing for the last month since I signed off on the initial disclosures? We went with an online bank, so that’s been an extra factor in uncertainty through this process.

RENTALS

I served a notice of non-renewal to one of my tenants. Her lease ends on 6/30, and we want her out. It’s the first time in 6 years that we’re so fed up with a tenant that we actually said it’s time to leave. We’ve had issues with tenants in the past, but we’ve just increased their rent as a means of giving them the option to leave, or compensating us for our frustrations associated with them living there. She, of course, didn’t pay rent by the 5th. When I asked her where rent was, along with the balance of outstanding late fees and the current late fee, she said she was trying to secure a place to live, so she wouldn’t be able to “pay towards that” until the 17th. Pay your rent timely OR communicate a need for more time without the landlord having to hunt you down. That will keep a roof over your head so you don’t have to move when you don’t want to, and it’ll also put you in a position where your current landlord can actually provide a referral at a new place.

My other usual suspect, who I told needed to start getting their act together and pay rent before the last Friday of every month, paid half of rent on the 3rd and sent an email saying we won’t get the rest until the last Friday of the month. Progress, I guess.

We had a massive issue with our property manager in Kentucky. The accountant felt he had a little too much power and ran with it. Mr. ODA went to meet with them, where the accountant had to admit his mistake in charging us $900 in front of the owner. As a means of making amends, the owner credited us the management fee they took out of our security deposit. While I understand their thought process that our contract says “10% of income,” and a security deposit gets counted as income for tax purposes, I disagree with them taking a commission out of it. If that’s the case, our security deposits under them should be 10% higher than a month’s worth of rent. A security deposit’s purpose is to reimburse us for our costs to fix a unit that has been unreasonable mangled by a tenant before their departure. In this case, we have $4000 worth of costs. The security deposit was $895. Them taking $89.50 was insult to injury in this case, especially after they took 18 days before taking any action to confirm the place was abandoned. Moving on.

That house that was abandoned ended up getting rented for June 1st. We’re netting about $250 more per month with the higher rent there.

One of our mortgages was going to be paid off in May, which I mentioned last month. I scrambled to find out how to pay the taxes, which wasn’t easy (it’s a different jurisdiction than most of our houses… being in the county instead of the city). I finally got that figured out and paid the taxes at the beginning of the month.

PERSONAL FINANCES

This month we actually had a few “receivables” to expect. We learned that our lender wasn’t requiring an appraisal (we don’t get it), so they were going to refund us the appraisal fee of $525. We had a major issue with Home Depot and getting an appliance delivered, which ended with us going to the store, buying the appliance, putting it in our car, and driving it to the rental. We had to wait for the terrible delivery company to “scan” the not-delivered appliance back into their warehouse, and then we got $600 back. When I registered my kids for preschool, the system glitched and charged an extra $100, so we got that back. I had already registered my oldest at the same school as this year before we learned we’d be moving, and they were kind enough to return my registration fees, so that was $300.

All that to say, stay on top of your finances. Know what you owe so that you know when you’re overcharged. When someone says you’re owed a refund, pay attention that you receive it; we had to follow up on the refund, and it turned out she hadn’t processed it. Don’t be afraid to ask if there’s an option for a refund in some cases. Just those transactions are $1525 worth of money back in our pockets in a month’s time.

SUMMARY

We have work on a rental that’s still outstanding. I don’t expect her to actually be out on June 30th at 5 pm like she’s been instructed. I have our property manager handling the move out (even though she doesn’t manage that property). This way, if she’s not out on the 30th, I haven’t driven 8 hours to find out I can’t do any work on the property.

We plan on doing a lot of work on our new house after close next week. That’ll take up a lot of our free time over the next few months.

The stock market has somewhat rebounded. It’s not back to levels it was once at, but it’s nice to see balances go up instead of down. Our credit cards are down significantly because I am purposely keeping a low balance right before we close on a house (down by paying it off, not down by not spending…). Our funds for closing are coming from our HELOC, so it hasn’t been a stressor to keep a cash balance to go towards our cash-to-close.

Building off of my last post about tenant abandonment, here’s what it took to turn over that unit. We rarely have units to turn over in our portfolio. Last year we had 1. This year we expected to have 1, but this abandonment made it 2. To have continued renewals over 13 properties is a blessing.

Usually, we need to clean and paint. Every once in a while, we have more work to do, but it’s rarely a massive undertaking. This one was a massive undertaking.

Our property manager walked through the house and saw that junk was left behind and it was filthy. There should be another word worse than filthy. I’m always surprised at how much damage someone can do to a place they have to eat and sleep in for two years.

This is a 3-story townhouse. The entry level is the garage and a den-type room; then there is a flight of stairs to the main living area of a kitchen, dining area, powder room, and living room; finally, there’s a flight of stairs to two nearly-identical bedrooms, each with their own bathroom. The two masters concept and a garage are benefits, but the two flights of stairs is a downside.

TURNOVER ACTIONS

The property manager had her maintenance staff remove everything left behind. I thought she was going to hire something like Junk Luggers, so I was pleased to see that this cost us less by her using in-house staff. They wiped down the baseboards, but didn’t clean. I was under the impression that it was going to be cleaned before I got there. I was also under the impression that the carpets were going to be cleaned on the 25th.

I was working weekends at the time, so I couldn’t get to the house until the 27th. I didn’t find the need to rush down there because I thought my property manager had action happening. Plus, I’m pregnant, so I didn’t want to be in someone else’s filth for extended periods of time, and I expected it cleaned up before I was scooting along the floors and in tight spaces. Well, I walked in and was so upset. The carpet was disgusting. It looked like someone made lines in the carpet with the steamer tool, but didn’t actually clean anything. Not a single thing was actually cleaned. The kitchen and bathrooms were horrendous. I’ll spare you pictures of what the bathrooms looked like. You can see “steamer” lines in the carpet, as someone had been there, but there was zero effort put into actually cleaning the stains.

I called the property manager, and she agreed to come meet me at the house. She agreed that the carpet cleaning was unacceptable, and I wouldn’t be charged for that. She explained that her guy didn’t have time to clean the place except for wiping baseboards, and they had decided to clean it once at the end. I said that would be fine if the house wasn’t this bad, but there should have been an initial cleaning. She showed me pictures, and even though the baseboards were gross, they had actually been wiped down because they had been even worse.

The property manager called her typically cleaner, and he agreed to get there the next morning. I showed up the next morning to find he was still there working. He said the house was in much worse condition than he was told, and they’d have to leave to go to another job and come back to this house. I wasn’t surprised, but I was very happy to see that everything was cleaned, and that I wasn’t completed grossed out by being there.

DECISION MAKING FOR TURNOVER WORK

There are costs that you just have to deal with in the turnover – junk removal, cleaning, carpet cleaning. Then there are costs that you don’t expect to be on your radar, but are necessary – replace broken floor vents, replace missing outlet covers. Then there are decisions that require more thought. For instance, we haven’t enjoyed this property in our portfolio, and we’re considering selling it. We’d like to recoup some of the costs we’re having to put into it now, but selling it is on our radar for the future. So do we want to clean the carpet, or start replacing the carpet with hard surface flooring to increase our property value for a future sale?

We recently received an updated assessment for our taxes on this property. I happened to look up their comps given. We bought this house for $86k. I noticed that the houses with no updates to it were selling around $110k, while houses with nicer flooring and fixtures were selling up to $130k. My goal was to start preparing for a sale in the future, and we’d have a few steps done instead of having to redo the entire house in a year or so.

The biggest actions I took while looking into the future were: 1) I painted the main floor baseboards white. The baseboards, walls, trim, and doors were originally all painted the same color – an off-white or beige. Over time, we kept the trend going because it made it easier and quicker to turn over the house. While I didn’t paint all the baseboards white, I did it in the main living area and in the stairwells. I painted the interior doors of the main living area (main entry door at the top of the stairs, the laundry room door, and the powder room door) and all their trim white. 2) Repaint all the main walls. At the last turnover, Mr. ODA went into the house and touched up the walls. The paint had gone bad, so the touch ups were very noticeable. I painted everything except one bathroom, half the laundry room, the powder room, and the two bedroom closets. Every other wall surface (including two stairwells…gosh) got painted a gray. 3) We did get a carpet cleaning company to come out and rotovac, which is an incredible process that brings a carpet in rough condition almost completely back to new. It’s truly impressive. They also charged us $159 for this more intense process, while the original company that just made lines in the carpet was going to charge $244 for nothing. 4) Instead of cleaning the main living area carpet, I wanted to replace it with hard surface flooring. We’ve had this house, with the same carpet, since 2016. That’s 6 years of carpeting that has been beat up (understatement) by 3 different tenants. The carpet could even be older than that because it’s what we inherited when we purchased the property. I explained in a recent post all the reasons why we laid LVP and how we accomplished it ourselves.

COSTS OF TURNOVER

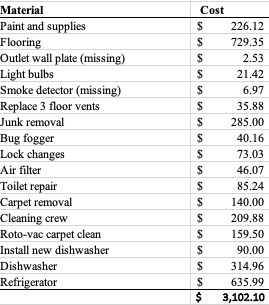

I had to supply my property manager with specific costs associated with the work I did, so here’s that, along with the charges they had on our account. Not all of this gets billed to the tenant. For example, the dishwasher and refrigerator were at its useful life and needed replacement, due to no fault of the tenant’s.

While it was hard to get started, seeing the mountain in front of me when I first walked into this house, I do appreciate having done most of the work myself. We spent over 28 hours at the house. I did about half of that by myself. Mr. ODA and his dad helped get some progress on the painting one day, and then Mr. ODA and I worked together on the flooring.

We also have the months of lost rent that were unexpected. With notice, we could have listed and shown the house before the current tenant vacated. We were caught on our heels, and we lost 2 full months of rent. Unfortunately, we truly lost 18 days of progress in those 2 months because our property manager didn’t enter the house to confirm abandonment timely.

LIGHT AT THE END OF THE TUNNEL

We ended up listing the house on May 6th. They had several showings, but the layout is hard to get rented. One couple submitted an application on a Thursday. When our property manager reached out to them, they never responded. Our property manager had pushed to list the house at $1250. Once that couple ghosted us, I told her to lower it to $1200. Just as I was about to give up and have it lowered, she was able to get another application and a signed lease. Luckily, being that it was May 25th, these people wanted a June 1st rental. We increased our rent by $275/month and only lost 2 months of rent, which is mostly made up by the drastic increase in rental income.

Another silver lining is that we paid off this property’s mortgage multiple years ago. Therefore, we didn’t have the extra “bleeding” of money by having to make two mortgage payments without having the cashflow to offset it.

We don’t expect to see a dime from the old tenant of what we spent to turnover the unit. We didn’t have any issues with him while he lived there, and his abandonment and lack of communication was surprising. Someone who leaves like that, and leaves the house in such poor condition, isn’t going to put forth effort to pay a $3k bill he receives in the mail. It’s in the hands of our property manager at this point and will likely move to collections. We’re just happy to have new renters in the unit and have this one behind us.

Most lease agreements state that you’re responsible for the entirety of the lease term, even if you try to leave early. Most landlords are willing to work out an agreement if you have a reason to leave the house early. We’ve let several people out of their leases early to either move out of the area or buy a new home (those are just the reasons we’ve dealt with, not saying those are the only reasons we’d let you out of a lease).

We usually default to two-months worth of rent as a “lease break fee.” You leaving early has increased our projected expenses for the house because turning over a house is expensive and you’re asking us to have more time without rental income. With that said, we’ve also left it at “you pay rent up until we get a new tenant in the house.” I’ve never taken more than a week to get a new tenant set up in a house, but my property managers (through companies, not the individual person we use in Virginia) consistently take 2 months to get a unit rented (I don’t get it!).

Then there are some people who just leave. No notice. No request. They abandon the property and stop communicating. Surprisingly, we’ve dealt with this twice in the last 6 years.

The positive, they’re mostly out of the house, and we can take action to get it re-rented, which is better than them living in the house while not paying rent. The negative, we’ve had no warning of their intent to stop paying rent. Plus, if a tenant is willing to just walk away from a house, s/he may not be leaving it in pristine condition.

ABANDONMENT #1

The first tenant abandonment ended well. In Virginia, if the house is abandoned for 7 days, it automatically returns to the landlord’s possession without the court getting involved.

I received a call from the public school system. They asked me if I was the owner and if so-and-so was living at this address. I truly could not answer. My property manager did the background check and set up the lease. I basically look at the lease to ensure the dates are correct and that all the initials and signatures are in place, but I certainly don’t commit names to memory. I gave the person my property manager’s contact. Connecting the dots, she must have confirmed the name of the tenant and the address because the tenant received notice that his children were no longer allowed to attend a school they were not districted for. This happened years ago. I always thought it was odd that they called in April to verify such a thing, when there was 4-5 weeks of school left. But then I was just telling this story last night, and someone said that if the kids are not causing trouble, they typically look the other way. So perhaps there was an underlying reason for the school system to go digging.

Well anyway, in true logical decision making, he blamed us for getting his kids kicked out of school. If I didn’t know his name, I certainly didn’t know how many kids he had or where he was sending them.

He let us know he was moving out, but he wasn’t cooperative. He said he’d be out by a certain date in May 2017, but he didn’t have everything cleared out. We finally got stern with him. By the end of May, he hadn’t paid what he agreed to, so we filed with the court.

We worked to get the house turned over in the last week of May, and we had new tenants move in on June 1st. We were only out 1 month worth of rent along with the costs of turnover. His security deposit covered a majority of the balance owed, so it wasn’t an immediate hit to our finances.

The court granted us the judgement. The total he owed was $1,074.76. Unfortunately, the judgement just writes the amount owed and whether interest is owed, but it doesn’t give a deadline for payment. The system expects the two parties to work together to make a payment plan. If he doesn’t live up to the payment plan, then we can go to the court and file for another judgement. We received $200 immediately from him, and then agreed to $200 every other Friday for the remaining $875.

He missed the second payment. We sent an email explaining that if he doesn’t reach out, our property manager will go to the court to file, which will then lead to a credit report hit and collections. He eventually started making a few payments, but I should have stuck to my guns and required 4-5 payments. In mid-November, he still had a balance owed of $685, plus 6% interest from the date on the judgement. We eventually got all the money he owed, but it took a year, and it was frustrating to constantly have to track him down and push him to finish the payment plan.

ABANDONMENT #2

The second abandonment just happened. In March, our property manager was tipped off by a neighbor that our tenant was moving out. Our property manager asked if he was moving out, and he denied it. Then he didn’t pay April’s rent, so she continued to follow up, but received no responses. I am not clear why it took until April 12 to decide to post notice to enter the property, and then why she didn’t actually enter the property until April 18, but that’s what happened. That’s 18 days of lost rent and lost productivity for us to turnover the unit. That’s $555 worth of rent that is just lost. We could have been working on cleaning out the house during that time.

Our property manager entered the unit and took pictures. She found that the tenant had left some furniture and garbage behind, but it was clear enough that he left and wasn’t returning. The house was also in bad shape. All the walls required a new coat of paint. The floors were filthy, as if things were spilled all over, never cleaned up, never vacuumed, and he left all the windows open for water to leak in. The kitchen was covered in fruit fly type bugs. The bathrooms were so horrendous that I refused to even be in the house until they got cleaned. It was impressively dirty. I always wonder how people live in such conditions. This is YOUR toilet. Why would you enter this room and think “yes, this is where I want to sit!”

The property management company had their staff remove the pieces of furniture and garbage from the house. Then they wiped down baseboards so that I could start painting. It was so bad when I entered that I had them get a professional cleaner in there before I’d spend much time there. I painted all 3 levels (including two stairwells), except for 1 bathroom and 3 closets. Then we got carpet cleaners in there and some maintenance items taken care of.

It was an extra 3 weeks worth of work that we did ourselves and coordination with contractors to get the house turned over. We lost April’s rent, and then we were set up to lose May’s rent. We didn’t get the house listed until May 6th, and then we didn’t get a confirmed renter until May 25th, for them to start a June 1st lease.

The silver linings here are that we improved the condition of the property over those 3 weeks; we could have lost even more weeks of rent, but we were lucky to find someone that wanted it nearly immediately; we have the unit rented $275 more per month than we had it leased for. Had we kept it rented through the end of the lease, we would have brought in about the same amount for the year that we’re bringing in now with the increase in rent, even though we lose 2 months worth of rent.

The tenant’s final cost, being billed for April, May, and June rent (I don’t know why the management company chose to include June), is $3,868.12. That’s after applying his security deposit to the balance owed. We probably won’t see a dime of that. If a tenant is willing to lie that they’re moving out, and then not respond to anything being sent after that, they’re not willing to work with us on a payment plan. We didn’t have any maintenance issues with the house, and we didn’t think he was unhappy with anything. Granted, I don’t know if our property manager was not responding to issues, but we weren’t aware of any. This house is in Kentucky, so we don’t have a grasp on how the court system works like we do in Virginia.

While it’s stressful and frustrating, eventually you move on. Once the house is re-rented, you start to feel better about the situation. Each day that you’re working on the house and each day there’s no application received for the property, you just keep building anxiety. While the first situation ended well in that we eventually received all our lost money, I don’t expect this second abandonment to end as well. Our long term (or more like 1-2 year short term) plan is to sell this property, so we’ll recoup that in the equity made over the last 6+ years with the house.

This has been a whirlwind of a month. Our crashing investment accounts have been offset by home values, so we’re still over $3 million net worth. But those investments are very low; it’s the first time I’ve seen a negative in my 12-month performance history for my ‘401k.’

HELOC

A couple of months ago, we were standing outside playing with the kids when a neighbor walked by and introduced themselves. Being that we easily have $150k worth of equity in our house, we started talking about how we should open a Home Equity Line of Credit to be able to float a future purchase. The process was initiated, but not really started, when we made an offer on another house to be our personal residence. More to come on that. But we close on the HELOC today at $100k, which was the maximum she could do as an “administrative authorization” (for lack of a better term, and to pull on my government background), which essentially just meant no appraisal cost.

NEW HOME PURCHASE

We’re about 3 weeks in being under contract on a new house. We’ve submitted all our files to an online bank that we’re using as our loan, and we’ve locked our rate at 4.0% on a 5 ARM. Closing is expected to be 6/15. We’ll need about $75k or 80k out of the HELOC for closing on that.

We found out that our appraisal that was ordered for this house got cancelled. A quick inquiry to our lender and we found out that they decided our credit profile doesn’t need one! They’re going to refund us what we already paid, which was a pleasant surprise.

PART TIME WORK

I worked the weekends in April at the local racetrack. It’s good money and only required 8 days of me actually working. This meet’s experience was slightly different, and I didn’t enjoy it as much as the Fall meet, but I made more than I did in during that meet.

RENTAL UPDATES

We had a tenant abandon a property on April 1st, so that was a lost month of rent that we weren’t expecting. Our finances aren’t in a position that we need that money. It also helps that we don’t have a mortgage on the property. But we still put over $2,000 into the house (including two appliances) and a week’s worth of our time in turning it over since it was left in poor condition. We’ve been fighting Home Depot on getting a dishwasher delivered and installed, and that still isn’t resolved.

We had our usual suspects not pay rent on time. One did manage to pay in full (not the late fee though) by the 7th. The other I finally told that paying on the last Friday of every month is no longer acceptable, and it needs to change. She sent a nice email back, but we still haven’t seen a dime from them this month.

We had one rent increase go into effect; it went from $1025 to $1100. That also increases our property management cost by $7.50 going forward.

We had an insurance company drop us by not renewing us since they found out we moved out of state. We told them we have a property manager, so there is someone available taking care of the houses, but they didn’t care. Luckily, not all insurance companies have such a requirement, and our agent was able to find someone with nearly the same price that accepted a property manager.

We have officially paid off one of the loans that we had with our partner. We had intended to pay the loan off this month, on our terms. Instead, because the balance was about $400, the loan company took it upon themselves to use our escrow and close the account. We were purposely waiting until after escrow paid the taxes due this month, and now we need to scramble and figure out the tax payment.

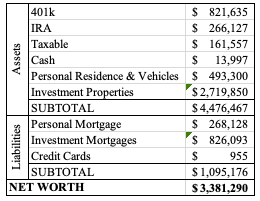

NET WORTH

SUMMARY

We now commence a very busy time of life. We have several trips planned, we expect to turnover a rental that we’re kindly asking a tenant to vacate, and we have a lot of work we want to do on our new personal residence. Hopefully the turnover of the one house goes smoothly, we get the house that was abandoned in April re-rented, and that there are no more surprises in our rental world. We also had our AC go out in our 18 month old house, so here’s to hoping there are no more surprises in the personal expense world too.

The market has recovered a good bit, so our net worth jumped. Our retirement accounts were at an intriguing low, but they’re back on track now. We also saw a few sales in the neighborhoods where our rentals are, so that increased our net worth based on the comps. We added a new property over the course of the last month as well.

NEW HOUSE IN OUR PORTFOLIO

We closed on a new house on March 24th. We worked on it for a few days, I held an open house, and we were able to get it rented as of April 8th. We had 16 days of vacancy. While showing it, most people were looking for a May or June start date, so we were lucky someone qualified for an April date. Back in 2016-2019, we were looking to follow the “1% Rule.” That means that if you buy a house for $100,000, your goal is to set rent at least $1,000 per month. This house isn’t even close. This market doesn’t allow for such a goal anymore because housing prices are soaring. The next goal would be to list for about $1/square foot. This house is 2100 square feet, but since the upstairs has smallish rooms and the basement is all open, we thought it wasn’t really worth pushing for $1/sf.

We bought it for $240k net, and ended up renting it at $1750. I wanted $1800, Mr. ODA wanted $1695, and when I went to list it, Zillow suggested $1750, so we went with that. Multiple people commented on how they appreciated the price, so we may have been able to get $1800 without an issue. I’m happy to have it rented, and I think these people are going to take good care of the house.

RENTALS

We put more money towards the house that we’ve been paying off, which is owned with a partner. We put our half towards it ($8,500), and it has a balance of about $600 now. The pay off quote required us to pay the anticipated taxes that will be paid out of escrow in May. We didn’t appreciate that, so we just went ahead and paid it down. We’ll let the May mortgage payment go through, wait for the taxes to get paid out of escrow in mid-May, and then pay it off. That’ll make 7 houses that are owned outright! But that also means I need to stay on top of insurance and tax payments.

We were just informed that one of our properties in Lexington that’s under a property manager hasn’t paid rent. She said it’s unlike them and that they aren’t even responding. She’s going to go to the house tomorrow to check on the situation. Since we’re paid a month after rent is received, this hasn’t affected us. A neighbor reported that they were moving out last month, but the tenant denied it. Perhaps they abandoned the property.

Once again, our two usual suspects didn’t pay rent on time. However, both of them actually made a better effort than they have been. One has paid this month’s rent in full, but has a balance of $286.31 (seriously…) to make up several late fees. I’m happy to waive late fees when it’s someone who communicates and isn’t always a fight to collect rent, but I’m holding this one to the balance owed. Another one told me that they wouldn’t pay until the last Friday of the month. I drafted an email to tell them that this is unacceptable because it’s been several months that they’re paying this late, and we need to work towards getting back to paying rent at the beginning of the month. Right after I drafted that, she sent half of this month’s rent. Better than nothing!

SPENDING CHANGES

Over the past month, we didn’t go out to restaurants very much. We haven’t been traveling because my family came into town for our daughter’s birthday party, and then I’ve been working on the weekend. Most of our spending went to gas (going back and forth to Lexington (half hour drive) multiple times per week!) and expenses to get the new house ready for a tenant.

I’m flying to my sister’s baby shower next month, so that another large and unusual expense on our credit cards ($250).

SUMMARY

We still have our state taxes to get paid. We went through the process of entering all our taxes, but we haven’t hit submit just yet. Surprisingly, we’re expecting a refund from the Federal side. The amount owed and the refund basically end up as a wash.

Our new property’s loan is a commercial loan, so it doesn’t get paid on the typical mortgage schedule, but on the 1 month anniversary of the opening. Therefore, the next payment is due on 4/24, and there’s no “1 month without a payment” type thing.

Clearly, our cash balance dropped significantly since last month because we had the closing. That was about $46k that we wired out, which was the expectation when we completed all the maneuvering with the cash out refinances in January. Our credit cards reflect our lower spending too, coming in about half what the balances were last month.

When looking to rent your house, you should do your due diligence. Our concerns are whether a person has a history of late payments, collections accounts, and if they have a criminal history.

We do two steps of initial screenings before asking a tenant to pay an application fee. The first two steps given them the opportunity to disclose anything that may be seen as unfavorable or not meet our rental criteria. This way, once they pay the application fee, it’s a verification step, and they’re not wasting any money for me to find out that I’m going to decline them.

Here are the details of how I go through the evaluation process, and specifically how I just did it for our new rental.

RENTING CRITERIA

First, I send everyone interested an “Interest Form.” We ask for their legal name, contact information, credit score, employment data, number of occupants, whether they smoke, if they have pets, if they’ve been evicted, and if they’ve been convicted of a felony. I also ask them to provide any other information they think I should know that may affect their ability to rent the house. I send this form to everyone who expresses interest, and it’s the first step before scheduling a showing. I request the data before scheduling a showing because I don’t want to waste my time or theirs showing the house, when they had adverse responses to our criteria. This was more important when I was scheduling individual showings, but I now conduct an “open house.” I set aside two hours to be at the house and ask they come during that time. If that doesn’t yield a tenant, then I’ll evaluate who couldn’t make it and field new requests to see it to determine if I’ll show it individually or host another open house.

We have this at the top of our Interest Form.

Properties are offered without regard to race, religion, national origin, sex, disability or familial status.

Required standards for qualifying to rent a home are: • Each prospective applicant aged 18 or older must submit a separate application. • We limit the number of occupants to 2 per bedroom. • Your combined gross monthly income must be at least $4,000. • You must be employed and/or be able to furnish acceptable proof of the required income. • You must have a favorable credit history. • You must have good housekeeping, payment, and maintenance references from previous Landlords.

Compensating factors can include additional requirements such as double deposit and/or a cosigner.

Our typical rental actually requires 3x the rent as the monthly income, but since our last house was more expensive, we put the requirement as a dollar amount threshold instead.

Then I would historically review those who say they’re interested and pick the one that appears to be most qualified. I’d send them a “pre-application” form to fill out. However, for our last tenant search, I asked everyone interested to fill out the “pre-application.” The tenant screening system doesn’t tell me their last landlord information or their employer, which are both necessary for making phone calls and checking their information given. The “pre-application” repeats some of the questions on the Interest Form, but the pre-application requires them to sign the form as an “affidavit” that the information is accurate.

If they tell me that they’re going to have a low credit score, it helps me to know the reasons for it up front. Additionally, by letting me know any issues up front, it saves them money. If they self-report that they have several collections accounts, then it could be cause for me to move on to a different person interested. If they don’t tell me that they have some issues in their history that may be unfavorable, and I send them the application, then they’re spending $40 per person only to potentially not get the house. I prefer to use the online tenant screening as a final verification step than an initial screening and potentially waste someone’s money.

One time I got through all these steps, had 3 different people submit an application for a house, and the report came back with an eviction. We asked why they didn’t disclose that to us originally. They told us a story about how they were asked to leave somewhere, but they didn’t know that it was reported as an eviction. We told them that they were disqualified. We went with our “runner up,” and they’ve been in the house almost 3 years without any issue or late payment.

We also had two people submit an application and then a bankruptcy was reported on the credit report (it was before the pre-application step I implemented). She said she didn’t see a place to explain a bankruptcy, so she didn’t think to mention it. For future reference, if I ask for your credit score and you have anything concerning in that credit report, it’s helpful to be upfront about it. In that case, everything else was fine and her explanation for the bankruptcy was clear and thorough. We gave them a chance, and they were amazing. She was rebuilding her life after taking on a lot of new bills after a divorce, juggling single-income life, and it was a way to consolidate the debt.

DECIDING BETWEEN TENANTS

In this last situation, I had several people express interest in the property.

I held the open house, and I asked everyone to let me know by noon the following day if they were interested in pursing an application after seeing the property. I received 6 or 7 people who were interested in the house.

I don’t look at one factor. I weigh all the information given to me in my head. In a perfect system, I may assign a weight to each data point, but that’s more effort. I’m reviewing the data and trying to see who has the best, well-rounded criteria.

The house is big (2100 sf with 4 bedrooms), and rent is higher than anything we’ve ever managed. I looked at what they are currently paying in rent. If they’re currently paying $1500 per month, then that made me more confident that they’d cover the $1750; if they are currently paying $400 per month, then I was concerned that they weren’t prepared to cover such a large expense difference. Along those lines, I also gave more credit to someone who has a stable job that they’ve been at for more than a year, versus a few people who said “I’m starting a new job at the end of April.” We have a tenant that goes through jobs every 1-3 months and is always a pain with rent, so I’m probably more scarred by job history now.

I gave more credence to those who had at least a 600 credit score, but I didn’t rule out anyone with a credit score less than that. One woman did have a lower credit score, but she had other good information, so I didn’t rule her out.

Finally, the determining factor came down to availability. My top two contenders had different desired move dates. One said early April, and another said June 1st, but May 1st may be ok. When I asked her to explain about her move date, I received a detailed story that didn’t have any conclusion on when she was available. Since this is a business, and I had a qualified group interested in the house sooner than others, they were the ones selected. If I didn’t have someone qualified for an April move in, then I would have waited for a May 1st rental instead of lowering my standards.

Luckily, I had enough interest in the property that I could select someone who was well qualified and get it rented sooner than later.

APPLICANT SCREENING

Once I’ve given someone these two opportunities to disclose unfavorable information in their credit or criminal history, and they’ve provided favorable responses that meet our criteria, I send the link for the application. The potential renter enters their data into the system, which helps keep their information secure (e.g., I don’t have their social security number) and helps eliminate any typographical errors that I may make transferring the information into the website instead of them entering the data they already know. Additionally, the tenant pays the fee (currently $40) directly to the website, which helps them understand that once the report is run and the fee is paid, it was for a service so it’s not refundable. I heard multiple stories this past week where people paid “application fees,” but were later told that they weren’t the first to respond. That’s not fair. I don’t need to know everyone’s detailed reports and cost people money if they aren’t going to get the property. So here’s how I handle the tenant screening process.

The system generates a report for me to see that includes their credit history, criminal history, eviction history, and income verification. – The credit history shows any missed or late payments; collections accounts; bankruptcies filed with the chapter, date filed, and amount settled; and their score. I’m more concerned about late or missing payments than anything else there. The collections accounts are typically related to medical bills, but if they’re for general credit cards or an enormous car loan, I’d find it more concerning. I’ve also not ruled someone out simply because they’ve filed bankruptcy; two of our tenants actually have a bankruptcy in their report. – The criminal history tells me if they’ve had any judgements against them. I’ve seen traffic violations, misdemeanors, and felonies. The report also tells me if they’ve been listed on any sex offender registry. If they have felonies, multiple misdemeanors, or are on a sex offender registry, it’s automatic disqualification. I’ve gone down the road of giving people chances, and it hasn’t gone well. This report isn’t fool-proof either. I know how to use the court record system where we have most of our houses, and I now look them up in all the nearby jurisdictions to be sure there’s nothing reported. – The eviction report will tell me if they’ve been formally evicted. This doesn’t capture any times where a tenant and landlord agreed on the tenant’s departure outside of the court system. This also may miss some jurisdiction evictions. We had someone show up in a separate jurisdiction when I went looking for their information in the surrounding areas, but it didn’t show up on the report. Don’t think that this report is fool-proof. – The income verification comes with a built-in caveat. I don’t know the details on how the report is run, but the result is something along the lines of “we believe that the self-reported income is near accurate.”

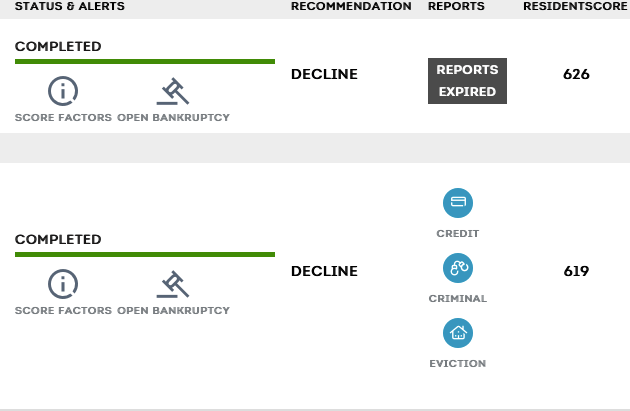

The report suggests whether to accept or decline the applicants. I suggest reviewing the data and making a decision for yourself. Some reasons why the recommendation will be to decline include: criminal history, bankruptcy, and low credit score.

We have given several people “chances” that don’t perfectly meet our criteria. Below is a screenshot where the recommendation was to decline. However, we ended up asking for more information and giving them a chance. They ended up spending a year in a rental of ours, moving out of the area, and then asking for our rental availability when they came back to town. They always paid on time, hardly asked for anything, and took great care of the house.

We have also accepted tenants that had some concerns in their report, but the system recommended we accept them. We tried to overlook the issues, but we’ve ended up regretting it. We have one tenant who has a criminal history (forgery) and we ended up having to release her roommate from the lease because of a domestic violence and restraining order issue. She’s also consistently late on making rent payments and doesn’t keep communication lines open. We plan to ask her to leave at the end of this lease term. We also had a tenant with a 480 credit score who wrote us a letter about her low credit and asked for a chance. She ended up consistently paying late (she always paid, but it was always a fight); we threatened eviction when it got to a breaking point where she was combative, but she left on her own terms. That’s a good example where she was a terrible tenant, who we gave multiple opportunities and even restructured her rent, but her eviction report won’t say anything to that effect.

DEPOSIT

Once I have an approved application, I request a deposit to hold the property and remove the listing. Typically, the lease signing doesn’t occur immediately. In those cases, I want protection of my cash flow that I’m holding the property for someone specifically. I’ve had a couple of houses that have signed a lease immediately, but typically there’s a lag between “acceptance” and the lease being signed (forming a contract).

In this last instance, the tenant was accepted on Friday, but the lease wasn’t going to be signed until the following Thursday. I requested a $400 deposit, which will be applied to their balance owed to get the keys transferred to them. I originally was going to request $500, but I realized that the week’s worth of time at the rent per diem rate came to $408. If they back out between now and Thursday, then I haven’t lost income if I had chosen someone else and not held the property until the date they wanted a lease. Ironically, they ended up paying a deposit of $500. For them to obtain the keys, they owe a security deposit ($1750), the first month’s pro rated rent (about $1300), and a pet fee of $500. Their total is $3,550, but the $500 I’ve already collected is applied to that balance. Therefore, on Thursday, they’ll owe me $3,050 for me to hand them the keys.

Usually, I require the first month of rent to be the full amount, and then the proration is applied to month 2. Since for this tenant, they already paid rent at their current address for the month of April, and the rent here is higher than our average, I went ahead and prorated the first month so they didn’t have to put so much cash out of pocket in a short period of time.

SUMMARY

You can see how I am not making black-and-white decisions. I’m not hanging my hat on one or two factors. I’m being reasonable in my decisions and understanding that there’s a person, and maybe a family, on the other end of this transaction.

Be fair. Utilize a variety of factors in making your eligibility determination. Keep your communication lines open with potential renters until you have a deposit and/or lease signed on the property.

Treat this as a business and make informed, logical decisions instead of emotional ones, but be reasonable.

We closed on a new type of loan last week. It wasn’t a completely smooth process, but it was easier than a residential loan.

WHY COMMERCIAL?

Residential loans on second+ properties were over 4.5% on their interest rates last month. The commercial loan gave us options that were lower than that. It comes with a catch though. While the loan is amortized over 25 years (there was a 20 year option too), there’s a balloon payment after 5 years. There were also 3, 7, and 10 year options. Being that this was our most expensive investment property purchase, 3 years was too much of a risk to take on that balloon payment. The interest rates for 7 and 10 years didn’t make it worth going the commercial loan route. While the interest rate is fixed (unlike in an ARM or adjustable rate mortgage), this balloon is a risk.

By going through a credit union, our costs were also minimal. Our closing costs were just over $1,000, rather than the typical $2k-3k that we’ve seen on closings that cost less than half what this house cost us.

The only other “catch,” if you want to call it that, is that there is no escrow. I already handle the taxes and insurance payments on my own for a handful of our houses, so that’s not a big deal. I also appreciate having control over my money instead of having to check in on escrow regularly and making sure all the escrow analyses are actually done correctly (because one recently wasn’t!)

PROCESS

We filled out an application, which they called the “personal financial statement” and included our detailed financial status. It had me list all our account types and balances. I assume that’s what they used to compare against our credit report, because we actually didn’t send any account statements to them (glorious!). We had to provide the last 3 years of tax returns (ugh… we haven’t done 2021 yet so we had to give 2018).

I developed a rent roll and gave that as well. It listed all real estate owned, purchase price and date, current market value, monthly rent, mortgage balance, monthly mortgage payment, and whether or not it’s occupied. I added the HOA payments on the houses where it’s applicable because that always seems to be a last minute request for documentation.

Once the application was completed and reviewed, that was it. We were asked a few follow up questions about the numbers on our forms, but we weren’t asked for anything further. Essentially, “underwriting” happened as part of the application process, versus in the middle of the application and closing dates, spanning days and maybe weeks of documentation gathering and answering of questions.

Instead of a “rate lock,” the rate given is the rate that was present at the application submission, pending any exceptions (e.g., if credit isn’t what we said it was or we have outstanding loans not disclosed). As an auditor, it was hard for me to accept that we weren’t going to be hit with a surprise somewhere along the way because we never signed anything agreeing to loan terms!

We saw no documentation until the Monday before our Thursday closing. There was no initial disclosure, and no “rate lock.” We had no idea how much the closing costs actually were going to be. The responses to our questions were slow or nonexistent. We didn’t see our appraisal until the Friday before closing. Not knowing the process or knowing when we’d find out how much this was costing us was more than we’re used to handling emotionally.

We received the HUD settlement statement on the Monday before closing. Luckily, everything was correct. Our sellers had already moved out of the area, so we had to have the statement sent to them, signed, and sent back to the Title attorney. They did that perfectly, and we had an easy closing on Thursday. We signed all the paperwork in about 20 minutes!

FIVE YEAR LOAN

Mr. ODA ran some numbers to show me why we should go for the 5 year loan instead of the other terms.

We didn’t consider the 3 year option because we didn’t want to manage that balloon payment or refinancing so quickly.

As a reminder: the closing costs for the commercial options are the same regardless of the term, and were about $2k less than the traditional loan; all the commercial loans are amortized over 25 years, but have a balloon payment at the end of the term given; all are based on 20% down (because there was no incentive for 25% down).

The final decision to go with the 5 year loan was that we haven’t shied away from risk in the past, so take the incentives that come with the shorter term (i.e., lower monthly payment and less interest paid). Our portfolio has made drastic changes over the last 5 years. Therefore, we don’t see a reason to pay more interest, reduce less principal, and have a higher monthly payment (thereby lowering our monthly cash flow) just because a balloon of $167k is concerning.

BALLOON PAYMENT

The loan is $193,600. After 60 payments (5 years), the principal balance (with no additional payments made) will be $167,500.

Let’s face it, if we had $160k+ liquid, we wouldn’t be paying the first 5 years of interest on the account. We can make additional principal payments over the next 5 years to dwindle the balance before the balloon payment is due, and/or we can look into refinancing the balance at the end of the 5 years.

We had another private loan that had a balloon payment at 5 years. That loan was originated at about $70k and we paid it off in about 3 years. We had several issues with that lender, so we had the incentive to throw money at the loan and be rid of it, versus attempting to refinance it at the end of the 5 year term.

It’ll be interesting to see what we do on this going forward. The balloon payment would typically be an incentive to make additional principal payments. However, we have six other loans with an interest rate higher than this loan’s, and one loan with the same interest rate. We’ve been focusing on either the one with the lowest principal balance or the one with the highest interest rate. This new loan doesn’t fit either of those categories!

SUMMARY

Mr. ODA asked me if I would do this again, and I would. It was frustrating to ask someone in customer service a pointed question and not get an answer, but overall this was easy. There was minimal documentation needed, the requests didn’t drag on, and the closing costs and interest rates available were favorable. The balloon payment is something that needs to stay on your radar over the next 5 years (and mostly in that final year), but refinancing is always an option. It doesn’t mean that you have to be ready to fork over $167k on that date, but you do need to plan for closing times and ensure you keep your credit worthiness in good shape (although isn’t that always the goal?!).

We have been surprisingly busy around here. I’ve been juggling a few rental issues, staying on top of some billing issues, and trying to make it through a commercial loan process.

At one point, most of our loans were held by one company. That was a more simple life. Even though we’re down to 6 mortgages under our name, it’s through 5 different companies. I’m really struggling keeping up with them and getting in a groove after our most recent refinance. I’ve mis-paid things 3 times now. I’m always on top of our payments, but something just isn’t clicking right now for me. I just paid one of our mortgages due April 1 instead of changing the date to be an April pay date. At the moment, we have a buffer in our account because we’re getting to this closing next week, but we usually don’t, so hopefully I have this figured out now that I’ve made so many mistakes.

RENTAL PROPERTIES

LEASE RENEWALS

We had 3 properties process their renewals this past month. Each of them had cost increases to their lease renewal (875 to 950 effective 5/1, 850 to 900 effective 8/1, and 1025 to 1100 effective 5/1). We have another property that will have a renewal offer go out this week. Then we have 3 that will need action by the end of April because the leases expire 6/30, and one that will need action by the end of May because it expires 7/31.

MAINTENANCE

We had a tenant reach out to us that they found bugs in their bathroom tub. She sent pictures and, sure enough, they were termite swarmers. I have way too much experience with termites. I called our pest company, and they sent someone out for an inspection to confirm they were termites. Then I got a call that because we didn’t pay the annual fee to keep our warranty current for the last 3 years (we had the house treated for termites in February 2019 when we bought it because there were active termites and extensive damage by the front door that needed repaired), they could charge us $650 again. However, since we’re considered a business account, she’d be happy to let us back pay the termite warranty and they’re treat it. So I paid $294 for the treatment instead (split with a partner on this house). She also informed me that they had cut off the hot water to the kitchen sink because there was a leak. I don’t know why tenants don’t tell us these things right away! I had my plumber out there the same day, and he replaced the whole faucet. That was $378. That’s one of those charges that’s frustrating because we could have replaced the faucet on our own, but we don’t live there anymore. Oh well; it’s also a cost split with our partner, so that helps.

We had another tenant reach out saying that her kitchen sink drained slowly. She’s been with us since we bought the house and never asks for anything. She’s on top of communication and was super appreciative each time we agreed to renew her lease. We had done a huge sewer line replacement project at this house, so I was skeptical of the issue. It turns out there was a plastic fork lodged down there, but I just let it go (meaning, she’s then technically responsible for the cost). Our property manager let her know that if it happens again, she’s financially responsible, but we’ll cover the cost ($200) this time.

RENT COLLECTION

We FINALLY got the check for one of our tenants that had an approved rent relief application. They submitted an application in November to cover December, January, and February rent. By mid-December, they ended up paying December rent because they hadn’t heard (and the application expires, meaning their protection from eviction expires (not that I would have pursued eviction for this group because they’ve been great tenants for several years)). They received approval for 3 months worth of rent and 2 late fees on January 11. We received the check on March 4th. So frustrating in that process, but still better than an October approval and us getting those 3 months paid at the end of January.

We had our usual suspects not pay rent. On the one house, they didn’t tell us they weren’t paying rent for the longest time. Now, they tell us they’ll pay us on a later date. I let it go this month, but with them paying on the 23rd, that means we’re in a perpetual cycle of not getting rent on the 1st. We have a partner on this house, so I plan to address it next month if they claim another 3+ week delay in getting us the rent. On the other house, she let us know in February that she’d struggle to pay rent and she gave us random amounts throughout the month. I let her know she was still $106 short from February and that she was now in default of March’s rent, and I got no response. Then Mr. ODA had $1000 show up in his account on Friday. She still owes $371 between the two months, but at least we have the mortgage payments covered. She’s also the tenant that we plan on not renewing her lease because she’s caused issues throughout her tenure.

BUYING A NEW PROPERTY

We’re still in the process of getting through closing on a new rental property. We’re expecting to close not he 24th, so we’ll see how that goes. It’s a commercial loan, and it operates different from residential mortgage underwriting, so we’re in the dark. Communication has been next-to-nothing. We’re currently waiting on the appraisal to come back. That was our one hurdle to getting into the house. I said once the appraisal clears, then we (as the buyer) shouldn’t have any risk in getting to closing. Therefore, we were hoping to have the house painted before we close (I would do the painting), then we could refinish the floor and get the rest of the cleaning done the weekend after closing, and get it listed for rent for April 1. I suppose I wouldn’t be trying to get to the house before Friday, so I guess I can be patient and wait to see what happens with the appraisal for a few more days (even though the appraiser was on site last Tuesday, and I’ve never had it take more than a day or two to get the paperwork).

REFINANCE FOLLOW UP, STILL

We still have an issue with the mortgage that I ended up paying 3 times for the 2/1 due date. Our refinance was difficult, and the communication continued to be difficult after closing. I asked on 2/1 whether our loans had been sold yet because I was surprised I hadn’t heard. Usually, I see a note saying to pay the new company before the first payment, thereby not paying the first payment to that “first payment notice” place that comes with the closing documents. The company’s contact said to keep paying them because they hadn’t sold the loans yet. I didn’t open the attachments in his email because I assumed he was reiterating what he said in the email. Turns out, one of the loans was already sold, and I should have paid the new company. Well, I processed a paper check to go to a completely different company (started with a C, and I didn’t catch that I selected the wrong one in bill pay). Luckily, that company sent us our check back, saying they think our loan is closed with them and they can’t process the payment (thank goodness we once had a loan with the address I put in the memo line so they could clearly make a connection and say “we don’t want this!”). When I noticed my mistake on the 14th, I sent a handwritten check that I rushed to the post office at 4:55 to get post marked. In the meantime, I found out that I was able to set up an online account with the new company even though I didn’t have the loan number yet (they gave it to me over the phone). I paid the new company online to make sure I didn’t have anything on my record claiming I didn’t pay by the 15th and it was late. I figured I’d rather manage 3 payments being made than fight the credit companies to change my credit report. Well, the initial company cashed my handwritten check, but they still haven’t sent the money to the new mortgage company. They just kept telling me they have 60 days to get it to them, and I said that’s unacceptable that they’re holding my money. That was a week ago that I was told I’d get a call back, and I haven’t heard from them.

PERSONAL EXPENSES

Now that the basement is done, I had a strong urge to finish projects. There were several things that were starting but not completed. Those final punch list items always seem to take forever. I was impressed that Mr. ODA pushed to get some of the things in the basement done right away, even though they weren’t on a critical path. However, I didn’t uphold my end of the project by painting those things, so I got back to that. I mentioned several of the projects in a recent post, and I’ve done a whole lot more since that post. But all that to say, I’ve spent a lot of money in the last month. I bought a lot of supplies to finish off these open projects. I also had big purchases of cabinet hardware, a dining room table, a desk, and a wood. We haven’t done very much out of the house, so we don’t have a lot of other expenses than these projects, which means our credit cards are actually have the usual balances. We did book an AirBnB for a trip at the end of the summer with friends of ours. That was a big hit on the credit card for a week at the beach, but they reimbursed us for their half.

SUMMARY

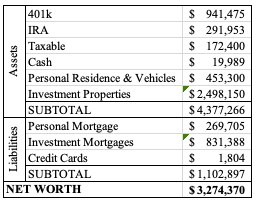

It feels like I just keep lowering the balance in our investment accounts each month, but I went to look at February 2021 to see the total. Even though some balances have decreased, we’ve still contributed to the accounts, so overall they’re $21k higher than last year, which is encouraging. I guess I should also focus on the property values raising significantly. We’re over $500k higher than last year in our assets, and our liabilities (i.e., mortgages) are about 13k less than February 2021. We’re also still over $3M on net worth, even if we’re hovering right around that. We’ll add about $50k to our net worth by the end of the month, as long as we close on the new property on time.

I have gone through all our expenses in 2021 and categorized them, which was very time consuming. I swore I’d do better this year, but it’s March, and I haven’t done anything.

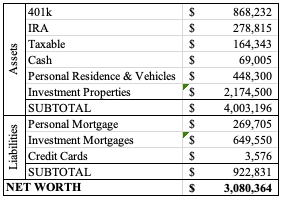

In the past year, we hit a net worth of $3 million. That’s really exciting, but we have more goals. It’s important to note that the net worth is through our investment properties, retirement accounts, and other investment accounts, so it’s not liquid funds. The values on our properties have drastically increased, many of which we’ve recently refinanced and have an appraisal on file showing just how much equity we’ve gained on these. Except for the cash that we have in our savings account right now, as we prepare to purchase another property at the end of the month, we don’t typically carry a cash balance. Our philosophy is that, if there’s an emergency, there are very few things that can’t be put on a credit card, and we can liquidate investment funds within 24 hours. We don’t subscribe to “3 months worth of expenses in savings” type actions. We’ve had plenty of large expenses hit us with rental properties, fertility treatments, and other random health needs, but it hasn’t ever been something to drown us financially. So while it’s exciting to see that new net worth, it doesn’t change our spending philosophy.

DIVIDENDS, INTEREST, & REWARDS

Mr. ODA used to have our dividends get reinvested automatically, but now they are transferred into our checking account. That was over $6,500 that came in, mostly at the end of the year, but there was ~$30 per quarter deposited also. In a different time, interest earnings on accounts used to be something to be excited about. Our checking and savings account combined brought in $6.51 for the year.

Mr. ODA is set up with GetUpside. When I went to their site to get a better description, I learned that you can earn cash back through gas, grocery, and restaurant purchases; I thought it was just gas. It’s an app that allows you to earn cash back through your normal purchasing. However, it also gives you an incentive for referring people, and so when that person buys gas, you get some cash back. By checking the app for a participating gas station (and only using it if the incentive offered is a better price than surrounding gas stations), Mr. ODA deposited $32.45 for the year.

Between 5 credit cards, we brought in $4,232 worth of rewards. These are simply earned by either spending or paying the credit card, no further action. We preach and preach to have credit cards with rewards. Everything we purchase goes onto a credit card; at the end of every cycle, we pay that credit card off. We’ve developed a mindset for spending that means we’re not afraid of what we put on the credit card and whether we’ll be able to pay it off in full at the end of the month, because we’re not spending frivolously. I will caveat that this amount of rewards was possible due to sign-on bonuses that were earned in a previous year, and then the credit card changed their reward redemption options, allowing us to pay ourselves back for restaurant purchases. We had previously been using the rewards to purchase travel needs through their portal, but we were able to dwindle down our rewards with this reimbursement change.

INVESTMENTS

Every month, we each put $500 into our investment accounts as an automatic contribution to max out our Roth IRA contributions. Additionally, each kid gets $50 deposited into their investment accounts each month. We also received the child tax credit each month, so with that, we put $125 into each kids’ account. The thought process was that we received $600 for them, and so after investing in their accounts, we were left with $350 to go towards “raising” them, which was the intent of the money being sent out in advance.

EXPENSES

My categories were super broad. For instance, if we traveled, I included all the expenses (e.g., lodging, flight, activities, parking, dog-sitting) as “entertainment.” But “entertainment” also included watching horse racing, baseball game, zoo, babysitting, etc. “Home” includes any furniture purchased, decorations, cabinet knobs, pictures/frames, etc. Even with the broad categories, I still had too many.

There are 3 categories that we have more control over, so I took a closer look at them: groceries, gas, restaurants. These are the ones that we can control our actions to change if we wanted/needed.

GROCERIES

A shortfall on my tracking is that I don’t know if Walmart purchases were necessarily for groceries or for something else. I removed a $300 purchase from my list because we wouldn’t have spent that much in one transaction in groceries, but I can’t figure out what we did spend it on because it was too long ago.

I investigated the spike in June, and I didn’t come up with anything jarring. There’s a transaction for $165 on a day with another transaction, so that may not have been food. August had several trips to Kroger. Trips to Kroger mean that we’re buying in bulk, so things purchased there are typically several of a particular deal they’re running that week versus an actual grocery shopping trip. There are 19 grocery transactions in August, which is higher than usual. August also included an emergency “find this kid some medicine while we’re on the road” that cost us $8 worth of medicine.

Lesson learned: We can do better meal planning and making fewer trips to the grocery store. We can be more deliberate about what we’re purchasing instead of stocking the pantry without a plan. We have a Sam’s Club membership and sometimes we tag along to Costco to scope out deals, so those lead to more bulk purchases, which will fall by the wayside in 2022. The Kroger deals will continue to be on Mr. ODA’s radar though.

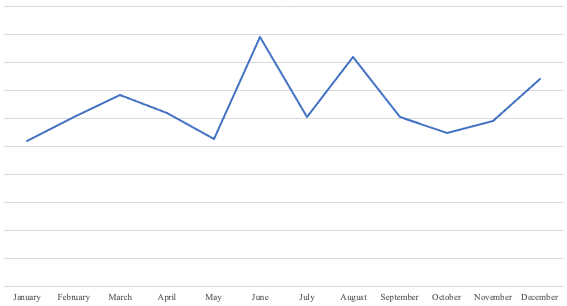

GAS

Interesting that January through April are so much lower because we didn’t necessarily stay home. We drove about an hour away for a trip in January and a trip about 90 minutes away in March, went from our house to Lexington (about a half hour) every weekend, and went to the zoo (about an hour or so away). I guess we stayed home during the week more, which kept our gas costs low. April was when we gave up on a lake house and decided to be deliberate about going on trips, so I expected to see an uptick in gas costs at that time. I described that whole thought process and what we did in this post. Some of the uptick in certain months can also be contributed to us trying to maximize gas prices (e.g., we fill up if we’re going to be near Costco, even if we don’t necessarily need the gas at that time). In October and half of November, I was working in Lexington on the weekends, so that was 3 days a week that I was driving 25 minutes each way. Then in December, we drove from KY to Long Island, which is a whole lot of gas.

Lesson learned: We like to be active, so I don’t foresee a change in our gas-purchasing patterns in this year. As I type this, gas prices are soaring all over the country. Since we like to travel, our trips are usually within driving distance versus flying with two kids, so spending the money in gas is cheaper than 3-4 plane tickets.

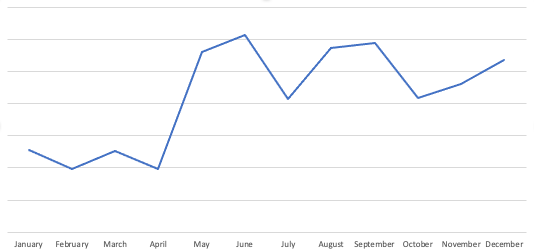

RESTAURANTS

This is a funky one to track. While we’re traveling, we’re clearly eating at restaurants more often. That’s seen in the higher spending that happened over the spring and summer months. I don’t remember spending all of February in the house, but our credit card purchases seem to say that’s what we did – no gas and no restaurants. In March, we splurged on a birthday dinner ($77!), which is unusual for us. From April through August, we were traveling (and therefore eating fast food and at sit-down restaurants), Mr. ODA had work trips (so he’s going out to eat with coworkers for multiple nights), and there seems to be one or two transactions each month where we paid for a group dinner that was reciprocated (and not captured). Under the restaurants category is also when we went for drinks somewhere. We went to a winery and had a couple of drinks with friends, and that could probably be considered “entertainment” versus eating outside the home.

HOUSE WORK

We put a lot of money into our house this year, which is surprising since it’s new construction. We finished our basement, which was about $15k instead of the $75k-100k that other people have been quoted for the job. We bought a patio set, a grill, and an entryway table. Mr. ODA built a “shed” under our deck (we can’t have free-standing sheds per the HOA, so we enclosed under the deck .. not “free standing” 🙂 ). Most of our furniture moved with us from the last house without an issue, but there were a few purchases needed. Between our initial move in purchases (a kitchen table and chairs), purchases in 2021, and a few purchases that have already happened in 2022, we should be done with big house purchases.

INCOME

I quit my job in 2019. I manage our 12 rental properties as my “job” now, but I also am open to part time jobs as something to do. In April 2021, I was asked if I could help fill a position at the race track during their Spring meet. It wasn’t a job that I wanted to go back and do in future meets. I mentioned that I’d work the Fall meet if I could do something like pour beer, and Mr. ODA’s dad (who works there) made it happen. I also worked some of the days of their horse sales. I worked 22 days for the year and contributed $5k to our family’s spending for the year.

LOOKING AHEAD

I’ll try to track our expenses in real time this year, so that I can categorize them more accurately. Watching expenses month-to-month means you can also make adjustments if you see you’ve spent more than usual in one category.

Finishing our basement meant that we moved furniture around. A sections that was in our dining room moved to the basement, freeing up the dining room to actually be a dining room; I purchased a table and chairs. The “playroom” toys were moved down to the basement, and that room became the guest room. It’s nice that the guests can have their own space on the first floor and not share a bathroom with the kids. That freed up the previous guest room to be an actual office, so I purchased a desk (our old desk was in poor shape and it didn’t move to KY with us). Other than that, I don’t see any major expenses on our own house for this year.

We expect to travel a lot again this year. We already have six trips planned. They’re all driving trips, so that’ll increase our gas category. I have one trip expected to fly to my sister’s baby shower, but that hasn’t been scheduled yet. We’ll also have day trips that we’ll do around our house, which is usually an hour to an hour and a half worth of driving.

While we don’t “budget” or believe in the “envelope system,” we do watch our spending on a regular basis. We check our accounts every few days to ensure there are no surprises as well (i.e., don’t wait for your statement to come and find out there have been false charges). Keep paying attention to what’s being spent and where your money is going so that you can make informed financial decisions.